Sentiment Still Weak Despite Big U-Turn in US Stocks, Dollar Firm With Yen

US stocks staged a strong comeback overnight, with DOW staging the first-ever 1000-point-plus intraday U-turn. It’s down -1100 pts at initially trading but closed up 11 pts eventually. Yet, risk-off sentiment remains dominant in Asia. Dollar is currently the strongest, followed by Yen. Sterling is the worst performer, followed by Kiwi and Loonie. Aussie managed to pare back some losses after much stronger than expected consumer inflation reading. Overall, sentiment would remain vulnerable on developments surrounding Ukraine.

Technically, we’ll keep our eyes on EUR/USD, USD/CHF and USD/JPY, which are still range bound. We’re talking about 1.1284/1482 in EUR/USD, 0.9090/9276 in USD/CHF and 113.47/115.05 in USD/JPY. The breakouts will reveal much about the underlying dynamics in both Dollar and Yen.

In Asia, at the time of writing, Nikkei is down -1.82%. Hong Kong HSI is down -1.32%. China Shanghai SSE is down -1.12%. Singapore Strait Times is down -1.04%. Japan 10-year JGB yield is down -0.005 at 0.134. Overnight, DOW rose 0.29%. S&P 500 rose 0.28%. NASDAQ rose 0.63%. 10-year yield dropped -0.012 to 1.735.

Australia CPI surged to 3.5% yoy in Q4, trimmed mean CPI at 7-yr high

Australia CPI rose 1.3% qoq, 3.5% yoy in Q4, well above expectation of 1.0% qoq, 3.2% yoy. RBA trimmed mean CPI rose 1.0% qoq, 2.6% yoy, also above expectation of 0.7% qoq, 2.4% yoy. The 2.6% yoy rise was the highest since June 2014.

Head of Prices Statistics at the ABS, Michelle Marquardt, said the most significant price rises in the December quarter were new dwellings (+4.2%) and automotive fuel (+6.6%).

Marquardt said: “Annual trimmed mean inflation is the highest since 2014, reflecting the broad-based nature of price increases, particularly for goods.”

Australia NAB business confidence dropped sharply to -12

Australia NAB business confidence dropped sharply from 12 to -12 in December. Business conditions dropped from 11 to 8. Trading conditions was unchanged at 14. Profitability conditions rose from 8 to 10. Employment conditions dropped from 11 to 2.

“Overall, the December survey results are consistent with an economy that’s starting to slow, with some similarities to the data when NSW and Victoria were first entering lockdown,” said NAB Chief Economist Alan Oster. “That probably means conditions will fall in early 2022. However, we don’t expect the Omicron variant to derail the recovery longer-term.”

BoJ Kuroda keeps an eye on inflation risks while maintaining ultra-easy policy

BoJ Governor Haruhiko Kuroda told the parliament today, “the BOJ will continue its ultra-easy policy so improvements in corporate profits and the economy prop up wages and gradually accelerate consumer inflation.”

“We remain vigilant to the risk prices may shoot up before wages begin to rise, or how (rising raw material costs) could hurt smaller firms. We must keep an eye out on these risks, while maintaining our current easy monetary policy,” Kuroda said.

Meanwhile, Prime Minister Fumio Kishida said, “it’s desirable to create an environment in which companies can pass on rising costs and raise wages, so that increasing consumption spurs economic growth and inflation.”

Looking ahead

Germany Ifo business climate will be the main focus in European session. UK will release public sector net borrowing. Later in the day, US will release consumer confidence and house price index.

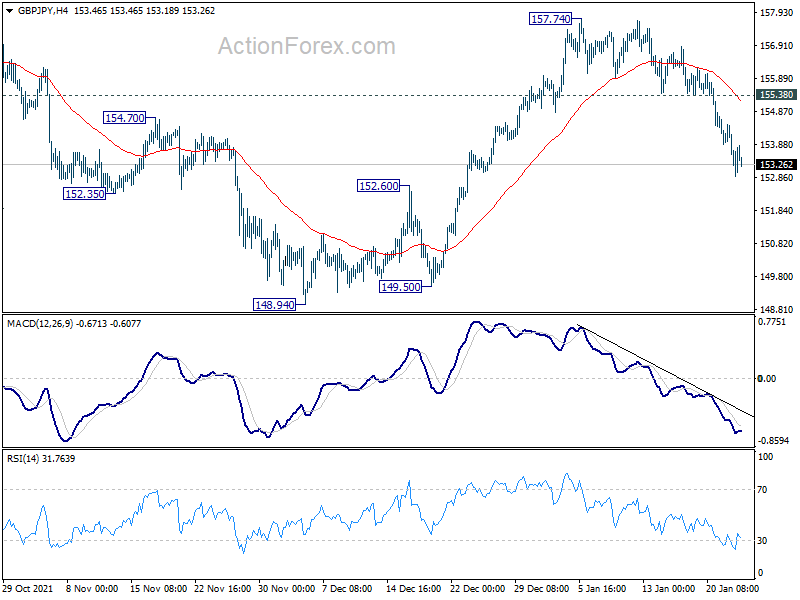

GBP/JPY Daily Outlook

Daily Pivots: (S1) 152.96; (P) 153.73; (R1) 154.54; More…

Intraday bias in GBP/JPY remains on the downside as fall from 157.74 is in progress. Such decline is seen as the third leg of the consolidative pattern from 158.19. Deeper fall would be seen to 148.94 support next. On the upside, above 155.38 minor resistance will flip bias back to the upside for 157.74/158.19 resistance zone instead.

{kind=link}

In the bigger picture, price actions from 158.19 are currently seen as developing into a consolidation pattern to up trend from 123.94 (2020 low). Downside should be contained by 123.94 to 158.19 at 145.10 to bring rebound. Firm break of 158.19 will resume the up trend to long term fibonacci level at 167.93. However, sustained break of 145.10 will raise the chance of trend reversal and target 61.8% retracement at 137.02.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Dec | -12 | 12 | ||

| 00:30 | AUD | NAB Business Conditions Dec | 8 | 12 | ||

| 00:30 | AUD | CPI Q/Q Q4 | 1.30% | 1.00% | 0.80% | |

| 00:30 | AUD | CPI Y/Y Q4 | 3.50% | 3.20% | 3.00% | |

| 00:30 | AUD | RBA Trimmed Mean CPI Q/Q Q4 | 1.00% | 0.70% | 0.70% | |

| 00:30 | AUD | RBA Trimmed Mean CPI Y/Y Q4 | 2.60% | 2.40% | 2.10% | |

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Dec | 14.5B | 16.6B | ||

| 09:00 | EUR | Germany IFO Business Climate Jan | 94.7 | 94.7 | ||

| 09:00 | EUR | Germany IFO Current Assessment Jan | 96.1 | 96.9 | ||

| 09:00 | EUR | Germany IFO Expectations Jan | 93 | 92.6 | ||

| 14:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Nov | 17.80% | 18.40% | ||

| 14:00 | USD | Housing Price Index M/M Nov | 1.00% | 1.10% | ||

| 15:00 | USD | Consumer Confidence Jan | 112.3 | 115.8 |