Euro Jumps on Record Inflation, Dollar Tumbles on Poor ADP Job Data

Dollar tumbles broadly today as markets are staying in risk-on mode. Additional selling pressure is seen on the greenback after shocking poor ADP job data. On the other hand, Euro is lifted by another record reading in consumer inflation data. Sterling is following Euro as markets await tomorrow’s BoE rate hike. Aussie is slowing down a bit, but maintains most of this week’s gains.

Technically, the case for near term bearish reversal in Dollar is building up with some levels taken out, including 1.1299 minor resistance in EUR/USD, 1.3523 minor resistance in GBP/USD and 114.46 minor support in USD/JPY. Focus is now on the next levels, including 1.1482 resistance in EUR/USD, 1.3748 resistance in GBP/USD, 0.7313 resistance in AUD/USD, 0.9090 support in USD/CHF and 113.46 support in USD/JPY. Break of these levels will suggest that Dollar has already started the bearish reversal.

In Europe, at the time of writing, FTSE is up 0.79%. DAX is up 0.39%. CAC is up 0.67%. Germany 10-year yield is up 0.0074 at 0.044. Earlier in Asia, Nikkei rose 1.68%. Japan 10-year JGB yield dropped -0.0038 to 0.179. Hong Kong, China and Shanghai were on holiday.

US ADP employment dropped -301k in Jan due to Omicron

US ADP private employment dropped -301k in January, much worse than expectation of 270k growth. By company size, small businesses lost -144k jobs, medium business lost -59k, large business lost -98k. By sector, goods-producing jobs dropped -27k, services-providing jobs dropped -274k.

“The labor market recovery took a step back at the start of 2022 due to the effect of the Omicron variant and its significant, though likely temporary, impact to job growth,” said Nela Richardson, chief economist, ADP. “The majority of industry sectors experienced job loss, marking the most recent decline since December 2020. Leisure and hospitality saw the largest setback after substantial gains in fourth quarter 2021, while small businesses were hit hardest by losses, erasing most of the job gains made in December 2021.”

Eurozone CPI accelerated to new record 5.1% yoy in Jan

Eurozone CPI accelerated to 5.1% yoy in January, up from December 5.0% yoy, well above expectation of slowing to 4.3% yoy. That’s also another record high. CPI core dropped from 2.6% yoy to 2.3% yoy, but still beat expectation of 1.9% yoy.

Energy is expected to have the highest annual rate (28.6%, compared with 25.9% in December), followed by food, alcohol & tobacco (3.6%, compared with 3.2% in December), services (2.4%, stable compared with December) and non-energy industrial goods (2.3%, compared with 2.9% in December).

RBA Lowe: Ending bond purchase does not mean imminent rate hike

In a speech, RBA Governor Philip Lowe said ending the bond purchase program “does not mean that an increase in the cash rate is imminent”.

He noted that while inflation has picked up in Australia, it remains “substantially lower” than the 7% in the US, 5.4% in the UK and 5.9% in New Zealand. It has “not been accompanied by strong wages growth” as in the case in the US and UK. “Our lower rate of inflation and low wages growth are key reasons we don’t need to move in lock step with others,” he added.

Lowe also said it’s “too early to conclude” that inflation is sustainably the in the target range. And there is “a range of significant uncertainties” here that will “take time to resolve”. He reiterated that “the Board is prepared to be patient as it monitors the evolution of the various factors affecting inflation in Australia.”

New Zealand employment dropped to record low 3.2%

New Zealand employment rose 0.1% in Q4, below expectation of 0.4%. Unemployment rate ticked down from 3.3% to 3.2%, slightly better than expectation of 3.2%. Labor force participation rate dropped -0.1% to 71.1%.

“The labour market continued to show the tightness we saw in the September 2021 quarter, with both unemployment and underutilisation rates remaining low,” work and wellbeing statistics senior manager Becky Collett said. “This quarter’s unemployment rate is now the lowest rate recorded since the HLFS series began in 1986.”

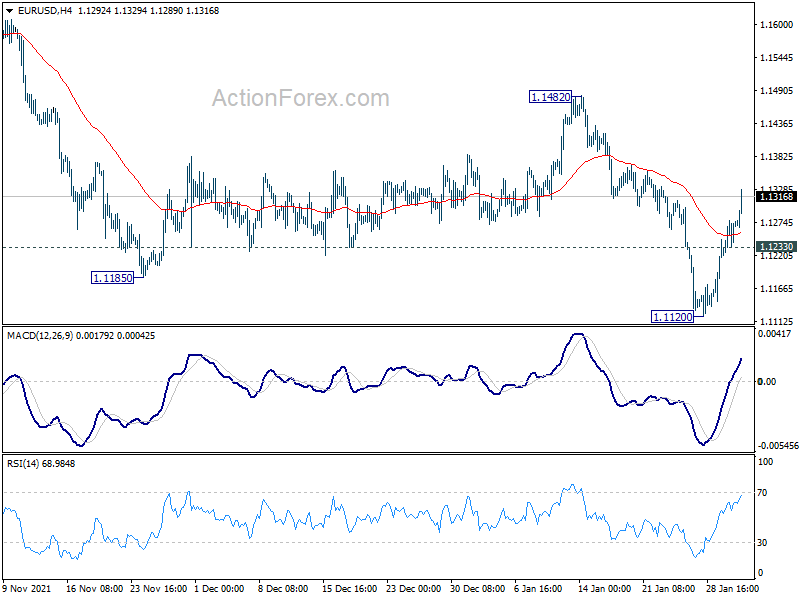

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1236; (P) 1.1258; (R1) 1.1294; More…

EUR/USD’s break of 1.1299 minor resistance suggests that fall form 1.1482 has completed. Intraday bias is back on the upside for 1.1482 resistance first. Firm break there will argue that a medium term bottom was formed on bullish convergence condition in daily MACD. Stronger rally would then be seen back to 1.1703 support turned resistance next. On the downside, break of 1.1233 minor support will flip bias back to the downside for retesting 1.1120 low instead.

{kind=link}

In the bigger picture, the strength of the the decline from 1.2348 (2021 high) suggests that it’s not a corrective move. But still, it could be the fourth leg of a sideway pattern from 1.0339 (2017 low), or resuming long term down trend. In any case, outlook will now stay bearish as long as 1.1482 resistance holds. Next target would be 1.0635 low. However, firm break of 1.1482 will raise the chance that whole fall from 1.2348 has completed, and turn focus back to 1.1703 resistance for confirmation.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Employment Change Q4 | 0.10% | 0.40% | 2.00% | 1.90% |

| 21:45 | NZD | Unemployment Rate Q4 | 3.20% | 3.30% | 3.40% | 3.30% |

| 23:50 | JPY | Monetary Base Y/Y Jan | 8.40% | 8.50% | 8.30% | |

| 10:00 | EUR | Eurozone CPI Y/Y Jan P | 5.10% | 4.30% | 5.00% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Jan P | 2.30% | 1.90% | 2.60% | |

| 13:15 | USD | ADP Employment Change Jan | -301K | 270K | 807K | 776K |

| 13:30 | CAD | Building Permits M/M Dec | -1.90% | -1.60% | 6.80% | |

| 15:30 | USD | Crude Oil Inventories | 1.8M | 2.4M |