Another Day, Same Story: Yen Extends Losses, Sterling Under Pressure, Franc Firm – Action Forex

The key themes driving global FX markets this week continued to dominate today’s session, with Yen weakness, Sterling softness, and Swiss Franc strength dominating. Political pressure in Japan, renewed rate-cut expectations in the UK, and optimism over a U.S.–Swiss trade breakthrough have kept traders rotating between safety and growth exposures, while risk sentiment remains mixed.

In Japan, the Yen’s selloff extended as Prime Minister Sanae Takaichi again urged the BoJ to hold off on tightening, arguing that the current bout of inflation—driven largely by food prices—is not the kind policymakers should welcome. Her public stance has effectively narrowed the odds of a rate hike this year. Governor Kazuo Ueda would likely refrain from proposing any move at the December meeting, with January seen as the earliest possible window for resuming normalization.

In the UK, Sterling remained under pressure as traders grew more confident that the BoE will deliver a rate cut in December, following weak employment data earlier this week. The Q3 GDP figures due tomorrow will be a critical input into those expectations, while the Autumn Budget on November 26 is viewed as the final political hurdle before easing can proceed.

Meanwhile, the Swiss Franc continued to outperform on mounting optimism that Washington and Bern are close to finalizing a trade deal that would slash U.S. tariffs on Swiss exports from 39% to 15%. Such a move would align Swiss treatment with that of EU goods, boosting the country’s export competitiveness and capital inflows.

Across broader markets, investors are awaiting a crucial U.S. House vote expected later today that could finally bring an end to the historic government shutdown. Yet sentiment remains tentative, with AI-related and semiconductor stocks oscillating after recent heavy swings. The uncertainty has kept risk appetite from gaining a firm footing, especially among commodity-linked currencies.

For the week so far, Swiss Franc leads as the strongest performer, followed by Aussie and Kiwi, though both antipodeans remain capped below last week’s highs, reflecting the prevailing indecision in risk trades. On the other end, Yen is the weakest, trailed by Sterling and Dollar, while Euro and Loonie are holding mid-pack.

In Europe, at the time of writing, FTSE is up 0.03%. DAX is up 1.27%. CAC is up 1.35%. UK 10-year yield is up 0.029 at 4.421. Germany 10-year yield is up 0.002 at 2.665. Earlier in Asia, Nikkei rose 0.43%. Hong Kong HSI rose 0.85%. China Shanghai SSE fell -0.07%. Singapore Strait Times rose 0.59%. Japan 10-year JGB yield fell -0.004 to 1.691.

ECB’s Schnabel: Rates appropriately set, inflation still sticky

ECB Executive Board member Isabel Schnabel said interest rates are “in a good place,” indicating no immediate need to shift policy as long as major shocks are avoided. “If there is no big shock, I would be rather relaxed,” she saidat a conference today.

Still, Schnabel warned that the risks to inflation are “tilted a little bit to the upside”. “Services inflation is a bit higher than we thought,” she noted, adding that pay pressures are cooling “more slowly than expected.”

Schnabel also pointed to signs that the Eurozone economy is recovering faster than feared, citing October’s PMI improvement as evidence that growth momentum is picking up even under higher U.S. tariffs.

“My narrative is one of an economy that is recovering, with a closing output gap,” she said.

RBA’s Jones warns on geopolitical risk underpricing, notes Gold shift

RBA Assistant Governor Brad Jones cautioned that global markets may be underestimating geopolitical risks and systemic fragmentation. At a conference today, he highlighted that risk premiums across major asset classes have fallen to “concerning lows,” suggesting investors are failing to fully price in potential shocks.

“We’re just surprised that there’s not a bit more reflected in spreads given what we observe,” Jones said, pointing to what he called “a confronting set of potential risks.”

Jones also drew attention to shifting dynamics in global reserve management, noting “emerging evidence of fragmentation” in how central banks allocate their assets. He said a distinct group of countries has driven the recent surge in official Gold holdings, reflecting a growing desire to diversify away from dollar- and euro-denominated assets amid heightened concerns about “risk of asset seizure sanctions”.

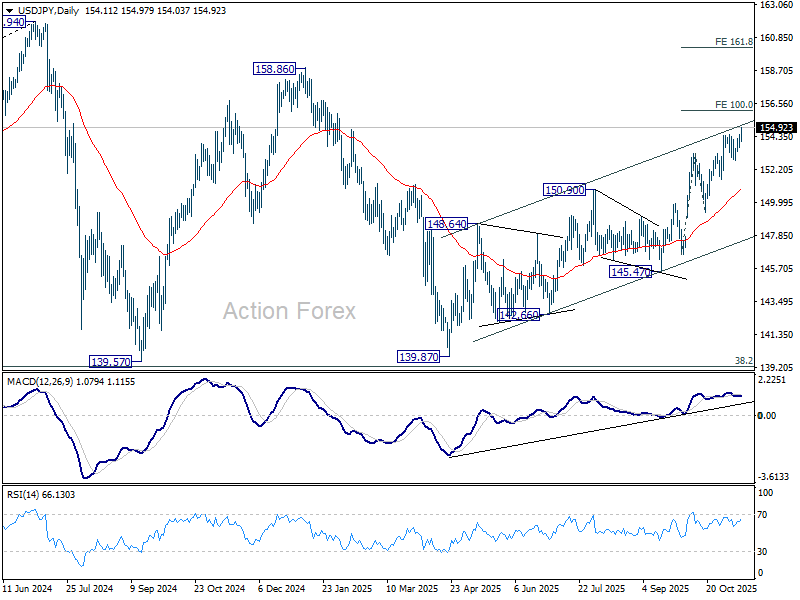

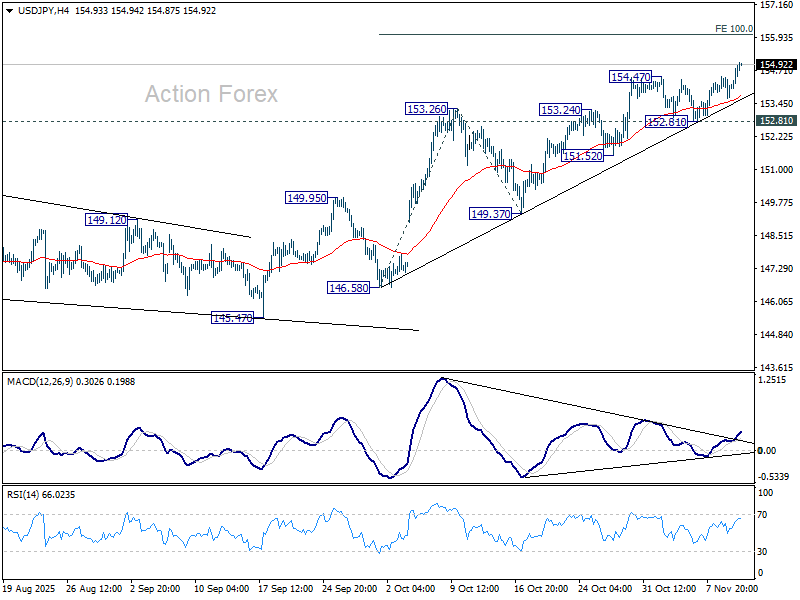

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 153.72; (P) 154.11; (R1) 154.54; More…

USD/JPY’s rally continues today and intraday bias stays on the upside. Current rally from 139.87 should target 100% projection of 146.58 to 153.26 from 149.37 at 156.05. Firm break there will pave the way to 158.86 key structural resistance. For now, near term outlook will stay bullish as long as 152.81 support holds, in case of retreat.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 149.37 support will dampen this bullish view and extend the corrective pattern with another falling leg.