Yen in Weak Recovery, Dollar and Sterling Still Firm

Yen is trying to recover on weaker risk sentiment today. But momentum is relatively soft against Dollar and Europeans. Aussie and Kiwi follow broader risk markets lower. Sterling and Dollar remain the strongest ones for the week, on expectation of hawkish BoE and Fed. Euro and Swiss Franc are mixed, with Euro having a slight upper handle. Traders could not turn more cautious until tomorrow’s non-farm payrolls report.

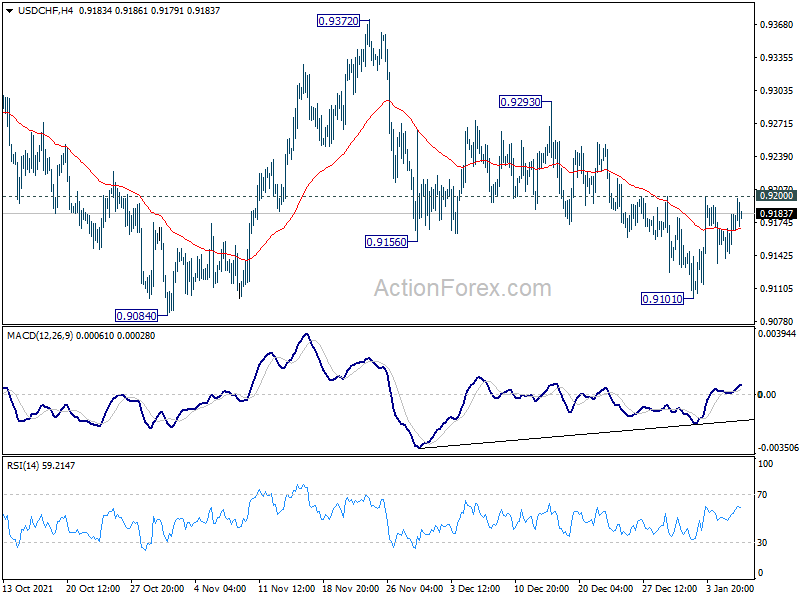

Technically, we’d now pay some attention to USD/CHF. Break of 0.9200 resistance will argue that fall from 0.9372 has completed with three waves down to 0.9101. Stronger rally would be seen to 0.9293 resistance and above. If that happens, it could be a prelude to EUR/USD’s downside range breakout.

{kind=link}

In Europe, at time of writing, FTSE is down -0.76%. DAX is down -1.14%. CAC is down -1.39%. Germany 10-year yield is up 0.0236 at -0.099. Earlier in Asia, Nikkei dropped -2.88%. Hong Kong HSI rose 0.72%. China Shanghai SSE dropped -0.25%. Singapore Strait Times rose 0.66%. Japan 10-year JGB yield rose 0.0323 to 0.119.

US initial claims rose to 207k, above expectation

US initial jobless claims rose 7k to 207k in the week ending January 1, above expectation of 199k. Four-week moving average of initial claims rose 5k to 205k. Continuing claims rose 36k to 1754k in the week ending December 25. Four-week moving average of continuing claims dropped -61k to 1799k, lowest since March 14, 2020.

Also, released, US trade deficit widened to USD -80.2B in November, versus expectation of USD -73.5B. Canada trade surplus widened to CAD 3.1B, above expectation of CAD 1.4B.

Eurozone PPI at 1.8% mom, 23.7% in Nov

Eurozone PPI rose 1.8% mom, 23.7% yoy in November, versus expectation of 1.2% mom, 22.9% yoy. For the month, industrial increased by 3.5% in the energy sector, by 1.5% for intermediate goods, by 0.6% for non-durable consumer goods, by 0.5% for durable consumer goods and by 0.4% for capital goods. Prices in total industry excluding energy increased by 0.9%.

EU PPI came in at 2.0% mom, 23.7% yoy. The highest monthly increases in industrial producer prices were recorded in Denmark (+10.3%), Bulgaria (+8.5%) and Romania (+7.3%), while the only decrease was observed in Ireland (-2.5%).

Germany factor orders rose 3.7% mom in Nov, strong foreign orders

Germany factory orders rose 3.7% mom in November, better than expectation of 2.5% mom. Comparing with October, Largest increase in new orders (32.0%) was recorded in the manufacture of other transport equipment (aircraft, ships, trains etc.) for which extensive major orders were reported. New orders in the manufacture of motor vehicles, trailers and semi-trailers were up by 7.0%. Not including major orders, an 3.8% increase in new orders in manufacturing was recorded.

The strong growth in new orders was attributable to foreign orders which increased by 8.0%. New orders from the euro area rose by 13.1%. New orders from other countries amounted to 5.0% in the current month. Domestic orders went up 2.5% in November 2021 on the previous month.

UK PMI services finalized at 53.6, severe loss of momentum

UK PMI Services was finalized at 53.6 in December, down from November’s 58.5, lowest level since February. Markit said export sales were hard-hit by renewed pandemic. Service provides remained upbeat about year ahead prospects. PMI Composite was finalized at 53.6, down from prior month’s 57.6.

Tim Moore, Economics Director at IHS Markit: “December data revealed a severe loss of momentum for the UK economy as many customer-facing businesses experienced a drop in demand due to escalating COVID-19 cases. Total new orders in the service sector increased at the weakest pace for 10 months. Mass cancellations of bookings in response to the Omicron variant led to a slump in consumer spending on travel, leisure and entertainment. Survey respondents also noted that renewed pandemic restrictions had slowed the recovery in business services.

China PMI services rose to 53.1, composite rose to 53.0

China Caixin PMI Services rose from 52.1 to 53.1 in December, above expectation of 51.9. PMI Composite rose from 51.2 to 53.0.

Wang Zhe, Senior Economist at Caixin Insight Group said: “To sum up, the economy recovered in December with improvements in demand and supply of manufacturing and services. Inflationary pressure eased. But the job market was still under pressure and businesses were less optimistic, raising questions about the stability of the economic recovery. The repeated Covid-19 flare-ups and sluggish overseas demand were challenges to stability.”

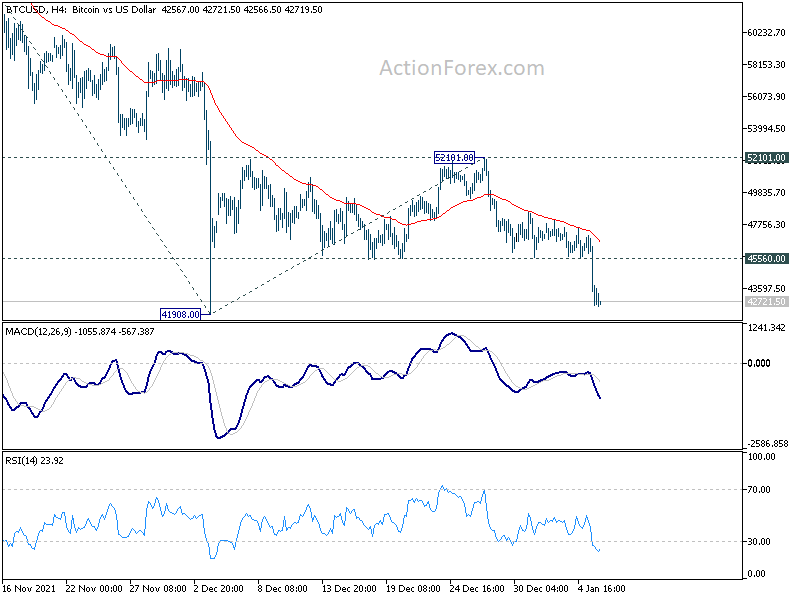

Bitcoin breaking down, 40k might only offer temporary support

Bitcoin finally breaks down and it’s now heading back to 41908 spike low. Prior rejection by 55 day EMA maintains near term bearishness and fall from 68986 is likely resuming. There might be some initial support between 39559/41908, around 40k handle. But outlook will stay bearish as long as 52101 resistance holds.

We’d expect fall form 68986 to hit 61.8% projection of 68986 to 41908 from 52101 at 35366 before finding a bottom.

{kind=link}

{kind=link}

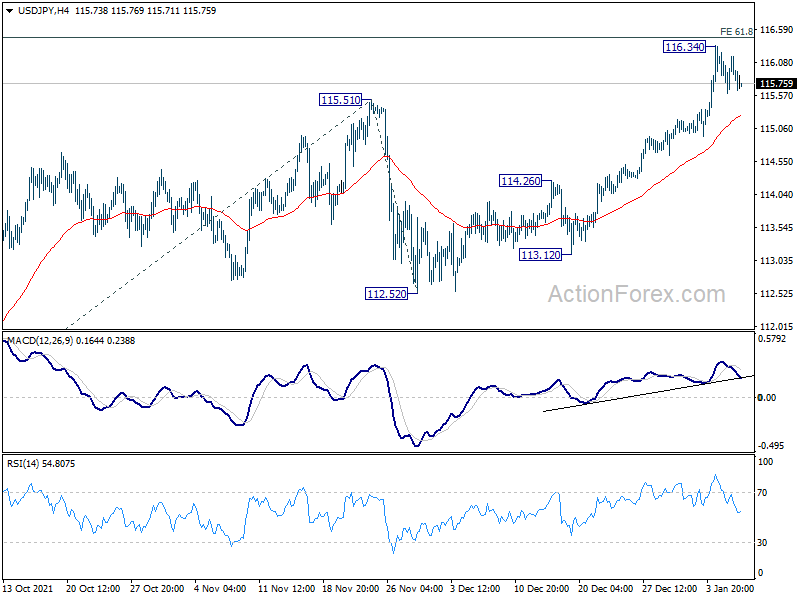

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 115.74; (P) 115.99; (R1) 116.36; More…

USD/JPY is staying in consolidation below 116.34 temporary top and intraday bias remains neutral. Some consolidations could be seen but downside should be contained well above 114.26 support turned resistance to bring another rally. On the upside, sustained break of 61.8% projection of 109.11 to 115.51 from 112.52 at 116.47 will pave the way to 100% projection at 118.90, which is close to 118.65 long term resistance.

{kind=link}

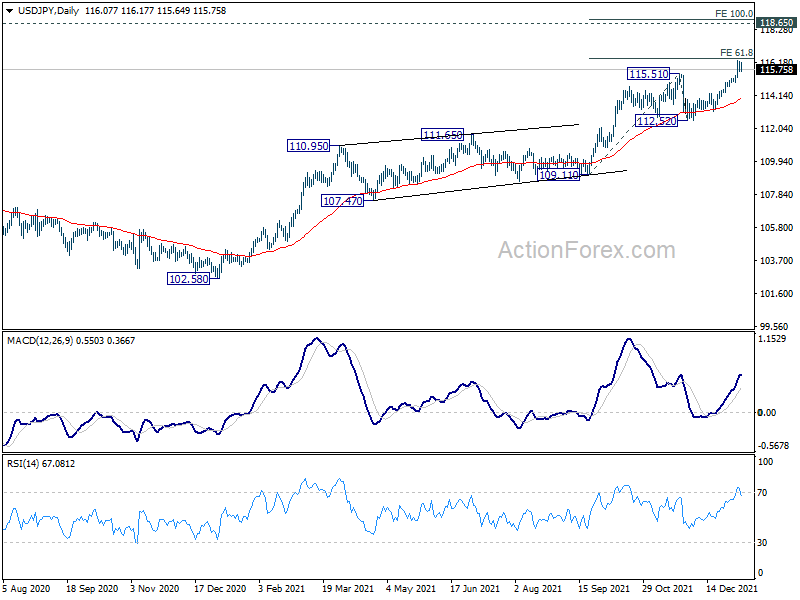

In the bigger picture, no change in the view that rise from 102.58 is the third leg of the up trend from 101.18 (2020 low). Such rally should target a test on 118.65 (2016 high). Sustained break there will pave the way to 120.85 (2015 high) and raise the chance of long term up trend resumption. For now, this will remain the favored case as long as 112.52 support holds, in case of deep pull back.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:45 | CNY | Caixin Services PMI Dec | 53.1 | 51.9 | 52.1 | |

| 07:00 | EUR | Germany Factory Orders M/M Nov | 3.70% | 2.50% | -6.90% | -5.80% |

| 09:30 | GBP | Services PMI Dec F | 53.6 | 53.2 | 53.2 | |

| 10:00 | EUR | Eurozone PPI M/M Nov | 1.80% | 1.20% | 5.40% | |

| 10:00 | EUR | Eurozone PPI Y/Y Nov | 23.70% | 22.90% | 21.90% | |

| 13:00 | EUR | Germany CPI M/M Dec P | 0.50% | 0.40% | -0.20% | |

| 13:00 | EUR | Germany CPI Y/Y Dec P | 5.30% | 5.10% | 5.20% | |

| 13:30 | CAD | Trade Balance (CAD) Nov | 3.1B | 1.4B | 2.1B | 2.3B |

| 13:30 | USD | Initial Jobless Claims (Dec 31) | 207K | 199K | 198K | 200K |

| 13:30 | USD | Trade Balance (USD) Nov | -80.2B | -73.5B | -67.1B | -67.2B |

| 15:00 | USD | ISM Services PMI Dec | 67.2 | 69.1 | ||

| 15:00 | USD | ISM Services Prices Paid Dec | 82.3 | |||

| 15:00 | USD | ISM Services Employment Index Dec | 56.5 | |||

| 15:00 | USD | Factory Orders M/M Nov | 1.50% | 1.00% | ||

| 15:30 | USD | Natural Gas Storage | -55B | -136B |