Euro Mildly Higher after ECB, Dollar Dips Slightly on GDP Miss

Major pairs and crosses are stuck inside yesterday’s range so far, as consolidative trading continues. Euro appears to be lifted slightly by ECB’s press conference but there is no follow through buying. Dollar also looks just a touch weaker after worse than expected Q3 GDP data. Overall, commodity currencies are the softer ones, with eyes on broader risk sentiment.

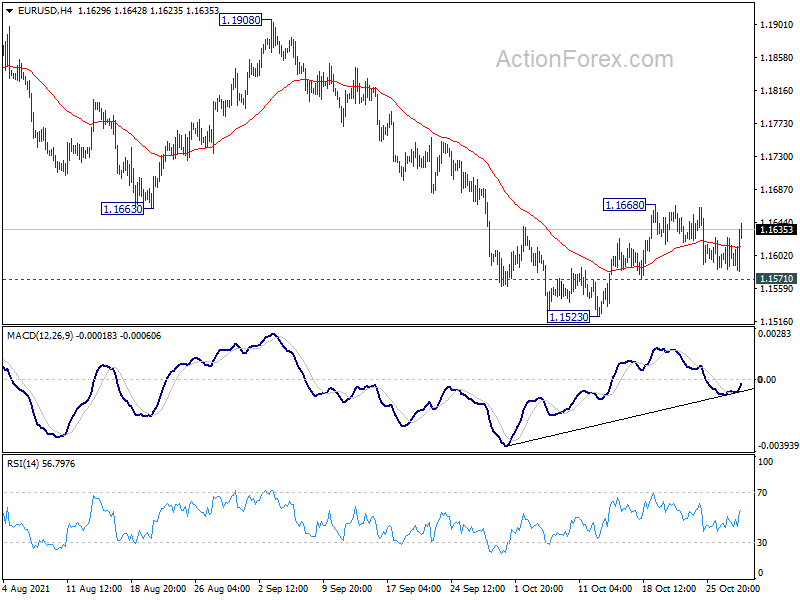

Technically, Euro would be back in focus for the rest of the week. In particular, break of 1.1668 minor resistance in EUR/USD will resume the rebound from 1.1523. Break of 0.8467 minor resistance in EUR/GBP will suggest short term bottoming at 0.8401. Similarly, break of 1.5598 minor resistance in EUR/AUD will also indicate short term bottoming at 1.5393. Break of all these levels will indicate that Euro is at least staging a broad based near term rebound.

In Europe, at the time of writing, FTSE is down -0.30%. DAX is down -0.42%. CAC is up 0.39%. Germany 10-year yield is up 0.064 at -0.112. Earlier in Asia, Nikkei dropped -0.96%. Hong Kong HSI dropped -0.28%. China Shanghai SSE dropped -0.28%. Japan 10-year JGB yield dropped -0.010 to 0.088.

US GDP grew 2.0% annualized in Q3, missed expectations

US GDP grew 2.0% annualized in Q3, below expectation of 2.6%. The increase in real GDP in the third quarter reflected increases in private inventory investment, personal consumption expenditures (PCE), state and local government spending, and nonresidential fixed investment that were partly offset by decreases in residential fixed investment, federal government spending, and exports. Imports, which are a subtraction in the calculation of GDP, increased.

US initial jobless claims dropped to 281k, continuing claims down to 2.24m

US initial jobless claims dropped -10k to 281k in the week ending October 23, slightly better than expectation of 289k. That’s the lowest level since March 14, 2020. Four-week moving average of initial claims dropped -21k to 299k, lowest since March 14, 2020 too.

Continuing claims dropped -237k to 2243k in the week ending October 16, lowest since March 14, 2020. Four-week moving average of continuing claims dropped -142k to 2513k, lowest since March 21, 2020.

ECB stands pat, continues PEPP with moderately lower pace

ECB kept monetary policy unchanged as widely expected. The interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.50% respectively. The forward guidance is maintained.

That is, “the Governing Council expects the key ECB interest rates to remain at their present or lower levels until it sees inflation reaching two per cent well ahead of the end of its projection horizon and durably for the rest of the projection horizon, and it judges that realised progress in underlying inflation is sufficiently advanced to be consistent with inflation stabilising at two per cent over the medium term. This may also imply a transitory period in which inflation is moderately above target.”

PEPP purchases will continue with a total envelop of EUR 1850B, until at least end of March 2022. The pace of net asset purchases will remain “moderately lower” than in Q2 and Q3. APP purchases will continue at a monthly pace of EUR 20B too.

Eurozone economic sentiment indicator rose to 118.6, EU ESI rose to 117.6

Eurozone Economic Sentiment Indicator rose to 118.6 in October, up from 117.8, above expectation of 116.9. Employment Expectations Indicator rose from 113.4 to 114.5. Industrial confidence rose from 14.1 to 14.2. Services confidence rose from 15.2 to 18.2. Consumer confidence dropped from -4.0 to -4.8. Retail trade confidence rose from 1.4 to 2.0. Construction confidence rose from 7.5 to 8.9.

EU ESI rose from 116.6 to 117.6. Amongst the largest EU economies, the ESI rose in Spain (+2.5), France (+2.1), Italy (+1.8), Poland (+1.5) and the Netherlands (+1.4), while it weakened slightly in Germany (-0.5).

From Germany, unemployment rate dropped to 5.4% in October, matched expectations.

BoJ stands pat, downgrades 2021 GDP and CPI forecasts

BoJ kept monetary policy unchanged today as widely expected. Under the yield curve control framework, short-term policy interest rate is held at -0.1%. 10-year yield target is maintained at around 0%, with JGB purchases without upper limit. It also reiterated that BoJ will continue with QQE with YCC “as long as it is necessary” for maintaining inflation at 2% target in a stable manner. It will also continue expanding the monetary base core CPI exceeds 2% and stays above in a stable manner.

Economic projections comparing to July forecast:

- Fiscal 2021 GDP growth downgraded from 3.8% to 3.4%.

- Fiscal 2022 GDP growth upgraded from 2.7% to 2.9%.

- Fiscal 2023 GDP growth unchanged at 1.3%.

- Fiscal 2021 CPI core downgraded from 0.6% to 0.0%.

- Fiscal 2022 CPI core unchanged at 0.9%.

- Fiscal 2023 CPI core unchanged at 1.0%.

BoJ Kuroda: Yen’s recent weakening is definitely positive

In the post meeting press conference, BoJ Governor Haruhiko Kuroda said, “the yen’s recent weakening, as a whole, is definitely positive for Japan’s economy. It’s good for exports and lifts the yen-based profits firms earn overseas. It more than offsets the negative impact from rising import costs.”

“At present, currency rates are moving in line with fundamentals,” he said. “I therefore see no problems with the moves”. He added, “there’s no pre-set norm on the desirable level of real, effective exchange rates. I won’t comment on specific levels.”

“In the long run, if growth accelerates and the output gap turns positive, we’ll likely see inflation accelerate and heighten inflation expectations,” Kuroda said. “Under current conditions, there are more merits than demerits in maintaining ultra-loose monetary policy.”

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1583; (P) 1.1605; (R1) 1.1624; More…

EUR/USD recovers today but stays below 1.1668 temporary top. Intraday bias remains neutral first. On the upside, break of 1.1668 will target 55 day EMA (now at 1.1688). Sustained break there will be a sign that larger correction from 1.2348 has completed. Stronger rally would be seen to 1.1908 resistance for confirmation. On the downside, though, break of 1.1571 minor support will turn bias back to the downside for 1.1523 support instead. Break there will resume larger fall from 1.2348.

{kind=link}

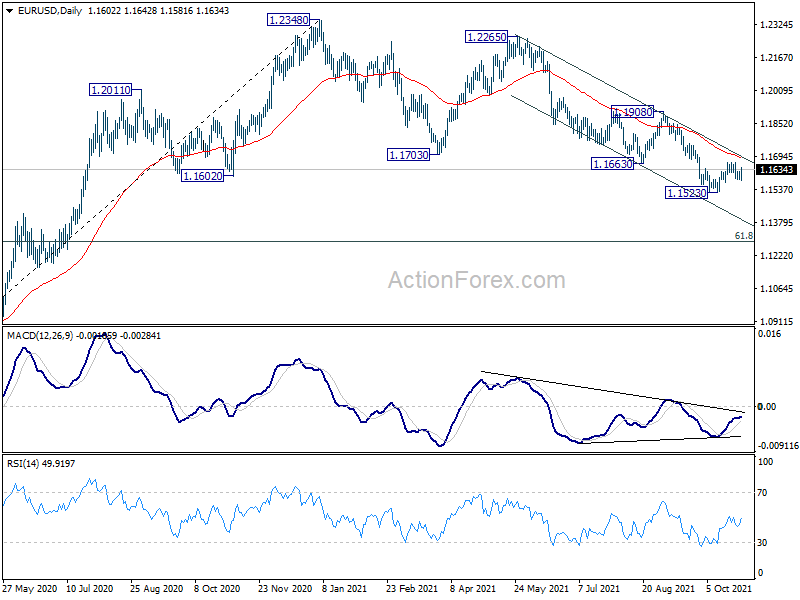

In the bigger picture, price actions from 1.2348 should at least be a correction to rise from 1.0635 (2020 low). As long as 1.1908 resistance holds, deeper fall would be seen to 61.8% retracement of 1.0635 to 1.2348 at 1.1289. Nevertheless break of 1.1908 resistance will revive medium term bullishness and turn focus back to 1.2348 high.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Retail Trade Y/Y Aug | -0.60% | -2.30% | -3.20% | |

| 00:30 | AUD | Import Price Index Q/Q Q3 | 5.40% | 3.60% | 1.90% | |

| 02:45 | JPY | BoJ Rate Decision | -0.10% | -0.10% | -0.10% | |

| 07:55 | EUR | Germany Unemployment Rate Oct | 5.40% | 5.40% | 5.50% | |

| 07:55 | EUR | Germany Unemployment Change Oct | -39K | -20K | -30K | |

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Oct | 118.6 | 116.9 | 117.8 | |

| 09:00 | EUR | Eurozone Services Sentiment Oct | 18.2 | 16.5 | 15.1 | 15.2 |

| 09:00 | EUR | Eurozone Industrial Confidence Oct | 14.2 | 12.5 | 14.1 | |

| 09:00 | EUR | Eurozone Consumer Confidence Oct F | -4.8 | -4.8 | -4.8 | -4 |

| 11:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | 0.00% | |

| 12:00 | EUR | Germany CPI M/M Oct P | 0.50% | 0.50% | 0.00% | |

| 12:00 | EUR | Germany CPI Y/Y Oct P | 4.50% | 4.40% | 4.10% | |

| 12:30 | EUR | ECB Press Conference | ||||

| 12:30 | USD | Initial Jobless Claims (Oct 22) | 281K | 289K | 290K | |

| 12:30 | USD | GDP Annualized Q3 P | 2.00% | 2.60% | 6.70% | |

| 12:30 | USD | GDP Price Index Q3 P | 5.70% | 5.30% | 6.10% | |

| 14:00 | USD | Pending Home Sales M/M Sep | 2.10% | 8.10% | ||

| 14:30 | USD | Natural Gas Storage | 86B | 92B |