Sterling Jumps on Strong CPI, Euro Selloff Continues

Sterling jumps broadly today after much stronger than expected consumer inflation data, that raises the chance that BoE will “have to act” on interest rates soon. On the other hand, Canadian Dollar shrugs off strong, but inline with expectation CPI. Dollar is still among the strongest for the week, but it’s apparently taking a breather for now. On the other hand, Euro is the worst performing, on expectation that ECB will lag behind other central banks in stimulus removal.

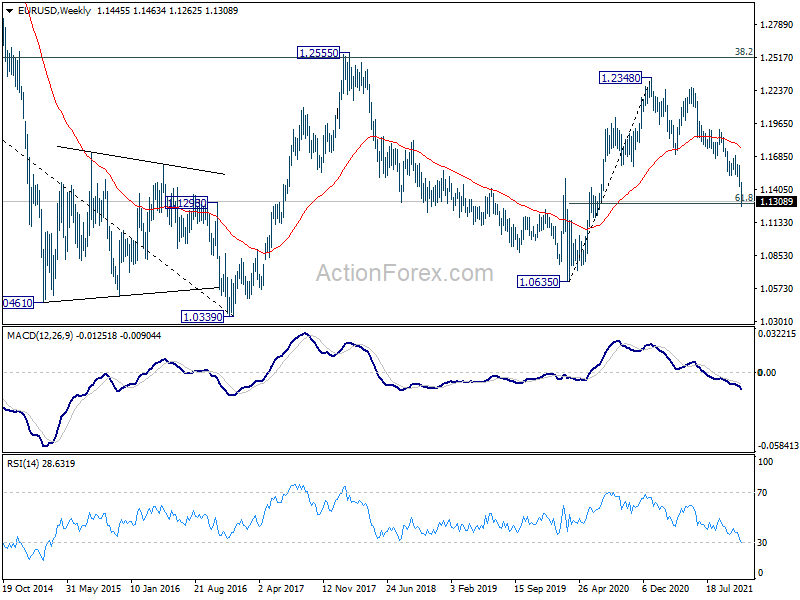

Technically, we’d continue to focus on EUR/USD’s reaction to 1.1289 long term fibonacci support. Sustained trading below this level will carry larger bearish implication and would bring even deeper down trend to 1.0635 (2020 low). Nevertheless, rebound from current level, followed by break of 1.1384 minor resistance, will indicate that selling pressure has eased, at least temporarily. And EUR/USD would then start to build a bottom.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.42%. DAX is up 0.11%. CAC is up 0.06%. Germany 10-year yield is up 0.0036 at -0.237. Earlier in Asia, Nikkei dropped -0.40%. Hong Kong HSI dropped -0.25%. China Shanghai SSE rose 0.44%. Singapore Strait Times dropped -0.19%. Japan 10-year JGB yield dropped -0.0012 to 0.074.

Canada CPI accelerated to 4.7% yoy in Oct, highest since 2003

Canada CPI accelerated to 4.7% yoy in October, up from September’s 4.4% yoy, matched expectations. That’s the highest reading since February 2003. Excluding energy, CPI rose 3.3% yoy, unchanged from September’s reading. On a monthly basis CPI rose 0.7% mom, largest gains since June 2020.

CPI common was unchanged at 1.8% yoy, below expectation of 1.9% yoy. CPI median rose to 2.9% yoy, up from 2.8% yoy, matched expectations. CPI trimmed slowed to 3.3% yoy, down from 3.4% yoy, below expectation of 3.4% yoy.

From US, building permits rose to 1.65m annualized rate in October, above expectation of 1.63m. Housing starts dropped to 1.52m, below expectation of 1.58m.

UK CPI surged to 4.2% yoy in Oct, highest since 2011

UK CPI surged to 4.2% yoy in October, up from 3.1% yoy, above expectation of 3.8% yoy. That’s the highest level in nearly 10 years since November 2011. Core CPI also jumped to 3.4% yoy, up from 2.9% yoy, above expectation of 3.0% yoy. RPI also accelerated to 6.0% yoy, up from 4.9% yoy, above expectation of 5.6% yoy.

PPI input came in at 1.4% mom, 13.0% yoy, versus expectation of 1.1% mom, 11.6% yoy. PPI output was at 1.1% mom, 8.0% yoy, versus expectation of of 0.7% mom, 6.8% yoy. PPI core output was at 0.8% mom, 6.5% yoy, matched expectations.

Eurozone CPI finalized at 4.1% yoy in Oct, EU at 4.4%

Eurozone CPI was finalized at 4.1% yoy in October, up from September’s 3.4%. The highest contribution came from energy (+2.21%), followed by services (+0.86%), non-energy industrial goods (+0.55%) and food, alcohol & tobacco (+0.43%).

EU CPI was finalized at 4.4%, up from September’s 3.6% yoy. The lowest annual rates were registered in Malta (1.4%), Portugal (1.8%), Finland and Greece (both 2.8%). The highest annual rates were recorded in Lithuania (8.2%), Estonia (6.8%) and Hungary (6.6%). Compared with September, annual inflation rose in all twenty-seven Member States.

Japan exports growth slowed to 9.4% yoy on fall in car shipments

Japan exports rose 9.4% yoy to JPY 7.18B in October. That was the slowest expansion since a decline in February. By region, exports to China rose 9.5% yoy, slowed from 10.3% yoy in the prior month, on -46.8% yoy fall in car shipments. Exports to US grew just 0.4% yoy, also weighed down by -46.4% yoy fall in car exports. Imports rose 26.7% yoy to JPY 7.25B. Trade balance came at as JPY -0.07B deficit

In seasonally adjusted terms exports rose 2.7% mom to JPY 6.93B while imports rose 0.3% mom to JPY 7.38B. Trade deficit came in at JPY -0.44B.

Also from Japan, machine orders rose 0.0% mom in September, versus expectation of 1.8% mom.

Australia wage price index rose 0.6% qoq in Q3

Australia wage price index rose 0.6% qoq 2.2% yoy in Q3. Private sector rose 0.6% qoq, 2.4% yoy. Public sector rose 0.5% qoq, 1.7% yoy. The three largest states were the main contributors to growth, New South Wales, Victoria, and Queensland. The most significant industries to contribute to growth this quarter were the Professional, scientific and technical services, Health care and social assistance and Construction industries.

Westpac leading index rose 0.20% mom in October.

From New Zealand, PPI input rose 1.6% qoq in Q3, versus expectation of 1.7% qoq. PPI output rose 1.8% qoq, versus expectation of 1.4% qoq.

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8410; (P) 0.8447; (R1) 0.8466; More…

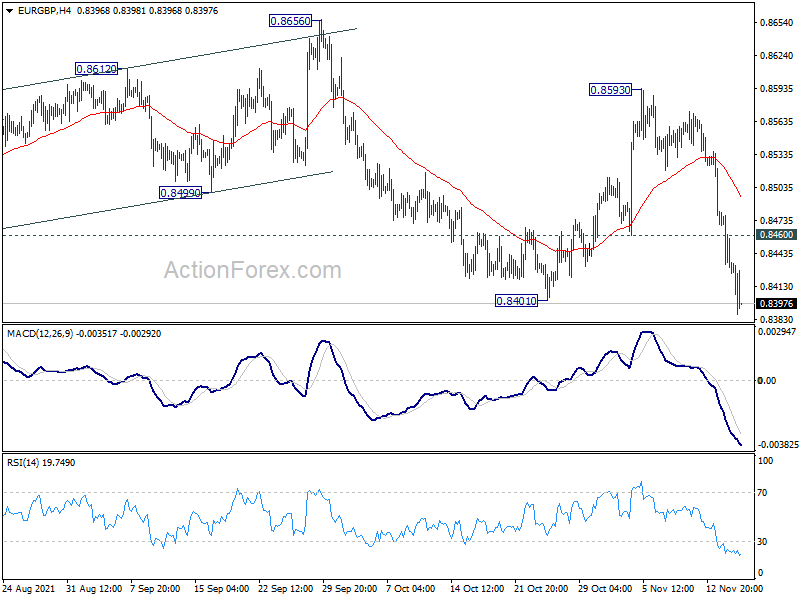

EUR/GBP’s break of 0.8401 support indicates resumption of larger down trend from 0.9499. Intraday bias stays on the downside. Deeper fall would now be seen towards 0.8276 long term support next. On the upside, however, break of 0.8460 minor resistance will delay the bearish case and turn intraday bias neutral first.

{kind=link}

In the bigger picture, price actions from 0.9499 (2020 high) are still seen as developing into a corrective pattern. Deeper fall could be seen as long as 0.8656 resistance holds, towards long term support at 0.8276. However, firm break of 0.8656 resistance would argue that a medium term bottom was already formed. Stronger rise would be seen to 0.8861 support turned resistance to confirm completion of the corrective pattern.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | PPI Input Q/Q Q3 | 1.60% | 1.70% | 3.00% | |

| 21:45 | NZD | PPI Output Q/Q Q3 | 1.80% | 1.40% | 2.60% | |

| 23:30 | AUD | Westpac Leading Index M/M Oct | 0.20% | 0.00% | ||

| 23:50 | JPY | Machinery Orders M/M Sep | 0.00% | 1.80% | -2.40% | |

| 00:30 | AUD | Wage Price Index Q/Q Q3 | 0.60% | 0.50% | 0.40% | |

| 07:00 | GBP | CPI M/M Oct | 1.10% | 0.80% | 0.30% | |

| 07:00 | GBP | CPI Y/Y Oct | 4.20% | 3.80% | 3.10% | |

| 07:00 | GBP | Core CPI Y/Y Oct | 3.40% | 3.00% | 2.90% | |

| 07:00 | GBP | RPI M/M Oct | 1.10% | 1.00% | 0.40% | |

| 07:00 | GBP | RPI Y/Y Oct | 6.00% | 5.60% | 4.90% | |

| 07:00 | GBP | PPI Input M/M Oct | 1.40% | 1.10% | 0.40% | 0.80% |

| 07:00 | GBP | PPI Input Y/Y Oct | 13.00% | 11.60% | 11.40% | 11.90% |

| 07:00 | GBP | PPI Output M/M Oct | 1.10% | 0.70% | 0.50% | 0.70% |

| 07:00 | GBP | PPI Output Y/Y Oct | 8.00% | 6.80% | 6.70% | 7.00% |

| 07:00 | GBP | PPI Core Output M/M Oct | 0.70% | 0.70% | 0.50% | 0.60% |

| 07:00 | GBP | PPI Core Output Y/Y Oct | 6.50% | 6.50% | 5.90% | 6.00% |

| 10:00 | EUR | Eurozone CPI Y/Y Oct F | 4.10% | 4.10% | 4.10% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Oct F | 2.00% | 2.10% | 2.10% | |

| 13:30 | CAD | CPI M/M Oct | 0.70% | 0.70% | 0.20% | |

| 13:30 | CAD | CPI Y/Y Oct | 4.70% | 4.70% | 4.40% | |

| 13:30 | CAD | CPI Common Y/Y Oct | 1.80% | 1.90% | 1.80% | |

| 13:30 | CAD | CPI Median Y/Y Oct | 2.90% | 2.90% | 2.80% | |

| 13:30 | CAD | CPI Trimmed Y/Y Oct | 3.30% | 3.40% | 3.40% | |

| 13:30 | USD | Building Permits Oct | 1.65M | 1.63M | 1.59M | |

| 13:30 | USD | Housing Starts Oct | 1.52M | 1.58M | 1.56M | 1.53M |

| 15:30 | USD | Crude Oil Inventories | 1.0M | 1.0M |