Dollar Up on ADP Job Data, Sterling Lifted by BoE Haldane

Dollar and Loonie rise in early US session after better than expected economic data. Sterling follows closely after hawkish comments from BoE chief economist. As for today, Swiss Franc is currently the worst performing, followed by New Zealand and than Australian Dollars. The greenback is surviving the first data test and focus will stay on ISM manufacturing tomorrow, and non-farm payrolls on Friday.

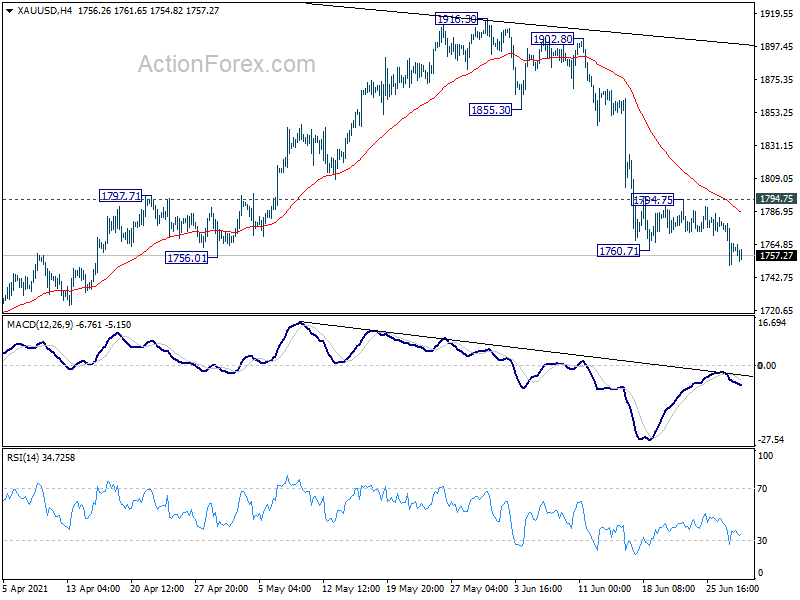

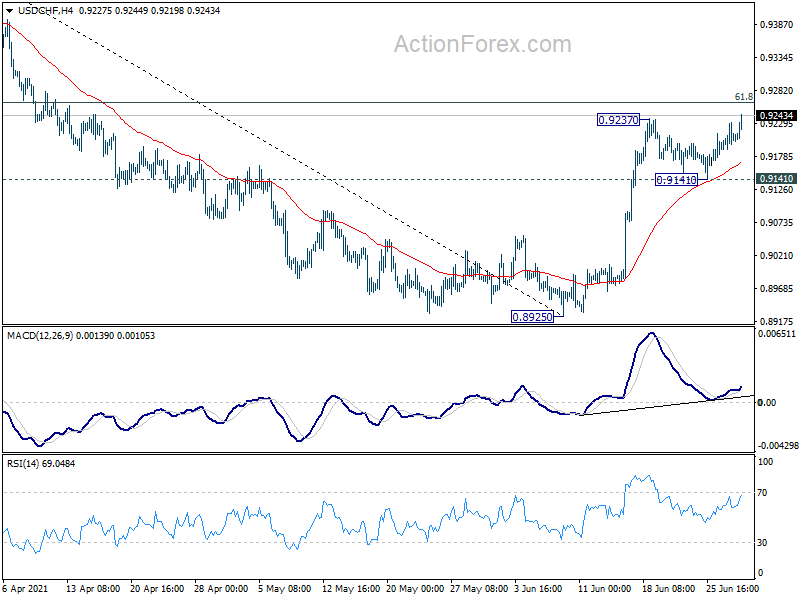

Technically, USD/CHF’s break of 0.9237 resistance is another sign of Dollar strength. But EUR/USD will need to break through 1.1846 support to affirm underlying momentum. GBP/USD and AUD/USD will also need to break through 1.3785 and 0.7476 support levels respectively. Gold’s softness is also consistent with more upside for the greenback. We’ll look for sign of downside acceleration in Gold through 1700 handle.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.42%. DAX is down -0.74%. CAC is down -0.53%. Germany 10-year yield is down -0.0207 at -0.188. Earlier in Asia, Nikkei dropped -0.07%. Hong Kong HSI dropped -0.57%. China Shanghai SSE rose 0.50%. Singapore Strait Times rose 1.33%. Japan 10-year JGB yield dropped -0.0003 to 0.060.

US ADP jobs grew 692k, services doing the heavy lifting

US ADP employment grew 692k in June, above expectation of 600k. By company size, small businesses added 215k jobs, medium businesses added 236k, large businesses added 240k. By sector, goods-producing jobs grew 68k, service-providing grew 624k.

“The labor market recovery remains robust, with June closing out a strong second quarter of jobs growth,” said Nela Richardson, chief economist, ADP. “While payrolls are still nearly 7 million short of pre-COVID-19 levels, job gains have totaled about 3 million since the beginning of 2021. Service providers, the hardest hit sector, continue to do the heavy lifting, with leisure and hospitality posting the strongest gain as businesses begin to reopen to full capacity across the country.”

Canada GDP contracted -0.3% mom in Apr, first decline in a year

Canada GDP contracted -0.3% mom in April, better than expectation of -0.80%. That’s the first contraction after 11 consecutive monthly growth. Total economic activity remains about -1% below its pre-pandemic level in February 2020.

12 of 20 industrial sectors were down. Good producing industries’ 0.5% gain were more than offset by -0.6% mom contraction in services-producing industries.

Preliminary information indicates a further -0.3% mom contraction in real GDP in May.

Also released Canada IPPI rose 2.7% mom in May, RMPI rose 3.2% mom.

BoE Haldane warns of Minsky Moment for monetary policy

BoE Chief Economist Andy Haldane said he in a speech he expected UK inflation to be “near 4% than 3%” by the end of this year. “This increases the chances of a high inflation narrative becoming the dominant one, a central expectation rather than a risk.” Inflation expectations would then “shift upward”.

“We would experience a Minsky Moment for monetary policy, a taper tantrum without the taper,” he warned “This would leave monetary policy needing to play catch-up to re-anchor inflation expectations through materially larger and/or faster interest rate rises than are currently expected.”

Different from the Global Financial Crisis, he said “time that policy script feels stretched.”. And, “the pace of recovery is significantly faster now than then, bouncing rather than edging back.” He warned, “a slow exit risks putting central bank balance sheets on an unsustainable footing”.

Overall, Haldane said, “in my view it does, however, call for immediate thought, and action, on unwinding the QE currently being provided, given the state of the economy and central banks’ balance sheets.”

UK Q1 GDP finalized at -1.6% qoq, -8.8% below pre-pandemic level

UK Q1 GDP contraction was finalized at -1.6% qoq, revised from first estimate of -1.5% qoq fall. The level of GDP was -8.8% below the pre-pandemic level at Q4 2019.

Services contracted -2.1% qoq, and was at -8.8% below Q4 2019. Production contracted -0.5% qoq, at -3.7% below Q4 2019. Construction grew 2.3% qoq, still -3.7% below pre-pandemic levels.

Also released, current account deficit narrowed to GBP -12.8B in Q1, versus expectation of GBP -13.8B.

Eurozone CPI slowed to 1.9% in Jun, core CPI ticked down to 0.9%

Eurozone CPI slowed to 1.9% yoy in June, down from 2.0% yoy, matched expectations. Core CPI closed to 0.9% yoy, down from 1.0% yoy, matched expectations.

Looking at the main components, energy is expected to have the highest annual rate in June (12.5%, compared with 13.1% in May), followed by non-energy industrial goods (1.2%, compared with 0.7% in May), services (0.7%, compared with 1.1% in May) and food, alcohol & tobacco (0.6%, compared with 0.5% in May).

France consumer spending rose 10.4% mom in May, close to pre-pandemic average

France consumer spending rose sharply by 10.4% mom in May, above expectation of 8.9% mom, more than enough to reverse -8.7% mom decline in April on return to lockdown. The rebound was mainly driven by manufactured goods purchases (+26.0%), with the reopening of all stores on May 19, and to a lesser extent by spending on energy (+2.6% after a stability), with the end of travel restrictions in early May. Food consumption was stable. Spending in May was at a level near to the average of Q4 2019, just down -0.3%.

Also released, CPI came in at 0.2% mom, 1.9% yoy in June, versus expectation of 0.2% mom, 1.8% yoy.

Swiss KOF dropped to 133.4, prospects remains very positive

Swiss KOF economic barometer dropped to 133.4 in June, down from all-time high at 143.7, missed expectation of 145.3. The barometer still lies well above its long-term average. KOF added, “the prospects for the Swiss economy remains very positive, provided that the economy is not severely affected by a renewed spread of the virus.”

China PMI manufacturing dropped to 50.9 in Jun, PMI non-manufacturing dropped to 53.5

China official PMI Manufacturing dropped slightly to 50.9 in June, down from 51.0, above expectation of 50.7. Production index dropped from 52.7 to 51.9, hitting a four-month low. Total new orders rose from 51.3 to 51.5. But new export orders dropped further from 48.3 to 48.1. Raw material costs eased from 72.8 to 61.2, after the government’s crackdown on prices.

PMI Non-Manufacturing dropped to 53.5, down from 55.2, below expectation of 50.7.

New Zealand ANZ business confidence dropped to -0.6, enormous cost pressures

New Zealand ANZ business confidence dropped to -0.6 in June, down from May’s 1.8. Own activity outlook rose to 31.6, up form 27.1. Looking at some details, export intentions rose form 12.2 to 13.4. Investment intentions rose from 18.9 to 25.5. Cost expectations rose from 81.3 to 86.2. Employment intentions dropped from 20.5 to 19.7. Pricing intentions rose from 57.4 to 62.8. Inflation expectation jumped further from 2.22% to 2.41%.

ANZ said: “The New Zealand economy is stretched, and firms are clearly facing enormous cost pressures. Increasingly, they are planning on raising their prices in response, with little fear evident that demand will collapse as a result. Shortages of labour are driving investment decisions to a greater extent, but it’s confidence in the economic outlook that will always be key here.

With firms keen to invest and employ, and both cost-push and demand-pull factors suggesting strong inflation ahead, it’s past time to unwind the emergency OCR stimulus. We are forecasting the RBNZ to raise the OCR in February next year, but odds are rising that we’ll see hikes this year.”

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9190; (P) 0.9212; (R1) 0.9233; More….

USD/CHF’s break of 0.9237 suggests resumption of rise from 0.8925. Intraday bias is back on the upside for 61.8% retracement of 0.9471 to 0.8925 at 0.9262. Sustained break there will pave the way to retest 0.9471 resistance. On the downside, however, break of 0.9141 minor support will turn bias to the downside for retesting 0.8925 low instead.

{kind=link}

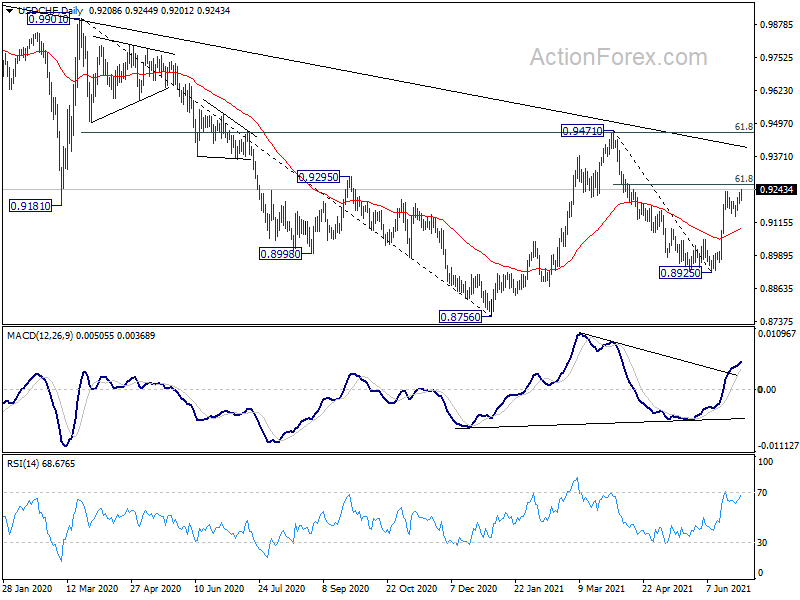

In the bigger picture, medium term outlook is currently neutral with focus on 0.9471 resistance. Sustained break there will indicate completion of whole decline from 1.0342 (2016 high). Medium term outlook will be turned bullish for a test on 1.0342 high. But, rejection by 0.9471 again will revive bearishness for another fall through 0.8756 low.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Shop Price Index Y/Y May | -0.70% | -0.60% | ||

| 23:50 | JPY | Industrial Production M/M May P | -5.90% | -1.90% | 2.90% | |

| 01:00 | CNY | Manufacturing PMI Jun | 50.9 | 50.7 | 51 | |

| 01:00 | CNY | Non-Manufacturing PMI Jun | 53.5 | 55.5 | 55.2 | |

| 01:00 | NZD | ANZ Business Confidence Jun F | -0.6 | -0.4 | ||

| 01:30 | AUD | Private Sector Credit M/M May | 0.40% | 0.10% | 0.20% | 0.30% |

| 05:00 | JPY | Housing Starts Y/Y May | 9.90% | 8.30% | 7.10% | |

| 05:00 | JPY | Consumer Confidence Index Jun | 37.4 | 35.6 | 34.1 | |

| 06:00 | GBP | GDP Q/Q Q1 F | -1.60% | -1.50% | -1.50% | |

| 06:00 | GBP | Current Account (GBP) Q1 | -12.8B | -13.8B | -26.3B | |

| 06:45 | EUR | France CPI M/M Jun P | 0.20% | 0.20% | 0.30% | |

| 06:45 | EUR | France CPI Y/Y Jun P | 1.90% | 1.80% | 1.80% | |

| 06:45 | EUR | France Consumer Spending M/M May | 10.40% | 8.90% | -8.30% | -8.70% |

| 07:00 | CHF | KOF Leading Indicator Jun | 133.4 | 145.3 | 143.2 | 143.7 |

| 07:55 | EUR | Germany Unemployment Change Jun | -38K | -16K | -15K | -19K |

| 07:55 | EUR | Germany Unemployment Rate Jun | 5.90% | 5.90% | 6.00% | 5.90% |

| 08:00 | CHF | Credit Suisse Economic Expectations Jun | 51.3 | 72.2 | ||

| 09:00 | EUR | Eurozone CPI Y/Y Jun P | 1.90% | 1.90% | 2.00% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun P | 0.90% | 0.90% | 1.00% | |

| 12:15 | USD | ADP Employment Change Jun | 692K | 600K | 978K | |

| 12:30 | CAD | GDP M/M Apr | -0.30% | -0.80% | 1.10% | |

| 12:30 | CAD | Industrial Product Price M/M May | 2.70% | 3.00% | 1.60% | |

| 12:30 | CAD | Raw Material Price Index May | 3.20% | 2.10% | 1.00% | |

| 13:45 | USD | Chicago PMI Jun | 70.2 | 75.2 | ||

| 14:00 | USD | Pending Home Sales M/M May | 0.00% | -4.40% | ||

| 14:30 | USD | Crude Oil Inventories | -4.2M | -7.6M |