Yen Selloff Continues With Dollar, Commodity Currencies Strong

The forex markets continue to stay in sort of risk-on mode today, with weakness in Dollar and Yen, and strength in commodity currencies as led by New Zealand Dollar. Though, traders in other markets are not too committed yet. European indexes are just mixed while US futures point to slightly higher open. There is prospect for S&P 500 to follow NASDAQ to make new record high today, but we’ll see how it goes.

Technically, selloff in Yen solidifies with breach of 110.95 key resistance in USD/JPY and 132.63 minor resistance in EUR/JPY. AUD/JPY also breaks 83.95 resistance to indicate completion of three-wave correction from 85.78. Similarly, NZD/JPY breaks 78.06 resistance to indicate completion of three-wave correction from 80.17. But weakness in Dollar is not too convincing yet. We’ll continue to pay attention to 4 hour 55 EMA at 1.1995 in EUR/USD, 1.3984 in GBP/USD, 0.9113 in USD/CHF and 1.2277 in USD/CAD.

In Europe, at the time of writing, FTSE is up 0.46%. DAX is down -0.30%. CAC is down -0.32%. Germany 10-year yield is down -0.020 at -0.181. Earlier in Asia, Nikkei dropped -0.03%. Hong Kong HSI rose 1.79%. China Shanghai SSE rose 0.25%. Singapore rose 0.30%. Japan 10-year JGB yield rose 0.0009 to 0.056.

Canada retail sales dropped -5.7% in Apr on pandemic third wave

Canada retail sales dropped -5.7% mom to CAD 54.8B in April, worse than expectation of -5.1% mom. That’s the largest decline since April 2020, due to the third wave of pandemic. Ex-auto sales dropped -7.2% mom, versus expectation of -4.4% mom.

Largest declines were observed in clothing and clothing accessories stores (-28.6%) and general merchandise stores (-8.1%). Sales decreased in 9 of 11 subsectors, representing 74.2% of retail trade.

Statistics Canada’s advance estimate suggests that sales would have declined further by -3.2% in May.

UK PMI composite ticked lower to 61.7, expansion rate appears peaked

UK PMI Manufacturing dropped to 64.2 in June, down from 65.6, above expectation of 64.0. PMI Services dropped to 61.7, down from 62.9, below expectation of 63.0. PMI Composite dropped to 61.7, down from 62.9.

Chris Williamson, Chief Business Economist at IHS Markit, said: “There are some signs that the rate of expansion appears to have peaked, as both output and new order growth cooled slightly from May’s record performances, but full order books and a further loosening of virus-fighting restrictions should nevertheless help ensure growth remains strong as we head through the summer.

“However, inflation worries have continued to intensify. Record levels of the survey’s price gauges and the further development of capacity constraints hint strongly that consumer price inflation has much further to rise after already breaching the Bank of England’s 2% target in May.

Eurozone PMI composite rose to 59.2, 15-year high

Eurozone PMI Manufacturing was unchanged at 63.1 in May, above expectation of 62.1. PMI Services rose to 58.0, up from 55.2, above expectation of 57.6, and a 41-month high. PMI Composite rose to 59.2, up from 57.1, a 180-month high.

Chris Williamson, Chief Business Economist at IHS Markit said: “The eurozone economy is booming at a pace not seen for 15 years as businesses report surging demand, with the upturn becoming increasingly broad-based, spreading from manufacturing to encompass more service sectors, especially consumer-facing firms… The data set the scene for an impressive expansion of GDP in the second quarter to be followed by even stronger growth in the third quarter.

“However, the strength of the upturn – both within Europe and globally – means firms are struggling to meet demand, suffering shortages of both raw materials and staff. Under these conditions, firms’ pricing power will continue to build, inevitably putting further upward pressure on inflation in the coming months.”

Germany PMI Manufacturing rose to 64.9 in June, up from 64.4, above expectation of 63.0. PMI Services rose to 58.1, up from 52.8, a 123-month high, above expectation of 55.5. PMI Composite rose to 60.4, up from 56.2, also a 123-month high.

France PMI Manufacturing dropped to 58.6 in June, down from 59.4, below expectation of 59.0. PMI Services rose to 57.4, up from 56.6, hitting a 38-month high, but missed expectation of 59.4. PMI Composite rose to 57.1, up slightly from 57.0, an 11-month high.

Japan PMI manufacturing dropped to 51.5, output back in contraction

Japan PMI Manufacturing dropped to 51.5 in June, down from May’s 53.0. Manufacturing Output dropped to 49.1, down from 53.7, back in contraction for the first time since January. PMI Services rose slightly to 47.2, up from 46.5. PMI Composite dropped to 47.8, down from 48.8.

Usamah Bhatti, Economist at IHS Markit, said: “Activity at Japanese private sector businesses remained in contraction territory… Panel members commonly associated disruption to operating conditions to ongoing COVID-19 restrictions, coupled with severe supply chain pressures, notably for manufacturers.

“That said, one bright note was private sector firms in Japan continued to expand employment levels despite subdued demand conditions… Despite the ongoing pandemic-related restrictions on the Japanese economy, private sector businesses were optimistic that business conditions would improve in the year ahead, and to a greater extent than that seen in May.”

Australia goods export hits new record, led by China and Hong Kong

According to preliminary estimate, Australia exports of goods rose 11.0% mom to AUD 39.2B in May. Imports of goods rose 1.0% mom to AUD 25.9B. Goods trade surplus widened to AUD 13.3B, from AUD 9.7B. That’s a record trade surplus as iron ore, together with strong coal and meat exports, has helped boost total exports to a new record high

Exports to China jumped AUD 2271m or 16%, to Hong Kong by AUD 622m or 69%, to Singapore by 133m or 9%. Exports to Japan dropped AUD 160m or -4%, to South Korea by AUD 280m or -11%.

Australia PMI composite dropped to 56.1, growth momentum eased by remained strong

Australia PMI Manufacturing dropped back to 58.4 in June, down from may’s 60.4. PMI Services dropped to 56.0, down from 58.0. PMI Composite dropped to 56.1, down from 58.0.

Jingyi Pan, Economics Associate Director at IHS Markit, said: “Australia’s private sector growth momentum further eased in June but remained at a strong level to indicate continued improvement in economic conditions during the recovery from the COVID-19 pandemic. Renewed movement restrictions in the Victorian state and supply constraints stood out as two key reasons weighing on the growth momentum for Australia in the June flash PMI data, which is worth scrutinising. Meanwhile private sector firms were also slightly less optimistic with regards to output in the next 12 months amid the uncertain virus and supply situation.”

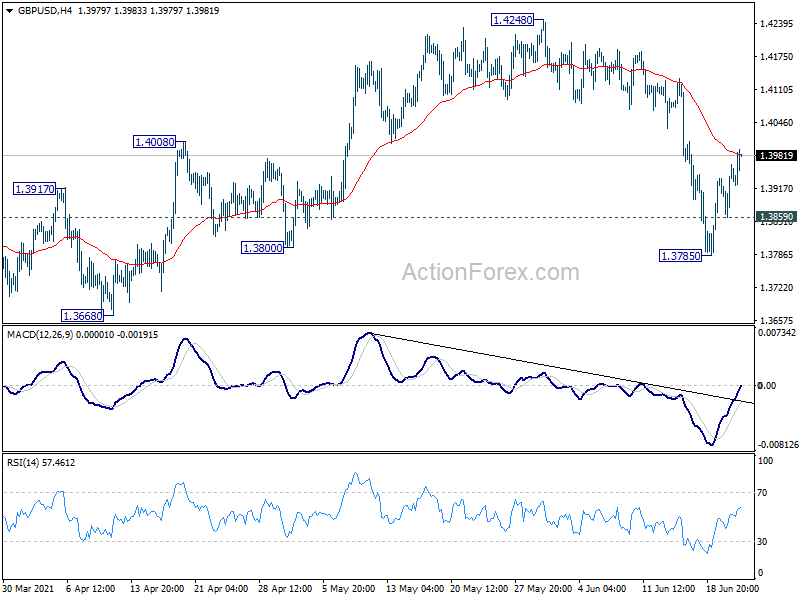

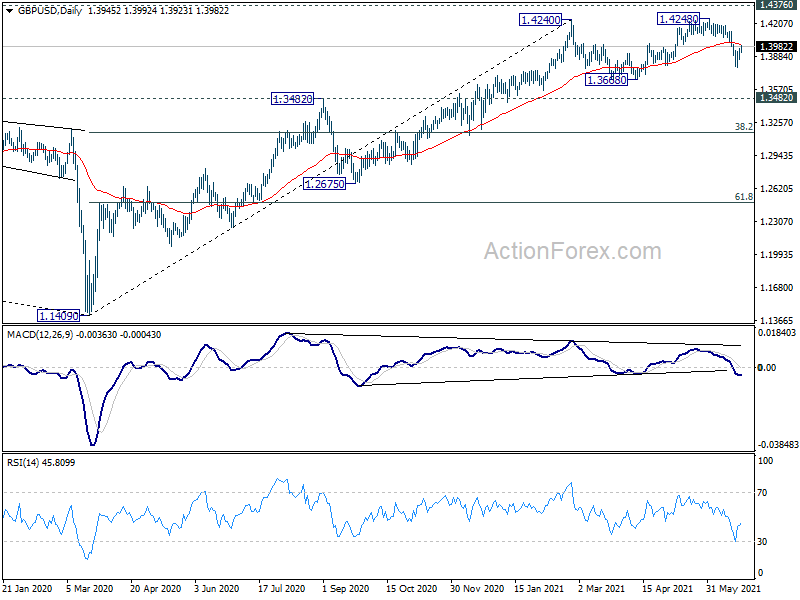

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3884; (P) 1.3924; (R1) 1.3987; More….

Intraday bias in GBP/USD stays neutral with focus now on 4 hour 55 EMA (now at 1.3983). Sustained break above this EMA will suggest that correction from 1.4248 has completed at 1.3785 already. Intraday bias will be turned back to the upside, for stronger rise back to retest 1.4248. On the downside, below 1.3859 minor support will resume the correction to 1.3668 support and below.

{kind=link}

In the bigger picture, as long as 1.3482 resistance turned support holds, up trend from 1.1409 should still continue. Decisive break of 1.4376 resistance will carry larger bullish implications and target 38.2% retracement of 2.1161 (2007 high) to 1.1409 (2020 low) at 1.5134. However, firm break of 1.3482 support will argue that the rise from 1.1409 has completed and bring deeper fall to 1.2675 support and below.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | CBA Manufacturing PMI Jun P | 58.4 | 60.4 | ||

| 23:00 | AUD | CBA Services PMI Jun P | 56.0 | 58.0 | ||

| 23:50 | JPY | BoJ Minutes | ||||

| 00:30 | JPY | Manufacturing PMI Jun P | 51.5 | 53.2 | 53.0 | |

| 07:15 | EUR | France Manufacturing PMI Jun P | 58.6 | 59.0 | 59.4 | |

| 07:15 | EUR | France Services PMI Jun P | 57.4 | 59.4 | 56.6 | |

| 07:30 | EUR | Germany Manufacturing PMI Jun P | 64.9 | 63.0 | 64.4 | |

| 07:30 | EUR | Germany Services PMI Jun P | 58.1 | 55.5 | 52.8 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Jun P | 63.1 | 62.1 | 63.1 | |

| 08:00 | EUR | Eurozone Services PMI Jun P | 58.0 | 57.6 | 55.2 | |

| 08:30 | GBP | Manufacturing PMI Jun P | 64.2 | 64.0 | 65.6 | |

| 08:30 | GBP | Services PMI Jun P | 61.7 | 63.0 | 62.9 | |

| 12:30 | CAD | Retail Sales M/M Apr | -5.70% | -5.10% | 3.60% | 4.50% |

| 12:30 | CAD | Retail Sales ex Autos M/M Apr | -7.20% | -4.40% | 4.30% | 5.40% |

| 12:30 | USD | Current Account (USD) Q1 | -195.7B | -205B | -188B | |

| 13:00 | CHF | SNB Quarterly Bulletin Q2 | ||||

| 13:45 | USD | Manufacturing PMI Jun P | 61.5 | 62.1 | ||

| 13:45 | USD | Services PMI Jun P | 70 | 70.4 | ||

| 14:00 | USD | New Home Sales M/M May | 876K | 863K | ||

| 14:30 | USD | Crude Oil Inventories | -3.6M | -7.4M |