Yen and Dollar Recovering as Asian Stocks Weighed Down by Evergrande

While DOW hit new intraday record high overnight, positive sentiment was not carried forward to Asia. Instead, stocks tumbled as the troubled China’s property giant Evergrande failed to close the sale of the controlling stake in its property management business. The company could official go into default next Monday. Yen and Dollar are both recovering mildly while commodity currencies retreat. But overall, there is no change in the near term trend yet. Dollar and Yen remain the worst performing ones for the week while Kiwi and Aussie are the strongest.

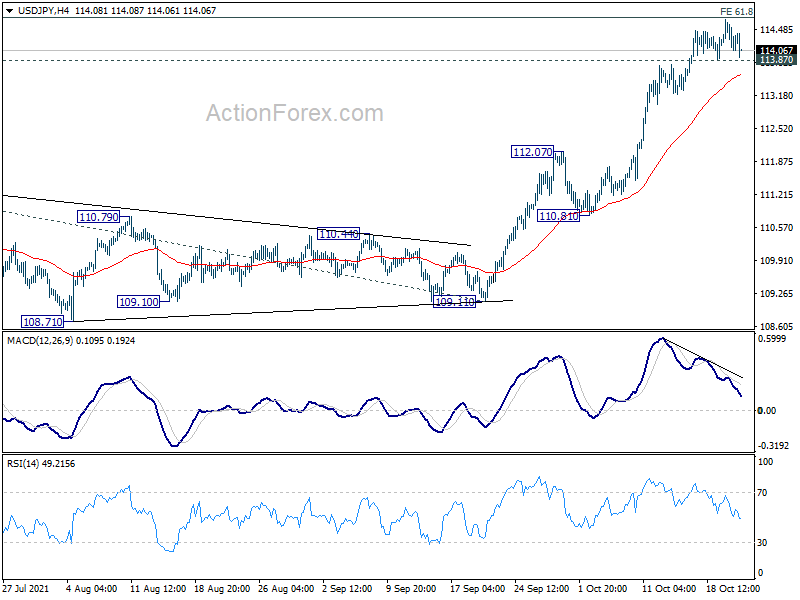

Technically, we’d continue to focus on 113.87 minor support in USD/JPY. Break there will indicate short term topping, after just missing 114.71 fibonacci projection level. USD/JPY would then turn into a near term corrective fall. At the same time, break of 156.58 minor support in GBP/JPY and 132.13 support in EUR/JPY would confirm that the selloff in Yen is over for the near term, and some consolidations would be in Yen crosses in general.

{kind=link}

In Asia, at the time of writing, Nikkei is down -1.48%. Hong Kong HSI is down -0.29%. China Shanghai SSE is up 0.46%. Singapore Strait Times is down -0.01%. Japan 10-year JGB yield is down -0.001 at 0.094. Overnight, DOW rose 0.43%. S&P 500 rose 0.37%. NASDAQ dropped -0.05%. 10-year yield rose 0.001 to 1.636.

Fed Quarles quite wary of further increases in inflation expectations

Fed Governor Randal Quarles said in a speech, “we have met the test of substantial further progress toward both our employment and our inflation mandates”. He would “support a decision at our November meeting to start reducing these purchases and complete that process by the middle of next year”.

He said Fed is not behind the curve on inflation, for three reasons: “Most of the biggest drivers of the very high current inflation rates will ease in coming quarters, some measures of underlying inflation pressures are less worrisome, and longer-term inflation expectations are anchored, at least for now”.

But, “forecast for growth and uncertainty about the resolution of supply constraints mean that there are upside risks to inflation next year.. Hence, his focus is “beginning to turn more fully from the rapidly improving labor market to whether inflation begins its descent toward levels that are more consistent with our price-stability mandate.”

“I would also be quite wary of further increases in inflation expectations in this environment,” Quarles said, “if inflation does remain more than moderately above 2 percent, be assured that the FOMC has the framework and the tools to address it.

Fed Mester: Rate hikes are not coming any time soon

Cleveland Fed President Loretta Mester told CNBC “the thought about raising interest rates is not a near-term consideration at all.” Instead, “we’re going to think about the decision coming up, which is about the asset purchases, and then as those wind down we’ll have time to assess where the economy is.”

“I don’t think that interest rate hikes are coming any time soon because I don’t think we’ll reach our goals which are maximum employment and inflation at and above 2% for some time,” Mester said.

“So far the medium-run inflation expectations and longer-run inflation expectations are still at levels consistent with our 2% inflation goal,” she said. “We don’t want to get into a situation where they continue to move up because that would be a signal that we may have to do an adjustment.”

Australia NAB business confidence dropped to -1 in Q3

Australia NAB business confidence dropped from Q2’s 18 to -1 in Q3. Current business conditions dropped from 30 to 13. Conditions for the next 3 months dropped from 35 to 8. Conditions for the next 12 months also dropped from 33 to 19. Capex plans for the next 12 months dropped from 37 to 26. Trading conditions dropped from 36 to 16. Profitability dropped from 30 to 11. Employment dropped from 23 to 11.

Alan Oster, NAB Group Chief Economist, “With lockdowns in place for most of Q3, it’s unsurprising to see both business conditions and confidence take a fairly large hit for the quarter… While conditions deteriorated sharply, they didn’t fall to the depths seen during the first lockdowns in 2020.”

“While these survey results confirm the large hit to activity that took place in Q3, we are optimistic for a strong rebound in activity in Q4 and into 2022 and reopening progresses.”

Looking ahead

UK will release public sector net borrowing. Canada will release ADP employment and new housing price index. US will release jobless claims, Philly Fed survey and existing home sales.

AUD/USD Daily Report

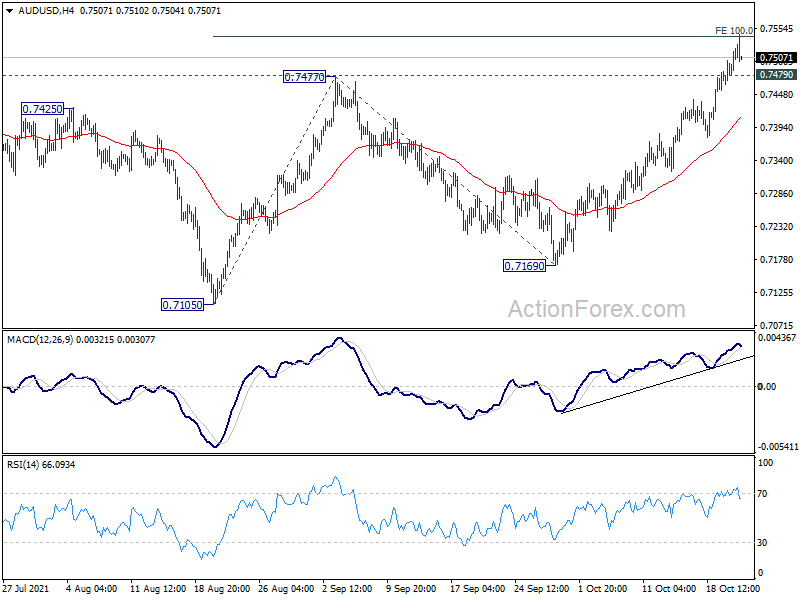

Daily Pivots: (S1) 0.7480; (P) 0.7501; (R1) 0.7538; More…

AUD/USD rises to as high as 0.7545 so far today and met 100% projection of 0.7105 to 0.7477 from 0.7169 at 0.7541. Intraday bias remains on the upside for the moment. Sustained break of 0.7541 will pave the way to 161.8% projection at 0.7771. On the downside, though, break of 0.7479 minor support will turn bias neutral for consolidation first, before staging another rally.

{kind=link}

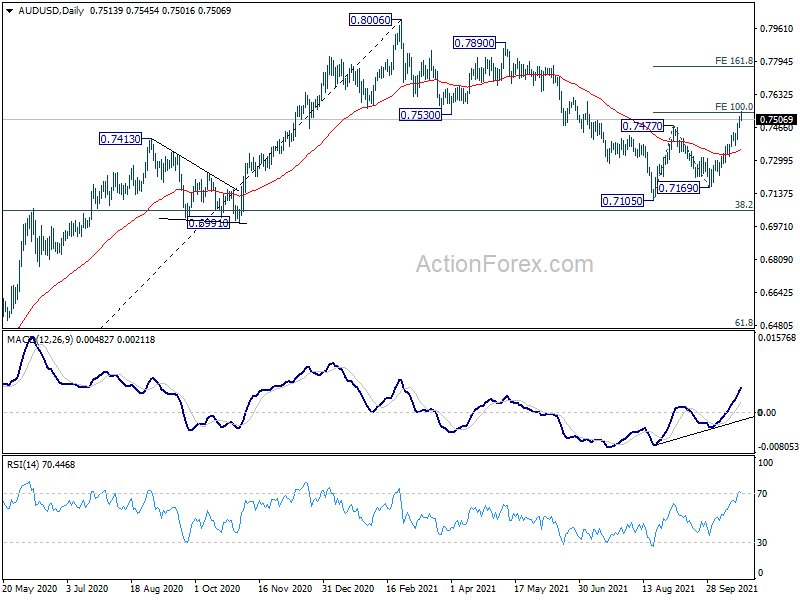

In the bigger picture, with 0.6991 cluster support (38.2% retracement of 0.5506 to 0.8006 at 0.7051) intact, we’re seeing price action from 0.8006 as a correction only. That is, up trend from 0.5506 low would resume after the correction completes. In that case, main focus will be 0.8135 key resistance (2018 high). Sustained break there will carry larger bullish implications. However, sustained break of 0.6991 will argue that the whole medium term trend has indeed reversed.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Q3 | -1 | 17 | 18 | |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Sep | 23.5B | 19.8B | ||

| 12:30 | CAD | ADP Employment Change Sep | 39.4K | |||

| 12:30 | CAD | New Housing Price Index M/M Sep | 0.60% | 0.70% | ||

| 12:30 | USD | Initial Jobless Claims (Oct 15) | 298K | 293K | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Oct | 26 | 30.7 | ||

| 14:00 | USD | Existing Home Sales Sep | 6.00M | 5.88M | ||

| 14:00 | EUR | Eurozone Consumer Confidence Oct P | -5 | -4 | ||

| 14:30 | USD | Natural Gas Storage | -61.0B | 81B |