Dollar Little Changed After Solid NFP, Euro Shrugs CPI

Dollar is little changed after another set of solid job data. The greenback is trying to extend the near term recovery against Euro and Yen, but turns softer against Aussie. Euro also shrugs off much stronger than expected consumer inflation reading. Yen continues to consolidate in tight range, digesting recent losses. There is still prospect of some bigger moves, depending how the risk markets end the week.

In Europe, at the time of writing, FTSE is up 0.36%. DAX is up 0.35%. CAC is up 0.47%. Germany 10-year yield is up 0.031 at 0.580. Earlier in Asia, Nikkei dropped -0.56%. Hong Kong HSI rose 0.19%. China Shanghai SSE rose 0.94%. Singapore Strait Times rose 0.31%. Japan 10-year JGB yield rose 0.0006 to 0.216.

US NFP employment grew 431k, unemployment rate dropped to 3.6%

US non-farm payroll employment grew 431k in March, lower than expectation of 488k. Overall job growth averaged 562k per month in Q1, the same as the average monthly gain for 2021. Employment was still down by -1.6m, or -1.0%, from its prepandemic level in February 2020.

Unemployment rate dropped from 3.8% to 3.6%, better than expectation of 3.7%. Labor force participation rate rate little changed at 62.4%.

Average hourly earnings rose 0.4% mom, matched expectations.

Eurozone CPI rose to 7.5% yoy, core CPI up to 3.1% yoy

Eurozone CPI accelerated sharply from 5.9% yoy to record high at 7.5% yoy in March, above expectation of 6.5% yoy. Core CPI also rose from 2.7% yoy to 3.0% yoy, but missed expectation of 3.1% yoy.

Looking at the main components of Eurozone inflation, energy is expected to have the highest annual rate (44.7%, compared with 32.0% in February), followed by food, alcohol & tobacco (5.0%, compared with 4.2% in February), non-energy industrial goods (3.4%, compared with 3.1% in February) and services (2.7%, compared with 2.5% in February).

Eurozone PMI manufacturing finalized at 56.5, Ukraine war an ominous new headwind

Eurozone PMI Manufacturing was finalized at 56.5 in March, down from February’s 58.2, hitting a 14-month low. Looking at some member states, Germany PMI manufacturing dropped to 18-month low at 56.9. Italy dropped to 14-month low at 55.8. France dropped to 5-month low at 54.7.

Chris Williamson, Chief Business Economist at S&P Global said: “Just as the fading of the latest pandemic wave was creating a tailwind for the eurozone manufacturing recovery, with economies re-opening and supply chain bottlenecks easing, the war In Ukraine has created an ominous new headwind.”

UK PMI manufacturing finalized at 55.2, hit by several headwinds simultaneously

UK PMI manufacturing was finalized at 13-month low of 55.2, down from February’s 58.0. S&P Global said new export orders contracted for the second month running. Inflationary pressures strengthened.

Rob Dobson, Director at S&P Global, said: “Manufacturers are being hit by several headwinds simultaneously, as supply shortages, greater caution among clients, escalating inflationary pressures, ongoing Brexit factors and rising geopolitical tensions all hamper the upturn. It is therefore little surprise that business optimism has slumped to a 14-month low.”

China Caixin PMI manufacturing dropped to 48.1, fastest contraction in two years

China Caixin PMI Manufacturing dropped from 50.4 to 48.1 in March, below expectation of 49.7. The pace of contraction was quickest since February 2020. Caixin said production fell at quickest rate for just over two years amid tighter pandemic restrictions. Total new work and foreign demand had steep declines. Suppliers’ delivery times worsened while cost pressures intensified.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Overall, impacted by factors including the Covid-19 outbreaks in multiple parts of China, manufacturing activity largely weakened in March. Supply contracted. Demand was also under pressure, and external demand worsened. The job market was more or less stable. Inflationary pressure continued to rise. And market optimism weakened.”

Japan PMI manufacturing finalized at 54.1, improvement in operation but subdued international markets

Japan PMI Manufacturing was finalized at 54.1 in March, up from February’s 52.7. Markit said there was renewed rise in output and stronger new order growth. But export orders had sharpest fall for 20 months. Stocks of raw materials had record rise amid higher prices and delays.

Usamah Bhatti, Economist at S&P Global, said:

“The Japanese manufacturing sector saw an improvement in operating conditions at the end of the first quarter of 2022… new order inflows saw a quickening in growth… international markets were subdued, following the reintroduction of strict restrictions across parts of China and the outbreak of war between Russia and Ukraine. As a result, new export orders fell at the sharpest rate since July 2020….

“Beyond the immediate future, firms remained confident about the year-ahead outlook for output, though the downside risks led to the softest degree of optimism for seven months. This is in line with current estimates for industrial production to rise 3.7% in 2022, meaning that output lost to the pandemic is unlikely to be recovered until 2023.”

Australia AiG manufacturing rose to 55.7, price pressures stepped up

Australia AiG Performance of Manufacturing Index rose from 53.2 to 55.7 in March. Looking at some details, production dropped -1.2 to 53.4. Employment rose 9l9 to 53.4. New orders rose 5.2 to 65.0. Input prices rose 6.8 to 82.4. Selling prices rose 0.4 to 72.0. Average wages rose 1.7 to 66.6.

Innes Willox, Chief Executive of Ai Group said: “The Australian manufacturing sector grew faster in March as manufacturers added new staff, lifted sales and continued to expand production (although at a slower pace than in February)… Across manufacturing pressures from wages and input prices stepped up while selling prices growth saw manufacturers recover some cost increases in the market. There was an encouraging rise in new orders in March although with labour and input supply constraints growing, manufacturers will be stretched to fill orders in a timely way.”

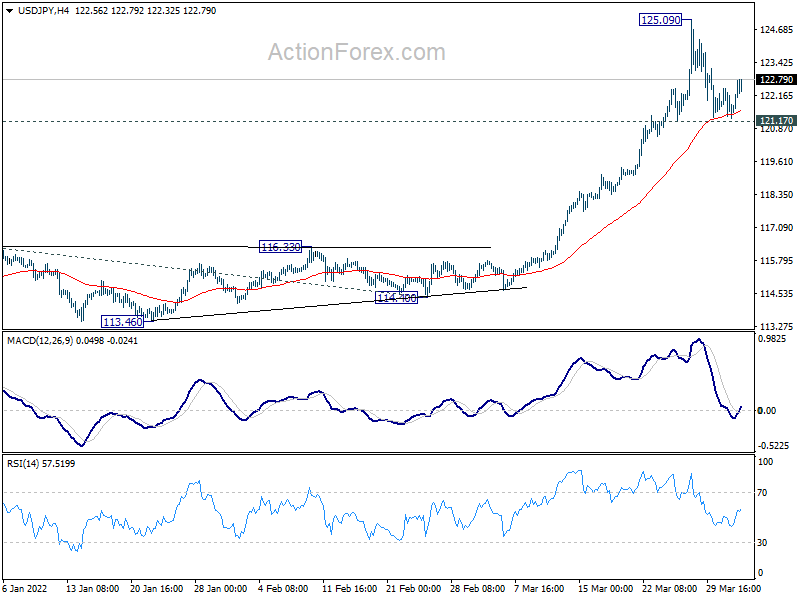

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 121.03; (P) 122.12; (R1) 122.92; More…

Intraday bias in USD/JPY remains neutral for the moment. With 121.17 support intact, further rally is in favor. On the upside, above 125.09 will target 161.8% projection of 109.11 to 116.34 from 114.40 at 126.09, which is close to 125.85 long term resistance. However, break of 121.17 will indicate short term topping, and bring deeper pull back.

{kind=link}

In the bigger picture, up trend from 98.97 (2016 low) in in progress for retesting 125.85 (2015 high). Sustained break there will confirm long term up trend resumption. Next target will be 61.8% projection of 75.56 (2011 low) to 125.85 (2015 high) from 98.97 at 130.04. This will now remain the favored case as long as 116.34 resistance turned support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Mfg Index Mar | 55.7 | 53.2 | ||

| 23:50 | JPY | Tankan Large Manufacturing Index Q1 | 14 | 12 | 18 | |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q1 | 9 | 10 | 13 | |

| 23:50 | JPY | Tankan Non – Manufacturing Index Q1 | 9 | 5 | 9 | |

| 23:50 | JPY | Tankan Non – Manufacturing Outlook Q1 | -10 | 8 | 8 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q1 | 2.20% | 4.40% | 9.30% | |

| 00:30 | JPY | Manufacturing PMI Mar F | 54.1 | 53.2 | 53.2 | |

| 01:45 | CNY | Caixin Manufacturing PMI Mar | 48.1 | 49.7 | 50.4 | |

| 06:30 | CHF | CPI M/M Mar | 0.60% | 0.50% | 0.70% | |

| 06:30 | CHF | CPI Y/Y Mar | 2.40% | 2.40% | 2.20% | |

| 07:30 | CHF | SVME PMI Mar | 64 | 61 | 62.6 | |

| 07:45 | EUR | Italy Manufacturing PMI Mar | 55.8 | 57 | 58.3 | |

| 07:50 | EUR | France Manufacturing PMI Mar F | 54.7 | 54.8 | 54.8 | |

| 07:55 | EUR | Germany Manufacturing PMI Mar F | 56.9 | 57.6 | 57.6 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Mar F | 56.5 | 57 | 57 | |

| 08:30 | GBP | Manufacturing PMI Mar F | 55.2 | 55.5 | 55.5 | |

| 09:00 | EUR | Eurozone CPI Y/Y Mar P | 7.50% | 6.50% | 5.90% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Mar P | 3.00% | 3.10% | 2.70% | |

| 12:30 | USD | Nonfarm Payrolls Mar | 431K | 488K | 678K | 750K |

| 12:30 | USD | Unemployment Rate Mar | 3.60% | 3.70% | 3.80% | |

| 12:30 | USD | Average Hourly Earnings M/M Mar | 0.40% | 0.40% | 0.00% | 0.10% |

| 13:30 | CAD | Manufacturing PMI Mar | 56.5 | 56.6 | ||

| 13:45 | USD | Manufacturing PMI Mar F | 58.5 | |||

| 14:00 | USD | ISM Manufacturing PMI Mar | 58.4 | 58.6 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Mar | 76 | 75.6 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Mar | 53.7 | 52.9 | ||

| 14:00 | USD | ISM Manufacturing New Orders Index Mar | 59.8 | 61.7 | ||

| 14:00 | USD | Construction Spending M/M Feb | 0.90% | 1.30% |