Aussie Dips Mildly on Cautious RBA, Dollar Paring Gains

Australian Dollar dips broadly after RBA sounds surprisingly cautious regarding raising interest rates. But loss is so far very limited, as supported by improving market sentiment following strong rebound in US stocks overnight. Dollar is the second weakest, continuing to pare recent gains while Yen is also heading lower. Euro is currently a stronger one for the week, as supported by buying in crosses, in particular against Sterling and Swiss Franc.

Technically, there is no clear sign of a larger reversal in Dollar yet, despite current retreat. Levels to watch include 1.1299 minor resistance in EUR/USD, 1.3523 minor resistance in GBP/USD, 0.7089 minor resistance in AUD/USD, 0.9243 minor support in USD/CHF and 114.46 minor support in USD/JPY. More upside in Dollar would remain in favor for the short term if these levels remain intact.

In Asia, at the time of writing, Nikkei is up 0.26%. Japan 10-year JGB yield is up 0.0015 at 0.177. Hong Kong, China and Singapore are on Lunar New Year holiday. Overnight, DOW rose 1.17%. S&P 500 rose 1.89%. NASDAQ rose 3.41%. 10-year yield closed flat at 1.782.

RBA stops QE purchases, to be patient on interest rate

RBA keeps cash rate target unchanged at 0.10% today. It’s reiterated that RBA “will not increase the cash rate until actual inflation is sustainably within the 2 to 3 per cent target range”. And, it is “too early to conclude that it is sustainably within the target band”. Thus, “the Board is prepared to be patient as it monitors how the various factors affecting inflation in Australia evolve.

RBA also decided to stop the asset purchase program after February 10. The issue of reinvestment of the proceeds of future bond maturities will be considered at the meeting in May.

As for the economy, RBA said Omicron “has not derailed” recovery. Central forecast if for GDP to grow around 4.25% over 2022 and 2% over 2.023. Unemployment rate is projected to fall below 4% later in the year, and to be around 3.75% at the end of 2023. Underlying inflation is is expected to increase further in coming quarters to around 3.25%, and decline to around 2.75% over 2023.

Australia retail sales dropped -4.4% mom in Dec, but turnover remains strong

Australia retail sales dropped -4.4% mom in December, much worse than expectation of -1.9% mom. That’s also the largest monthly decline since April 2020.

“Despite this month’s fall, retail turnover remains strong, up 4.8 per cent on December 2020, with strong consumer spending continuing post the Delta Outbreak,” Ben James, Director of Quarterly Economy Wide Statistics, said.

Australia AiG manufacturing dropped to 48.4, modest contraction

Australia AiG Performance of Manufacturing Index dropped sharply by -6.4 pts to 48.4 in January. Production dropped -0.6 to 51.9. Employment dropped -4.6 to 45.4. New orders dropped -8.0 to 51.3. Supplier deliveries dropped -15.6 to 37.8. Exports dropped -9.5 to 45.1. Input prices rose 4.0 to 82.3. Selling prices dropped -3.3 to 64.8. Wages rose 1.1 to 63.5.

Innes Willox, Chief Executive of Ai Group said: “Australia’s manufacturers reported a modest contraction in performance over December and January as businesses reported further disruptions to supply chains and as staff availability emerged as a major constraint on many businesses. Cost pressures were keenly felt with input prices continuing to rise and the selling prices index indicating only a partial recovery of these costs in the market.”

Fed Daly: We definitely are poised for a March increase

San Francisco Fed Bank President Mary Daly said “we definitely are poised for a March increase.” But she added, “after that, I want to see what the data brings us … let’s get through Omicron, let’s look at this and let’s see.”

“If the economy progresses like I see it progressing, then it is clear that it can stand on its own two feet, that we do not need to be providing the same level of extraordinary … accommodation that we provided during the pandemic and have provided for the last two years,” Daly said.

Fed Bostic: 50bps hike in March not my preferred action

Atlanta Fed Bank President Raphael Bostic said, 50bps hike in March was “not my preferred policy action.” He added, “I had three rate increases in mind. March is looking like the right time” to get that started. From there, however, “we are not on any set progression.”

“We are going to need to be thinking very carefully about how things are going, how the economy responds to our first moves,” Bostic said. “We are not set on any particular trajectory. The data will tell us what is happening.”

Fed Barkin: I don’t hear much resistance to rate hikes

Richmond Fed President Thomas Barkin said yesterday, “as I talk to participants in the economy, what I hear is they actually want us to do something now about inflation. They’d like us to get back to at least a normal interest-rate posture and not be simulating more demand on top of normal levels. So, I don’t hear much resistance to that.”

“I’d like us to be better positioned,” Barkin said. “Better positioned is somewhere closer to neutral, certainly, than we are now and I think the pace of that just depends on the pace of inflation.”

Fed George: Appropriate to move earlier on the balance sheet

Kansas City Fed President Esther George said Fed’s policy normalization approach could be more aggressive on balance sheet reduction, rather than faster rate hikes.

“What we do on the balance sheet is likely to affect the path of policy rates and vice versa,” George said during an event “For example, if we took more aggressive action on lowering, pulling down that balance sheet, it might allow for fewer interest rate increases.”

He added that raising short-term interest rate while maintaining a large balance sheet “could flatten the yield curve”, and lead to “reach-for-yield behavior from long-duration investors.”

“All in all, it could be appropriate to move earlier on the balance sheet relative to the last tightening cycle,” she said.

Elsewhere

Japan PMI manufacturing was finalized at 55.4 in January. Unemployment rate dropped from 2.8% to 2.7% in December.

New Zealand goods export rose 13% yoy to NZD 6.1B in December. Goods imports rose 23% yoy to USD 6.5B. Monthly trade balance was a deficit of NZD -477m, smaller than expectation of NZD -700m.

Looking ahead, Swiss will release retail sales and SECO consumer climate in European session. Eurozone will release PMI manufacturing infal and unemployment rate. Germany will release unemployment. UK will release PMI manufacturing final and M4 money supply.

Later in the day, Canada will release PMI manufacturing. US will release ISM manufacturing and construction spending.

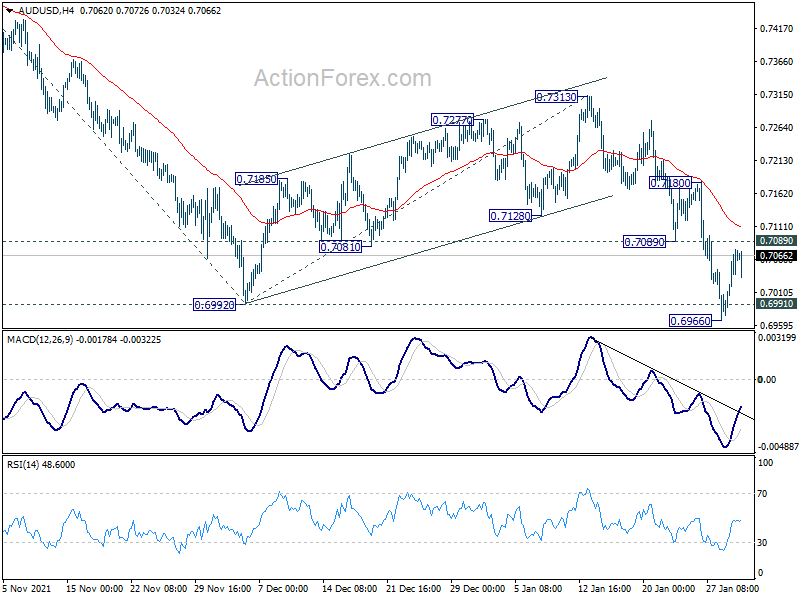

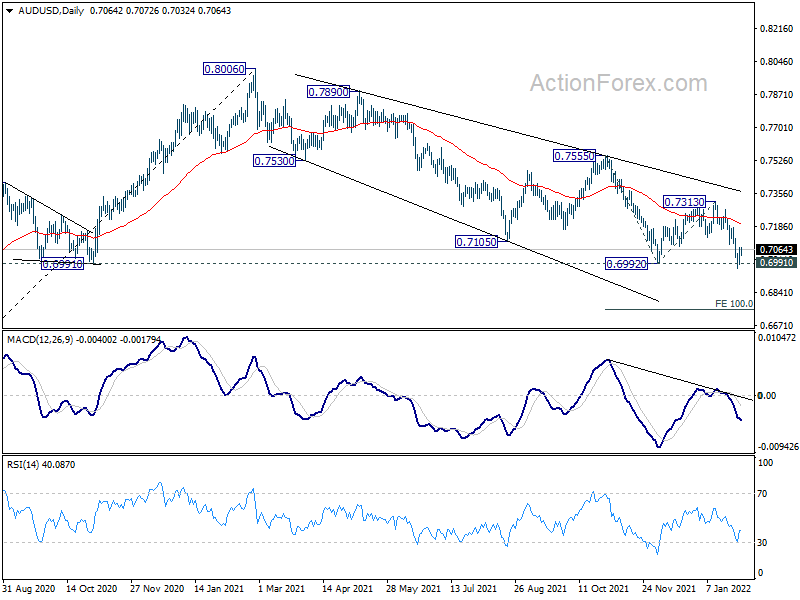

AUD/USD Daily Report

Daily Pivots: (S1) 0.7011; (P) 0.7044; (R1) 0.7101; More…

Intraday bias in AUD/USD remains neutral at this point. On the downside, sustained break of 0.6991 key support will confirm resumptions of whole down trend from 0.8006. Next target is 100% projection of 0.7555 to 0.6992 from 0.7313 at 0.6750. However, break of 0.7089 minor resistance will argue that 0.6991 was defended, and turn bias back to the upside for 0.7180 resistance next.

{kind=link}

In the bigger picture, focus remains on 0.6991 key structural support. Sustained break there will argue that the whole up trend from 0.5506 might be finished at 0.8006, after rejection by 0.8135 long term resistance. Deeper decline would then be seen back to 61.8% retracement of 0.5506 to 0.8006 at 0.6461. Meanwhile, strong rebound from 0.6991 will retain medium term bullishness. That is, whole up trend from 0.5506 is still in progress.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Mfg Index Jan | 48.4 | 54.8 | ||

| 21:45 | NZD | Trade Balance (NZD) Dec | -477M | -700M | -864M | -1060M |

| 23:30 | JPY | Unemployment Rate Dec | 2.70% | 2.80% | 2.80% | |

| 00:30 | AUD | Retail Sales M/M Dec | -4.40% | -1.90% | 7.30% | |

| 00:30 | JPY | Manufacturing PMI Jan F | 55.4 | 54.6 | 54.6 | |

| 03:30 | AUD | RBA Interest Rate Decision | 0.10% | 0.10% | 0.10% | |

| 07:00 | EUR | Germany Retail Sales M/M Dec | -1.20% | 0.60% | ||

| 07:30 | CHF | Real Retail Sales Y/Y Dec | 5.50% | 5.80% | ||

| 08:00 | CHF | SECO Consumer Climate Q1 | 4 | 4 | ||

| 08:50 | EUR | France Manufacturing PMI Jan F | 55.5 | 55.5 | ||

| 08:55 | EUR | Germany Unemployment Change Jan | -8K | -23K | ||

| 08:55 | EUR | Germany Unemployment Rate Jan | 5.20% | 5.20% | ||

| 08:55 | EUR | Germany Manufacturing PMI Jan F | 60.5 | 60.5 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Jan F | 59 | 59 | ||

| 09:30 | GBP | Mortgage Approvals Dec | 66K | 67K | ||

| 09:30 | GBP | Manufacturing PMI Jan F | 56.9 | 56.9 | ||

| 09:30 | GBP | M4 Money Supply M/M Dec | 0.80% | 0.70% | ||

| 10:00 | EUR | Eurozone Unemployment Rate Dec | 7.10% | 7.20% | ||

| 13:30 | CAD | GDP M/M Nov | 0.40% | 0.80% | ||

| 14:30 | CAD | Manufacturing PMI Jan | 56.5 | |||

| 14:45 | USD | Manufacturing PMI Jan F | 55 | 55 | ||

| 15:00 | USD | ISM Manufacturing PMI Jan | 57.5 | 58.7 | ||

| 15:00 | USD | ISM Manufacturing Prices Paid Jan | 79.5 | 68.2 | ||

| 15:00 | USD | ISM Manufacturing Employment Index Jan | 54.2 | |||

| 15:00 | USD | Construction Spending M/M Dec | 0.70% | 0.40% |