Dollar and Yields Rise Sharply After Fed, But Both Near Key Barriers Ahead – Action Forex

It was a week packed with market-moving headlines and wild cross-asset swings. Traders found themselves caught between optimism over a U.S.–China trade breakthrough and caution sparked by a hawkish twist from the Fed. The result was a volatile mix that saw US equities push to new records, yields jump, and currencies shuffle in dramatic fashion.

Early in the week, markets cheered reports that Washington and Beijing had finalized a framework deal that would avert another round of 100% tariffs. Yet when the agreement was formally confirmed during US President Donald Trump’s Asia trip, the reaction was muted — a reminder that much of the optimism had already been priced in.

Central banks also took the center stage, dominating the midweek flow. The Fed stole the spotlight with a decision that, while delivering the expected cut, came laced with a distinctly hawkish tone. The message sent Treasury yields higher and revived Dollar’s appeal.

Across the border, the BoC initially sounded ready to pause their easing cycle, but a shock contraction in August GDP released later in the week quickly put the door to further cuts back on the table. Elsewhere, both the ECB and the BoJ opted for uneventful holds. Meanwhile in Australia, an unexpected surge in Q3 inflation forced traders to rethink the RBA’s policy path altogether — questioning even whether the central bank was done cutting.

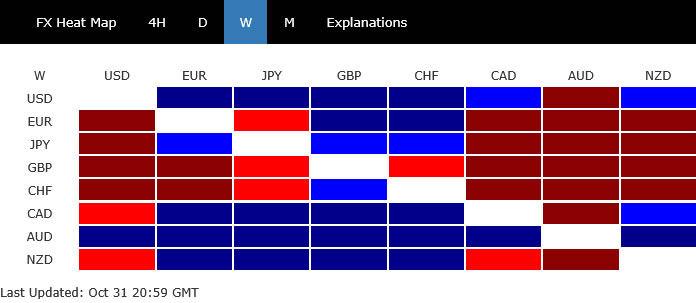

When the dust settled, Aussie led the pack, followed by Dollar and Loonie, Sterling’s fiscal woes left it trailing far behind. Swiss Franc and Euro were also on the weaker side, while Yen and Kiwi ended in the middle.

Wall Street Hits Record Highs Despite Fed Jolt

Risk sentiment stayed remarkably resilient in the US. Equity markets once again defied gravity, with all three major indexes powering to fresh record highs as optimism over global trade and tech earnings overshadowed the Fed’s hawkish tone.

NASDAQ jumped 2.2%, while S&P 500 rose 0.7% and DOW added 0.8%, marking yet another week of gains in a year already defined by relentless risk appetite. The tech-heavy Nasdaq led the charge as upbeat earnings from Amazon and Apple reinforced confidence that corporate profits can weather higher rates and trade uncertainty.

That tone was reinforced by the confirmation of the U.S.–China trade framework, which effectively took the threat of 100% tariffs off the table. The removal of a major tail risk helped investors stay committed to equities. The result was a market more inclined to consolidate gains than to correct them.

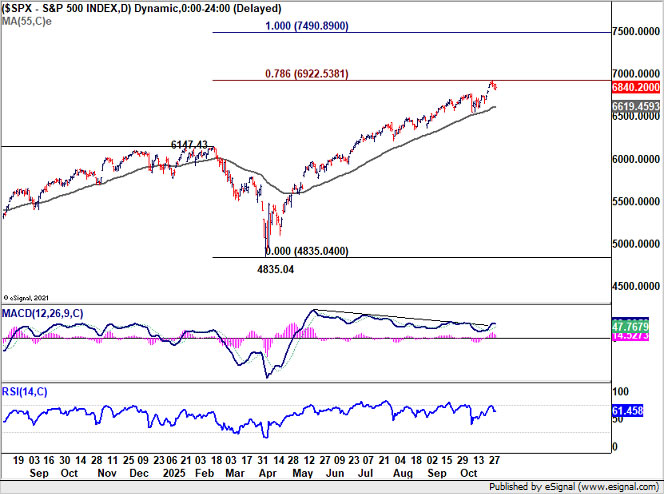

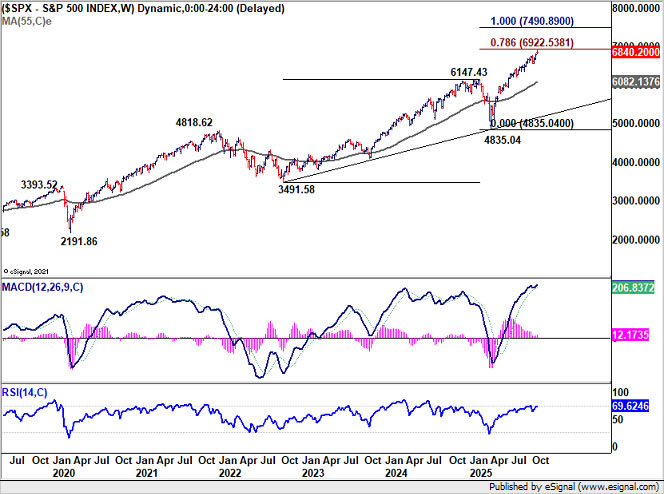

Technically, S&P 500 surged to as high as 6,920.34, just shy of 78.6% projection of 3491.58 to 6147.43 from 4835.04. The key question now is whether the index can break above 7,000 psychological barrier, where momentum could either fade or accelerate.

Sustained break above 7,000 — particularly if confirmed by D MACD’s upward cross above the falling trend line — would likely invite momentum chasing toward 100% projection at 7,490.89, possibly before year-end. Meanwhile, outlook will stay bullish as long as 55 D EMA (now at 6619.45) holds, in case of retreat.

Dollar and Yields Regain Strength After Fed’s Hawkish Cut

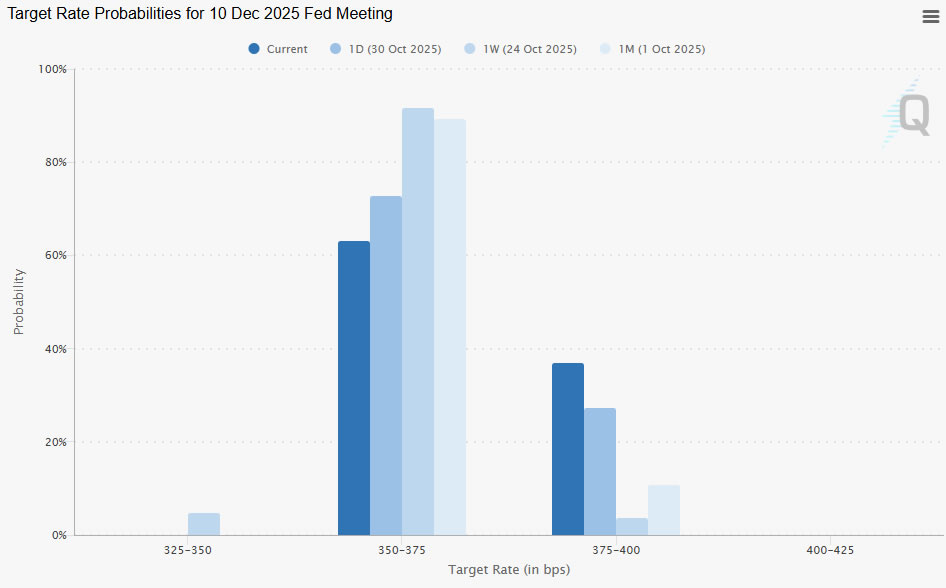

The Fed’s October meeting delivered both the expected and the unexpected — a 25bps cut as anticipated, but the underlying message came with a distinctly hawkish twist. Markets that had been positioned for a more dovish signal quickly adjusted, sending Treasury yields and Dollar higher.

The FOMC vote revealed deepening divisions within the committee. While Governor Stephen Miran called for a larger 50-basis-point reduction, Kansas City Fed President Jeffrey Schmid broke ranks by voting for no change. Schmid later defended his dissent, citing a balanced labor market, steady momentum, and still-elevated inflation as reasons to pause.

Schmid also argued that another cut would do little to alleviate structural labor market stress, emphasizing that “demographics and technology” are the main drivers behind slower job creation. More importantly, he warned that credibility risks could arise if the Fed appears too eager to ease before inflation is convincingly anchored near 2%.

Besides, Powell’s tone at the post meeting press conference aligned with that cautious stance. He emphasized that while the Fed remains flexible, “a December cut is not a foregone conclusion.”

Markets took note — futures pricing for another cut fell to around 63%, down sharply from above 90% the week before. The shift marked a turning point for sentiment around the U.S. rate path.

The bond market responded swiftly. 10-year yield’s extended rebound confirms short term bottoming at 3.947. Considering bullish convergence condition in D MACD, the fall from 4.629 could be complete too.

Further rise is now expected to 4.205 cluster resistance (38.2% retracement of 4.629 to 3.947 at 4.207). Strong resistance could emerge there to cap upside to set the range for sideway trading.

Dollar Index reclaimed upside traction, breaking through 99.56 resistance to resume the rebound from 96.21. Further rise is now expected, as long as 98.56 support holds, to 100.25 resistance and above. But upside should be capped by 38.2% retracement of 110.17 to 96.21 at 101.54.

However, a sustained push beyond 101.54 would signal a true bullish trend reversal, rather than a corrective bounce, particularly if accompanied by a break above 4.2% in the 10-year yield.

Sterling Trapped at the Bottom as UK Fiscal Woes Deepen

While Dollar was buoyed by hawkish Fed signals, the British Pound struggled and ended the week as the weakest among major currencies. The decline reflected growing fiscal unease in the UK as investors confronted a widening budget gap and rising concern about the government’s ability to maintain stability in public finances.

The selloff accelerated after reports that Chancellor Rachel Reeves faces a deeper fiscal hole than previously anticipated. The revelation complicates the government’s fiscal strategy at a time when the economy is already slowing and public debt levels remain historically high. Investors are increasingly worried that the UK will need to either tighten spending or raise taxes to restore credibility, both of which could undercut near-term growth.

For the BoE, the dilemma is becoming sharper. A significant fiscal tightening could offset some inflation pressures but at the cost of weaker demand — forcing the BoE to lean more dovishly in 2026. Markets are now debating whether Governor Andrew Bailey and his colleagues will need to accelerate rate cuts if fiscal tightening materializes, or if inflation persistence keeps them cautious for longer.

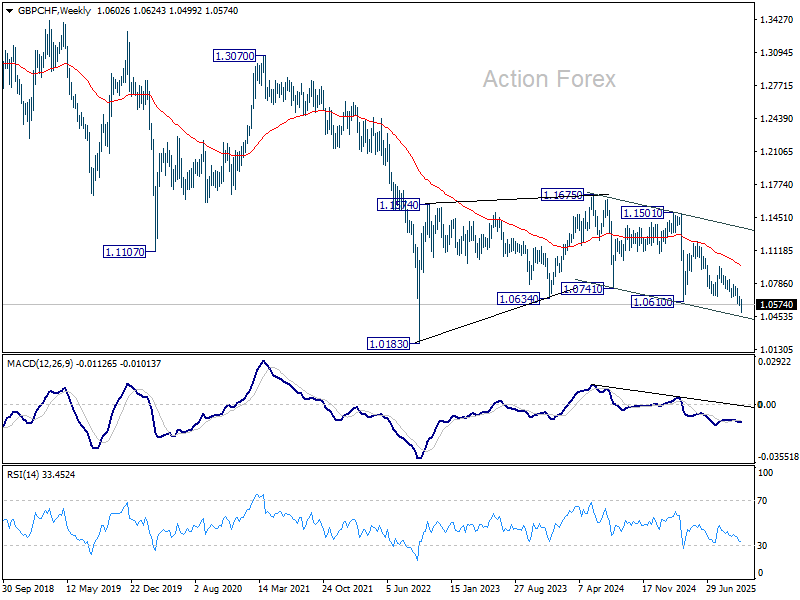

Technically, the Pound’s weakness is visible in GBP/CHF, which extended its downtrend to 1.0499 before stabilizing. Some consolidations could be seen in the near term, but outlook will stay bearish as long as 1.0658 support turned resistance holds. Next target is 100% projection of 1.1204 to 1.0658 from 1.0959 at 1.0413.

Current downside momentum, as seen in W MACD, doesn’t warrant a break through 1.0183 (2022 low). Range trading is still more likely to continue between 1.0183/1.1675 in the medium term. However, any pickup in downside momentum could mean that GBP/CHF is actually ready to resume the multi-decade down trend.

Aussie Outperforms as Traders Push Back RBA Easing Timeline

In contrast to Sterling’s fiscal drag, Aussie emerged as the standout performer of the week, buoyed by much stronger-than-expected Q3 CPI report that caught RBA, economists, and traders off guard.

In response, money-market pricing for a November or December cut has collapsed, with several leading institutions now forecasting no additional easing this year. Instead, traders are focusing on the February 2026 meeting as the next plausible window for policy action — and only if Q4 inflation, due in January, shows clear disinflation momentum.

That outlook could change only if the labor market deteriorates materially, forcing the RBA to respond. So far, however, employment data have remained resilient, reinforcing the view that the Bank can afford to wait and watch.

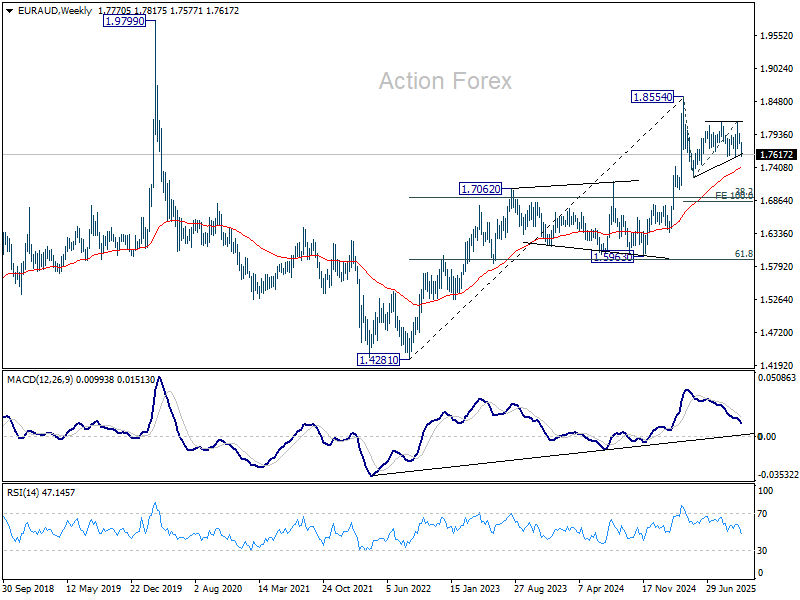

Technically, EUR/AUD is a key pair to monitor in the coming days. Decisive break below 1.7569 support confirms that the fall from 1.8554 (2025 high) has resumed. The next near-term target lies at 1.7245, with a firm break there opening the way toward 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 down the road.

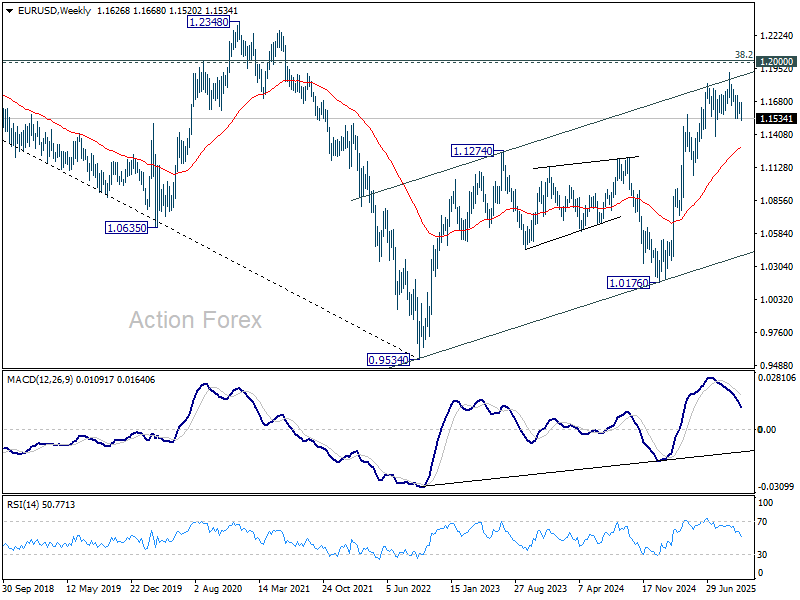

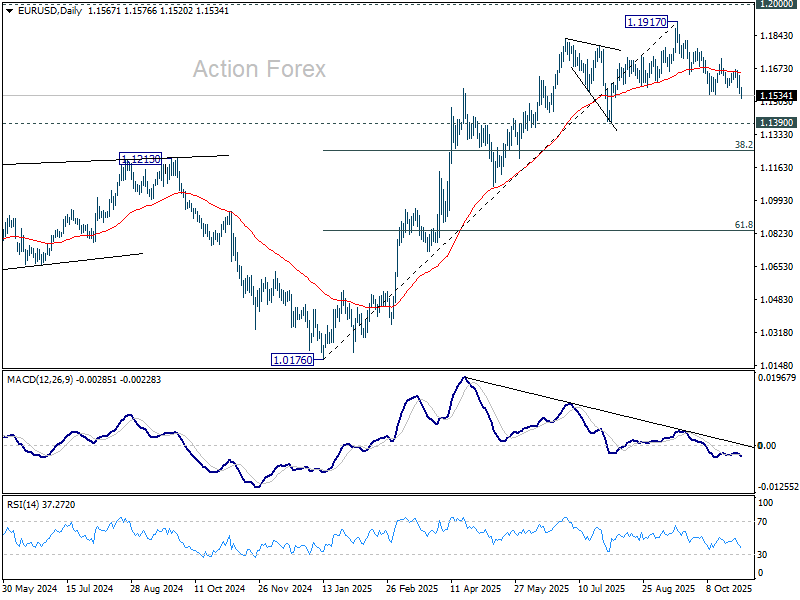

EUR/USD Weekly Outlook

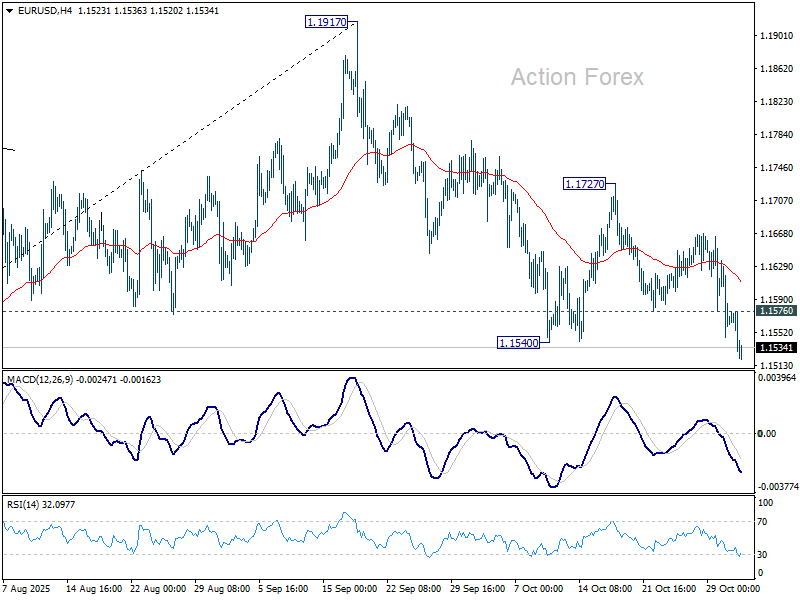

EUR/USD’s fall from 1.1917 resumed by late break of 1.1540 support. Initial bias stays on the downside this week for 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, above 1.1576 minor resistance will turn bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1298) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep larger outlook bearish.

In the long term picture, 38.2% retracement of 1.6039 to 0.9534 at 1.2019, which is close to 1.2000 psychological level is the key for the outlook. Rejection by this level will keep the multi decade down trend from 1.6039 (2008 high) intact, and keep outlook neutral at best. However, decisive break of 1.2000/19, will suggest long term bullish trend reversal, and target 61.8% retracement at 1.3554.