Yen Reverses Losses on Risk-off Sentiment, Dollar Supported By Yields

Stocks markets are turning back into risk off mode with US futures pointing to sharply lower open. Yen managed to reverse earlier losses and trading generally higher. Canadian Dollar is also firm as supported by extended rally in oil prices. Dollar is following with some lift by rising treasury yields. On the other hand, Sterling is currently the weakest one, weighed down further by selloff against other Europeans. But Aussie and Kiwi are not to far away.

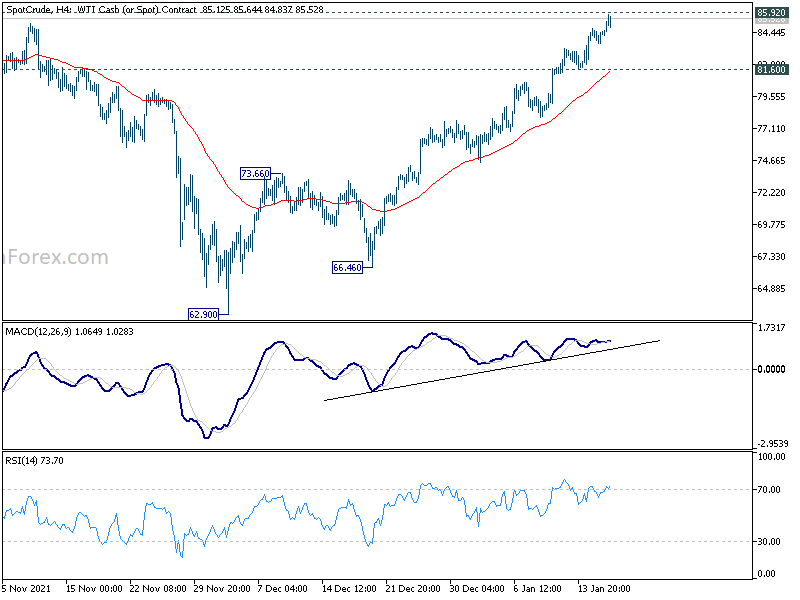

Technically, we’ll pay attention to WTI crude oil today as it’s now pressing 85.92 high. We’re not expecting a decisive break there. Rejection by this resistance, followed by break of 81.60 support, should trigger near term reversal back towards 73.66 resistance turned support. In this case, we could seen Canadian Dollar reverses too with USD/CAD breaking through 1.2619 resistance. However, strong break of 85.92 will give the Loonie another boost, probably pushing EUR/CAD through 1.4162 low.

{kind=link}

In Europe, at the time of writing, FTSE is up 0.50%. DAX is up 0.86%. CAC is up -0.77%. Germany 10-year yield is flat at -0.023. Earlier in Asia, Nikkei dropped -0.27%. Hong Kong HSI dropped -0.43%. China Shanghai SSE rose 0.80%. Singapore Strait Times dropped -0.24%. Japan 10-year JGB yield rose 0.0056 to 0.152.

US Empire state manufacturing dived to -0.7, expectations firm

US Empire State Manufacturing Survey general business conditions index dropped sharply from 31.9 to -0.7 in January. Twenty-two percent of respondents reported that conditions had improved over the month, while 23 percent reported that conditions had worsened. Expectations for the six months ahead ticked down from 36.4 to 35.1.

Looking at some details, new orders dropped from 27.1 to -5.0. Shipments dropped from 27.1 to 1.0. Delivery times dropped slightly from 23.1 to 21.6. Price paid eased from 80.2 to 76.6. Prices received also dropped from 44.6 to 37.1.

Germany ZEW surged to 51.7, economic outlook improved considerably

Germany ZEW Economic Sentiment rose sharply from 29.9 to 51.7 in January, well above expectation of 32.7. Current Situation index deteriorated from -7.4 to -10.2, missed expectation of -7.5.

Eurozone ZEW Economic Sentiment jumped from 26.8 to 49.4, well above expectation of 29.2. Current Situation index dropped -3.9 pts to -6.2.

ZEW President Achim Wambach said: “The economic outlook has improved considerably with the start of the new year. The majority of financial market experts assume that economic growth will pick up in the coming six months. It is likely that the phase of economic weakness from the fourth quarter of 2021 will soon be overcome.

“The main reason for this is the assumption that the incidence of COVID-19 cases will fall significantly by early summer. The more positive economic expectations include the consumer-related and export-oriented sectors and thus a large part of the German economy.”

UK payroll rose 184k in Dec, unemployment rate dropped to 4.1% in Nov

UK payrolled employees rose 184k to 29.5m in December. The number was up 409k on pre-pandemic level back in February 2020. All region are now above pre-coronavirus levels.

For September to November period, comparing to the prior quarter, employment rate rose 0.2% to 75.5%. Unemployment rate dropped -0.4% to 4.1%. Economic inactivity rate rose 0.2% to 21.3%.

Average earnings including bonus rose 4.2% 3moy while average earnings excluding bonuses rose 3.8% 3moy.

BoJ stands pat, upgrades 2022, 2023 inflation forecasts

BoJ left monetary policy unchanged. Under the yield curve control, short-term policy interest rate is held unchanged at -0.1%. BoJ will also buy a “necessary amount” of JGB bonds to keep 10-year yield at around 0%.

BoJ maintained the pledge to continue with QQE with yield curve control, “aiming to achieve the price stability target of 2 percent, as long as it is necessary for maintaining that target in a stable manner”. It will also continue expanding the monetary base “until the year-on-year rate of increase in the observed consumer price index (CPI, all items less fresh food) exceeds 2 percent and stays above the target in a stable manner.”

In the new economic projections, comparing to October forecasts:

- Fiscal 2021 real GDP growth downgraded from 3.4% to 2.8%.

- Fiscal 2022 real GDP growth upgraded from 2.9% to 3.8%

- Fiscal 2023 real GDP growth downgraded from 1.3% to 1.1%.

- Fiscal 2021 core CPI unchanged at 0.0%.

- Fiscal 2022 core CPI upgraded from 0.9% to 1.1%.

- Fiscal 2023 core CPI upgraded from 1.0% to 1.1%.

BoJ Kuroda: We are not debating an interest rate hike

In the post meeting press conference, BoJ Governor Haruhiko Kuroda said, “consumer inflation is likely to stay around 1% through the end of the BoJ’s projection period. As such, there is no need to modify the BoJ’s monetary easing.”

“We are not debating an interest rate hike … As shown in the report, we’re not yet in a situation where inflation is steadily accelerating toward the BoJ’s goal. The median forecast of board members is for inflation around 1%. Under such conditions, we are absolutely not thinking about raising rates or modifying our easy monetary policy,” he said.

“If achievement of 2% inflation comes into sight, the BoJ’s board will likely debate an exit strategy and communicate its intention to markets. That in itself won’t be that difficult. The problem is that unfortunately, we haven’t see inflation hit 2%. It’s premature to debate an exit strategy,” he added.

Downbeat New Zealand business confidence, strong inflation pressures

In the The latest NZIER Quarterly Survey of Business Opinion, a net 34.4% of New Zealand businesses expect a deterioration in general economic conditions over the coming months, much worse than prior quarter’s 11.1%. Trading activity for the next three months dropped slightly from 8.7 to 8.3.

Regarding inflation, a net 61% reported increased costs in Q4, highest since 2008. A net 65% expect further increase in prices in the next quarter. NZIER said, “these results point to inflation pressures in the New Zealand economy remaining strong over the coming year.”

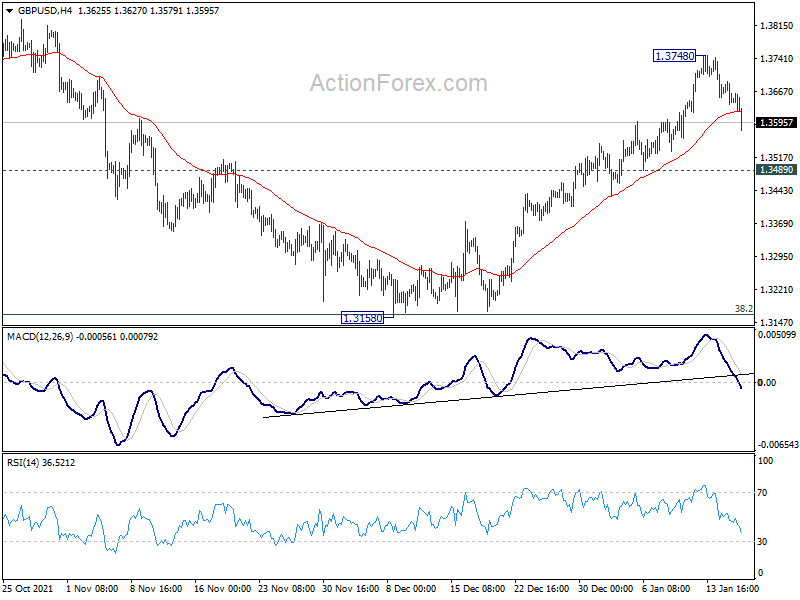

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3624; (P) 1.3657; (R1) 1.3676; More…

GBP/USD’s pull back from 1.3748 extended lower today but stays above 1.3489 support. Outlook is unchanged and intraday bias remains neutral first. Downside of retreat should be contained by 1.3489 support to bring another rally. As noted before, corrective fall from 1.4282 should have completed with three waves down to 1.3158, after hitting 1.3164 medium term fibonacci level. Above 1.3748 will target 1.3833 first. Sustained break of 1.3833 will pave the way back to retest 1.4248 high.

{kind=link}

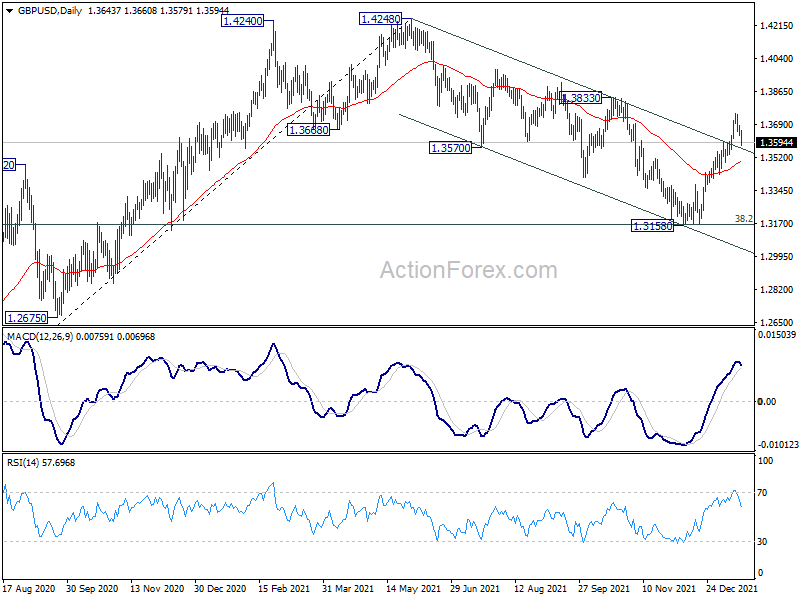

In the bigger picture, strong support was seen from 38.2% retracement of 1.1409 to 1.4248 at 1.3164. The development suggests that up trend from 1.1409 (2020 low) is still in progress. On resumption, next target will be 38.2% retracement of 2.1161 to 1.1409 at 1.5134. Nevertheless sustained break of 1.3164 will argue that whole rise from 1.1409 has completed and bring deeper fall to 61.8% retracement at 1.2493.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | NZIER Business Confidence Q4 | -28 | -11 | ||

| 03:00 | JPY | BoJ Rate Decision | -0.10% | -0.10% | -0.10% | |

| 04:30 | JPY | Industrial Production M/M Nov F | 7.00% | 7.20% | 7.20% | |

| 07:00 | GBP | ILO Unemployment Rate (3M) Nov | 4.10% | 4.20% | 4.20% | |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Nov | 4.20% | 4.20% | 4.90% | |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Nov | 3.80% | 3.80% | 4.30% | |

| 07:00 | GBP | Claimant Count Change Dec | -43.3K | -38.6K | -49.8K | |

| 07:30 | CHF | Producer and Import Prices M/M Dec | -0.10% | 0.40% | 0.50% | |

| 07:30 | CHF | Producer and Import Prices Y/Y Dec | 5.10% | 5.80% | ||

| 09:00 | EUR | Italy Trade Balance (EUR) Nov | 4.16B | 4.23B | 3.89B | |

| 10:00 | EUR | Germany ZEW Economic Sentiment Jan | 51.7 | 32.7 | 29.9 | |

| 10:00 | EUR | Germany ZEW Current Situation Jan | -10.2 | -7.5 | -7.4 | |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Jan | 49.4 | 29.2 | 26.8 | |

| 13:15 | CAD | Housing Starts Dec | 236K | 234K | 301K | |

| 13:30 | USD | Empire State Manufacturing Index Jan | -0.7 | 28 | 31.9 | |

| 15:00 | USD | NAHB Housing Market Index Jan | 84 | 84 |