UK Political Noise Weighs Slightly on GBP, FX Board Shows No Clear Theme – ActionForex

Sterling weakened slightly today as markets digested last night’s abrupt resignation of OBR Chair Richard Hughes, who stepped down following the premature release of budget documents last week. Investors viewed the episode as destabilizing for an institution designed to promote fiscal transparency and market confidence.

There was also a delayed reaction to UK Prime Minister Keir Starmer’s remarks, in which he reiterated his goal of driving inflation lower to enable further rate cuts and reduce business-investment costs.

In contrast, Yen is the worst performer of the day, unwinding much of its earlier gains. Markets initially bid up the currency early in the week on speculation of a possible BoJ rate hike, but enthusiasm has faded quickly. Risk-on sentiment has returned across global markets, removing the defensive bid that had supported JPY.

The re-pricing has shifted the day’s FX rankings, with Aussie on top, followed by Euro and Swiss Franc. Sterling and Kiwi sit near the bottom, while Dollar and Loonie hold middle ground.

The distribution of moves suggests no strong singular narrative is driving markets. Instead, today’s flows reflect a combination of UK political noise, unwinding of BoJ-related bets, and a cautious return of risk-taking in global markets—all contributing to a fragmented and directionless environment across major FX pairs.

In Europe, at the time of writing, FTSE is up 0.15%. DAX is up 0.39%. CAC is up 0.08%. UK 10-year JGB yield is up 0.012 at 4.498. Germany 10-year yield is up 0.009 at 2.765. Earlier in Asia, Nikkei closed flat. Hong Kong HSI rose 0.24%. China Shanghai SSE fell -0.42%. Singapore Strait Times rose 0.26%. Japan 10-year JGB yield fell -0.017 to 1.862.

OECD: Tariffs to weigh on 2026 global growth; inflation to ease

OECD’s latest economic outlook points to a cooling global economy over the next two years as higher effective tariff rates and persistent geopolitical uncertainty weigh on activity.

Global growth is projected to slow from 3.2% in 2025 to 2.9% in 2026 before recovering modestly to 3.1% in 2027. The US is expected to decelerate from 2.0% growth in 2025 to 1.7% in 2026, while the Eurozone will hover near 1.2%–1.4% through 2027. China’s growth is seen easing from 5.0% in 2025 to 4.3% by 2027 as structural and external pressures build.

Near-term momentum is expected to soften as global trade and investment absorb the impact of higher tariffs, weaker confidence, and ongoing policy uncertainty. OECD expects conditions to improve toward late 2026 as the drag from tariffs fades, financial conditions ease, and lower inflation supports demand.

Inflation is expected to continue moderating. Headline CPI across the G20 is projected to fall from 3.4% this year to 2.9% in 2026 and 2.5% in 2027. By mid-2027, inflation is expected to be back to target in most major economies, allowing central banks additional flexibility to support growth if needed.

Eurozone CPI edges higher to 2.2% in November; services rise to 3.5%

Eurozone headline inflation ticked up slightly in November, rising to 2.2% yoy from 2.1% and coming in just above expectations of 2.1%. Core CPI (ex energy, food, alcohol & tobacco) held unchanged at 2.4%, matching forecasts.

Looking at the details, services were the main driver of inflation, climbing to 3.5% from 3.4%. Food, alcohol and tobacco inflation stayed steady at 2.5%. Non-energy industrial goods were unchanged at 0.6%, and energy inflation remained negative at –0.5% but improved from –0.9%.

Labor-market data painted a slightly softer picture. Eurozone unemployment rose to 6.4% in October from 6.3%, missing expectations of 6.3%.

RBNZ’s Breman sets tone for Leadership: Mandate discipline and public trust

New RBNZ Governor Anna Breman used her first appearance before a parliamentary committee to underline a back-to-basics approach for the central bank. She said her leadership will be “laser focused” on the core mandate of keeping inflation low and stable, ensuring financial system resilience, and maintaining a safe and efficient payments framework.

Her comments signal an intention to anchor policy discussions firmly around credibility and discipline after a period of volatility in inflation and rate expectations. By highlighting the fundamentals of price stability and financial stability, Breman appears set to build continuity with the bank’s existing stance while strengthening its emphasis on execution and institutional reliability.

Looking into 2026, Breman said “transparency, accountability, and clear communication” will be central pillars of her leadership. She noted that maintaining public trust is critical for the next phase of policy.

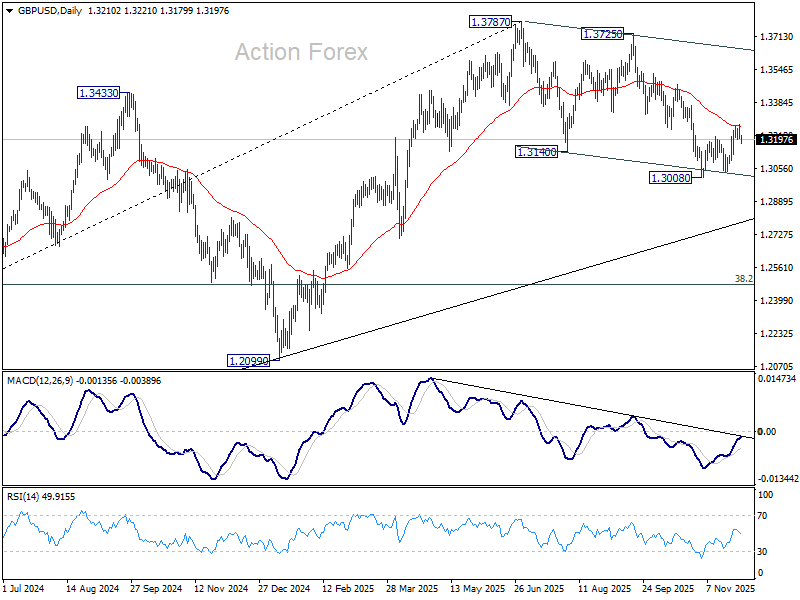

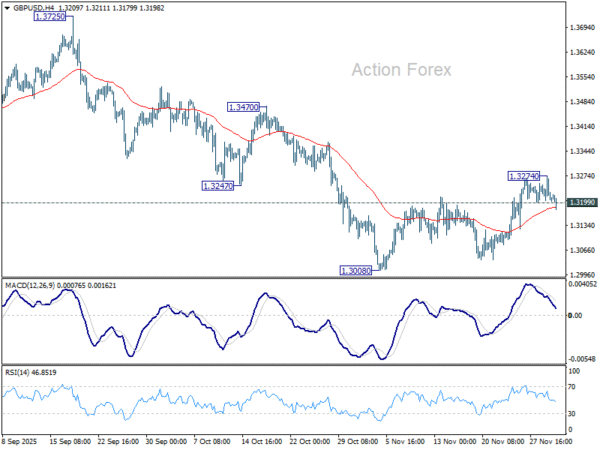

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3188; (P) 1.3232; (R1) 1.3257; More…

GBP/USD’s break of 1.3199 minor support argues that recovery from 1.3008 might have completed as a three-wave corrective move to 1.3274. That came after touching 55 D EMA (now at 1.3265). Intraday bias is back on the downside for retesting 1.3008 low. On the upside, however, sustained trading above 55 D EMA should confirm that fall from 1.3787 has completed. Further rise should then be seen to 1.3725/3787 resistance zone.

In the bigger picture, the break of 55 W EMA (now at 1.3184) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2760) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.