Sterling Firm, Dollar Mixed, as Focus Turns to FOMC

Asian markets continue to trade in risk averse mode today but selling has somewhat decelerated. Commodity currencies remain the weakest ones for the weak on risk-off sentiment, while Aussie is ignoring stronger than expected inflation reading. Yen and Swiss Franc are both strong, but they were outshone by Sterling. The Pound is supported by IMF’s forecast upgrade on UK. Meanwhile, Dollar and Euro are mixed as focus now turns to FOMC meeting, which is unlikely to reveal something new at this stage.

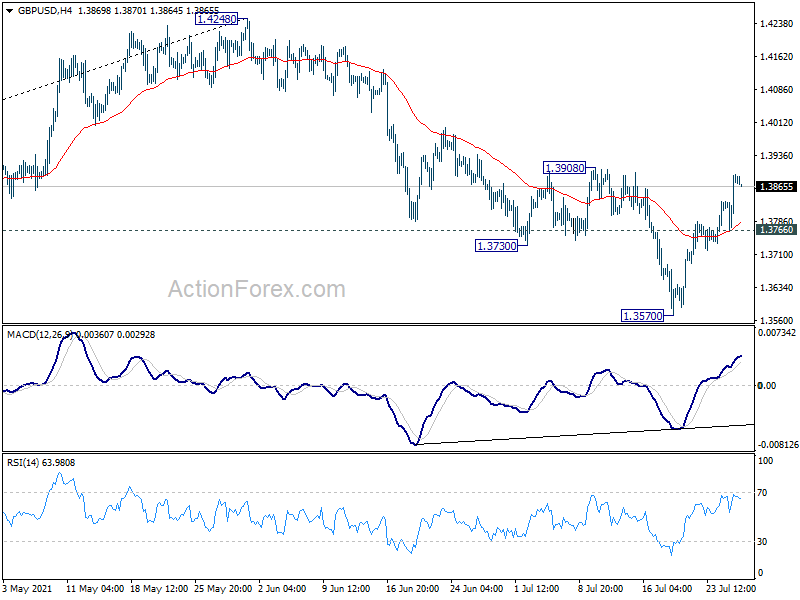

Technically, 1.3908 resistance in GBP/USD is an immediate focus. Firm break there will suggest completion of fall from 1.4248 and retest of this high could be seen next. If that happens, we’d keep an eye on 1.1880 resistance in EUR/USD as well as 0.9116 support in USD/CHF. Break of these levels will affirm Dollar’s weakness, compared to European majors at least.

In Asia, at the time of writing, Nikkei is down -1.71%. Hong Kong HSI is down -0.27%. China Shanghai SSE is down -0.65%. Singapore Strait Times is down -0.46%. Japan 10-year JGB yield is down -0.0059 at 0.014. Overnight, DOW dropped -0.24%. S&P 500 dropped -0.47%. NASDAQ dropped -1.21%. 10-year yield dropped -0.042 to 1.234.

BoJ opinions: Important not to tighten prematurely

In the Summary of Opinions of July 15-16 meeting, BoJ noted that it should “continue to support financing, mainly of firms, and maintain stability in financial markets by conducting monetary easing through the three measures”

Even though core CPI is likely to increase on the back of rise in commodity prices, there is “a long way to go” to achieve target in a stable manner. Hence, it is “important not to tighten monetary policy prematurely”. Also, the “deflationary mindset is strongly entrenched in Japan”.

Australia CPI rose 0.8% qoq, 3.8% yoy in Q2

Australia CPI rose 0.8% in Q2, slightly above expectation of 0.7% qoq. Annual rate accelerated to 3.8% yoy, up from 1.1% yoy, matched expectations. RBA trimmed mean CPI came in at 0.5% qoq, 1.6% yoy. RBA weighted mean CPI was at 0.5% qoq, 1.7% yoy.

Head of Prices Statistics at the ABS, Michelle Marquardt said: “Rising fuel prices accounted for much of the increase in the June quarter CPI, with prices surpassing pre-pandemic levels”.

“The annual CPI movement was significantly influenced by COVID-19 related price changes from this time last year… These ‘base effects’ led to a sharp increase in the annual CPI movement”, she added. “In situations such as this, it is useful to consider underlying inflation measures such as the trimmed mean, which are designed to remove large, one-off price impacts”.

Fed to hold the cards of tapering to chest

FOMC is widely expected to keep monetary policy unchanged today. Without new economic projections, the focus will be on the policy statement and press conference. In particular, Fed Chari Jerome Powell would likely just reiterate that the Committee is in talks of QE tapering. Yet, it is premature to make any conclusion.

Also, more information about policy changes will be revealed at the Jackson Hole symposium in late August, followed by the September meeting. The formal announcement of tapering could indeed be made in December.

Some suggested readings on Fed:

Elsewhere

Germany Gfk consumer sentiment and Swiss ZEW expectations will be released in European session. US will also release goods trade balance and wholesale inventories. Canada will release CPI.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3799; (P) 1.3847; (R1) 1.3926; More….

Focus remains on 1.3908 resistance in GBP/USD. Decisive break there will indicate that fall from 1.4248 has completed. Intraday bias will be turned back to the upside for retesting this high. On the downside, below 1.3766 minor support will turn bias to the downside for 1.3570. Break there will resume the fall from 1.4248 to 1.3482 resistance turned support.

{kind=link}

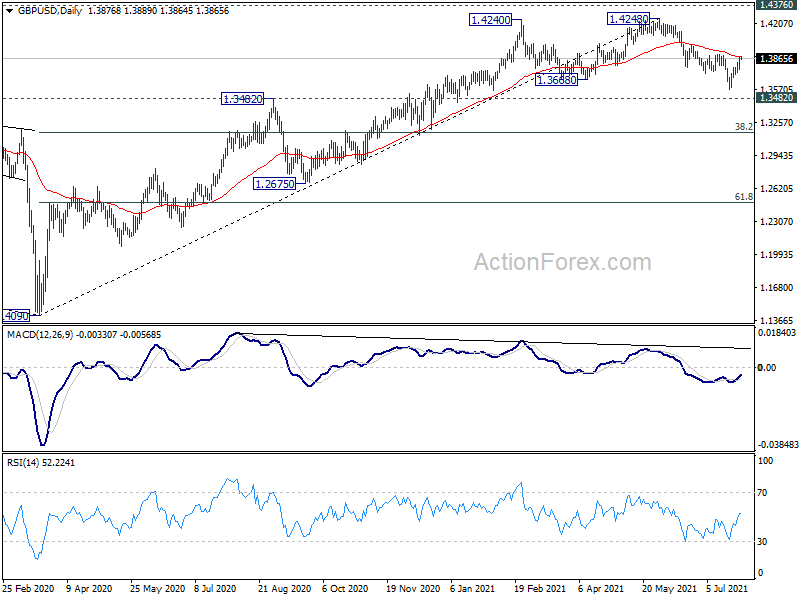

In the bigger picture, as long as 1.3482 resistance turned support holds, up trend from 1.1409 should still continue. Decisive break of 1.4376 resistance will carry larger bullish implications. However, firm break of 1.3482 support will argue that the rise from 1.1409 has completed. GBP/USD would then be seen in another leg of long term range pattern between 1.1409 and 1.4376. Deeper fall could then be seen to 61.8% retracement of 1.1409 to 1.4248 at 1.2493, and even below.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Shop Price Index Y/Y Jun | -1.20% | -0.70% | ||

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 01:30 | AUD | CPI Q/Q Q2 | 0.80% | 0.70% | 0.60% | |

| 01:30 | AUD | CPI Y/Y Q2 | 3.80% | 3.80% | 1.10% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q2 | 0.50% | 0.50% | 0.30% | 0.40% |

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q2 | 1.60% | 1.60% | 1.10% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence Aug | 0.9 | -0.3 | ||

| 08:00 | CHF | ZEW Expectations Jul | 51.3 | |||

| 12:30 | USD | Goods Trade Balance (USD) Jun P | -88.0B | -88.1B | ||

| 12:30 | USD | Wholesale Inventories Jun P | 1.20% | 1.30% | ||

| 12:30 | CAD | CPI M/M Jun | 0.40% | 0.50% | ||

| 12:30 | CAD | CPI Y/Y Jun | 3.50% | 3.60% | ||

| 12:30 | CAD | CPI – Core M/M Jun | 0.40% | |||

| 12:30 | CAD | CPI Common Y/Y Jun | 1.90% | 1.80% | ||

| 12:30 | CAD | CPI Median Y/Y Jun | 2.30% | 2.40% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Jun | 2.60% | 2.70% | ||

| 14:30 | USD | Crude Oil Inventories | -2.6M | 2.1M | ||

| 18:00 | USD | Fed Rate Decision | 0.25% | 0.25% | ||

| 18:30 | USD | FOMC Press Conference |