Franc Leads Safe-Haven Bid, Tech Rout Pressures Sentiment – Action Forex

Risk aversion intensified with markets once again gripped by tech-led weakness. Nvidia slumped in premarket trading, dragging the broader semiconductor and AI complex lower and reinforcing concerns that the sector’s valuation reset still has further to run. The risk-off tone spilled over into cryptocurrencies, where Bitcoin dropped more than 2% and looked increasingly vulnerable to a break below the 95k level.

In currencies, Swiss Franc’s rally accelerated as safe-haven inflows picked up pace. For the first time this week, the depth of risk aversion was also enough to lift Yen, which finally staged a rebound after spending days pinned at the bottom of the performance table on expectations of delayed BoJ tightening. By contrast, Sterling and Aussie were among the weakest performers, while Dollar also traded with a soft bias. Euro and Loonie held to the middle of the pack.

A key question for the final hours is whether tech stocks can deliver another bout of late-session short covering, similar to last Friday’s dramatic reversal. But with sentiment deteriorating quickly and positioning still heavy in AI-linked names, the risk of a deeper, more disorderly selloff cannot be ruled out.

In the UK, reports that the Office for Budget Responsibility has upgraded its fiscal forecasts trigged some volatility. Sources suggested that Chancellor Rachel Reeves is now unlikely to raise income taxes in this month’s Budget, given the improved outlook. The Treasury declined to comment, but markets reacted swiftly.

Gilt yields jumped sharply on the news as government bond prices fell, reflecting expectations of looser fiscal constraints. Sterling attempted a brief recovery but failed to build momentum, weighed by softer risk appetite and ongoing speculation that the BoE could cut rates as early as next month.

In Europe, at the time of writing, FTSE is down -1.74%. DAX is down -1.61%. CAC is down -1.47%. UK 10-year yield is up 0.079 at 4.520. Germany 10-year yield is down -0.001 at 2.691. Earlier in Asia, Nikkei fell -1.77%. Hong Kong HSI fell -1.85%. China Shanghai SSE fell -0.97%. Singapore Strait Times fell -0.65%. Japan 10-year JGB yield rose 0.011 to 1.702.

EU swings back to surplus, powered by chemicals and US trade

The Eurozone posted a solid EUR 19.4B trade surplus in September, supported by broad rise in goods exports. Outbound shipments increased 7.7% yoy to EUR 256.6B, outpacing the 5.3% yoy rise in imports.

The broader EU trade balance also swung sharply back into surplus, moving from a EUR -4.5B deficit in August to a EUR 16.3B surplus in September. The turnaround was driven primarily by a strong rebound in the chemicals sector, where the surplus jumped from EUR 15.4B to EUR 26.9B.

On a partner basis, EU shipments to the US were a major driver, rising 15.4% yoy to EUR 53.1B. Imports from the U.S. grew a solid 12.5%, leaving a wider EUR 22.2B surplus. Trade with Switzerland was also strong: exports increased 13.4% and imports 10.6%, taking the bilateral surplus to EUR 6.7B. In contrast, exports to China fell -2.5% yoy, while imports rose 3.6%, pushing the deficit with China deeper to EUR -33.1B. Trade flows with the UK were mixed, as exports rose 2.8% yoy, while imports dipped -0.3%, widening the surplus to EUR 16.1B.

China industrial production slows to 4.9% yoy in October, investment contraction deepens

China’s October activity data pointed to a loss of momentum, with industrial production rising 4.9% yoy, down from September’s 6.5% yoy and below expectations of 5.6%. It marks the weakest annual pace since August 2024.

Retail sales also slowed, rising 2.9% yoy compared with 3.0% in September, though slightly outperforming expectations of 2.7% yoy. Still, it was the slowest pace since August last year, underscoring persistently cautious household demand. Excluding autos, consumer goods retail sales rose a firmer 4.0%, suggesting pockets of resilience but not enough to anchor a broad consumption recovery.

More concerning was the continued drag from investment: fixed asset investment fell -1.7% ytd yoy, deteriorating from -0.5% and missing expectations of -0.7%. Private-sector investment remained under heavy pressure, dropping -4.5%, underscoring structural weakness in confidence, property-linked spillovers, and limited risk appetite.

New Zealand BNZ PMI at 51.4 as orders hit three-year high

New Zealand’s manufacturing sector showed further improvement in October, with BusinessNZ PMI rising from 50.1 to 51.4, marking a fourth straight month above 50. While still below the long-term average of 52.4, the sector is now experiencing its most sustained period of expansion in three years, hinting that the worst of the downturn may be behind it.

The details were encouraging: production improved from 50.5 to 52.0. New orders jumped from 50.5 to 54.9, the strongest pace since August 2022 and a key sign that demand conditions are firming. Employment remained in contraction at 48.1, up from 47.7, but even that component showed stabilization after six months of declines.

BusinessNZ’s Catherine Beard said October brought “more signs of life” after months of stagnation. The share of negative respondent comments fell from 60.2% to 54.1%, with many firms reporting stronger orders, seasonal demand, new customers, and productivity gains driven by process improvements and automation.

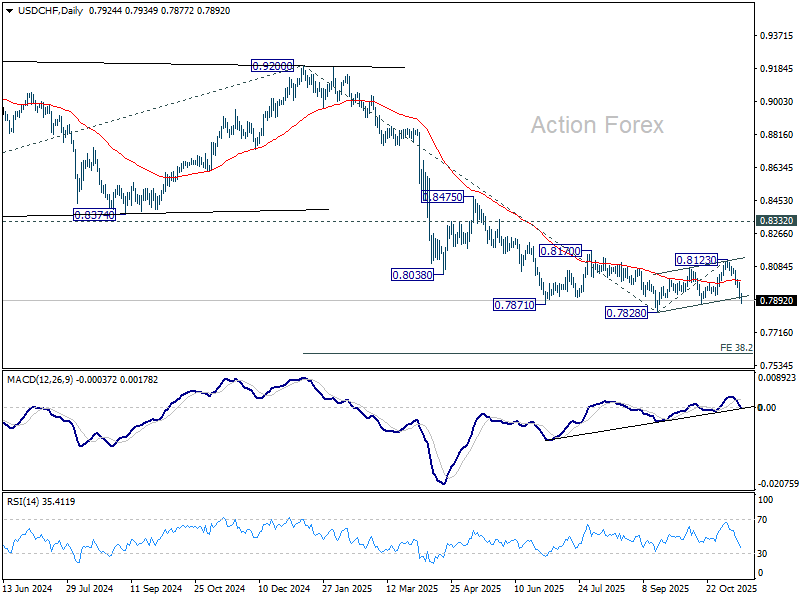

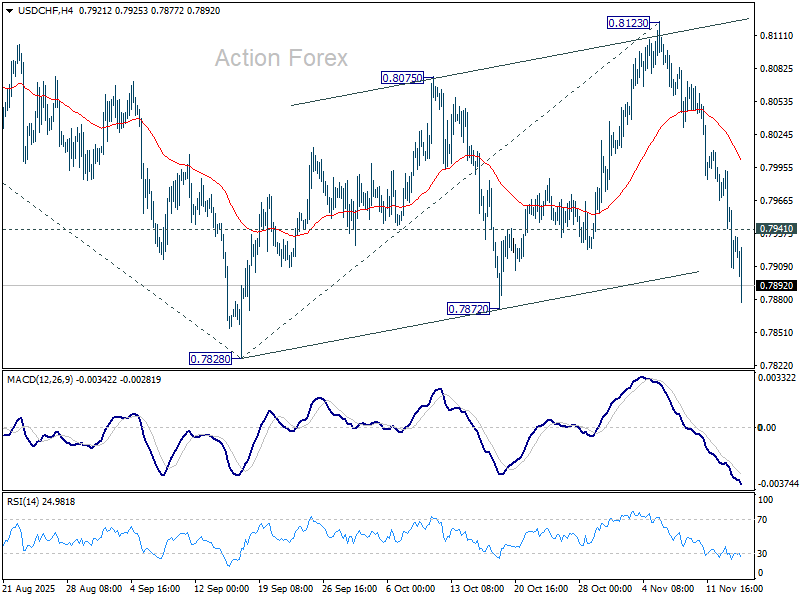

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7894; (P) 0.7944; (R1) 0.7979; More…

USD/CHF’s fall from 0.8123 accelerates lower today and intraday bias remains on the downside. Decisive break of 0.7872 support will argue that larger down trend is ready to resume. Break of 0.7828 will target 38.2% projection of 0.9200 to 0.7828 from 0.8123 at 0.7599. On the upside, above 0.7941 minor resistance will delay the bearish case and bring more consolidations first.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).