Yield Curve Inversion, Stocks Rallied, Euro Rebounded

There were a couple of developments of last week to note. Firstly, US yield curve inverted for the first time since 2019. There is no reason to panic for the moment, but deeper inversion could set the tone in the risk markets ahead. Secondly, Euro ended as the strongest one, attempting to extend its near term rebound. But momentum of the common currency has been rather disappointing. Euro still have a lot to prove. Thirdly, Yen’s recovery faltered somewhat and ended as one of the worst performers. There is prospect of a return to weakness in Yen. But deeper pull back in benchmark treasury yields has the prospect to give Yen a hand. Elsewhere in the forex markets, Swiss Franc and Dollar were the second and third best performer. Sterling and Kiwi are among the worst.

While the impact of Russia invasion of Ukraine seemed to be fading, the overall direction of of major forex pairs and crosses will continue to hinge on the developments on it. Risks are two sided as acknowledged by central bankers from the BoE and ECB, higher inflation and lower growth. Chance of stagflation is so far talked down, but it will depend on how long the invasion would last.

{kind=link}

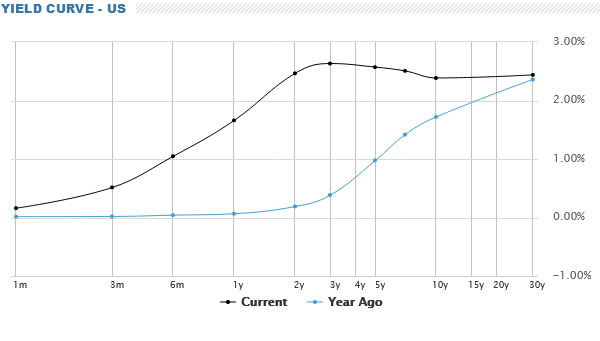

First yield curve inversion in US since 2019

Yield curve inversion became a much talked about topic last week. The mostly watched part of the curve, between yield of 2-year and 10-year notes, inverted for the first time since 2019. The spread between 2-year yield at 2.465 and 10-year yield at 2.377 wasn’t too serious, and it’s still inconclusive to call for a recession in the US. But risk of deeper inversion is growing.

{kind=link}

Fed is clearly on track to normalize interest rate to neutral at around 2.4-2.5%, and possibly slightly above. There is still room for yields to rise in the short end. However, 10-year yield is now facing a key multi-decade channel resistance at around 2.6. A light-handed rejection from there could easily push TNX through 2.299 support back to 2.00 handle, which is close to 55 day EMA (now at 2.025) and 2.065 resistance turned support. A spread of -0.4 to -0.5 between 2-year and 10-year yield would be rather serious.

{kind=link}

{kind=link}

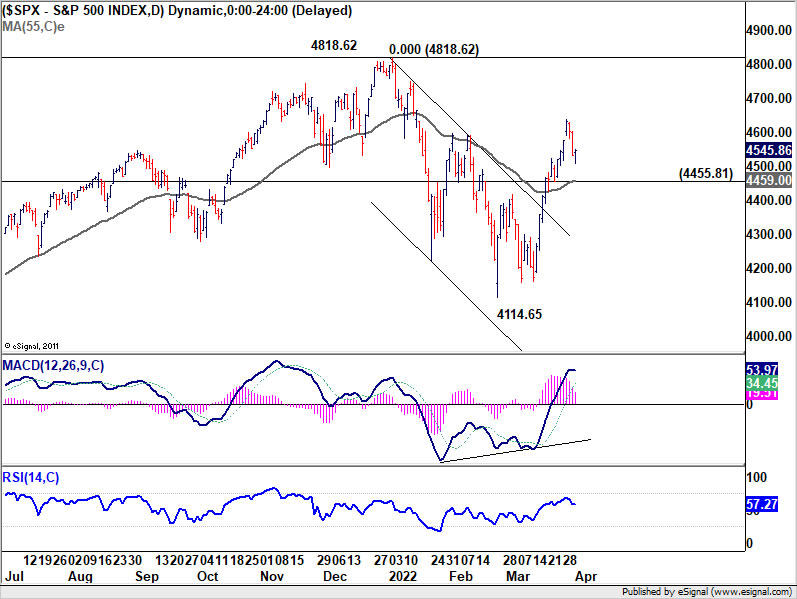

S&P 500 on track to retest 4818 high

Meanwhile, it should be noted that even if a recession is going to occur in the US, it could be around 12- to 18-months away. Stocks typically lead the economy by 6 to 12 months. Due to the different time frame, there is no reason for investors to panic on yield curve inversion for now. Indeed, S&P 500 extended the rebound from 4114.65 last week. Further rise is expected as long as 4455.81 support holds, to retest 4818.62 high.

For now, strong resistance is expected around 4818.62 to bring near term reversal, to start the third leg of the corrective pattern from there. The steepness and depth of this third leg could be indicative on the next recession. But of course, it would then be a completely different picture if SPX could break through 4818.62 in decisive manner.

{kind=link}

Euro rebound made progress, but momentum unconvincing

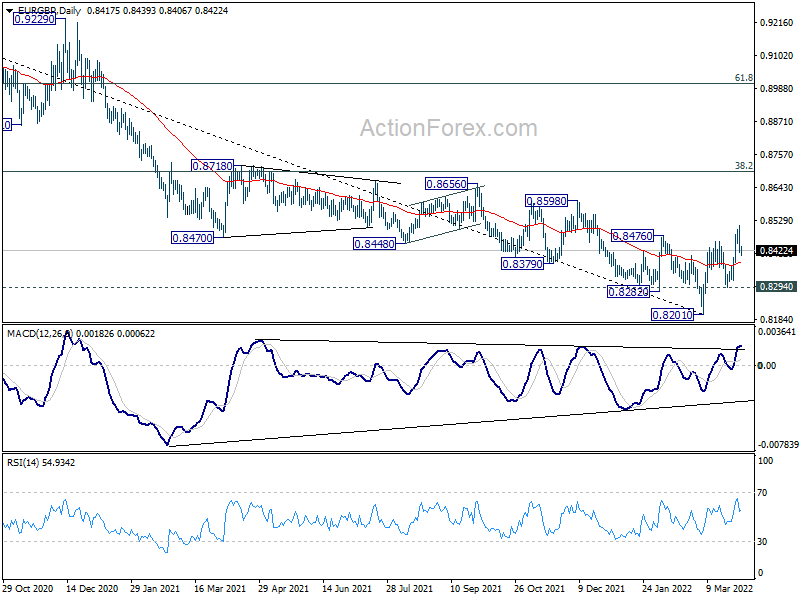

In the forex markets, there are two developments to monitor in the days ahead. Firstly, both EUR/USD and EUR/GBP made some progress in breaching 1.1120 and 0.8476 resistance last week. Both are signs of bullish reversal, but upside momentum has been unconvincing.

As for EUR/USD, further rise will remain mildly in favor as long as 1.0943 support holds. Rebound from 1.0805 should resume later to target 38.2% retracement of 1.2265 to 1.0805 at 1.1363.

{kind=link}

Further rise is also in favor in EUR/GBP as long as 0.8294 support holds. Rebound from 0.8201 would target 0.8598 resistance and above.

{kind=link}

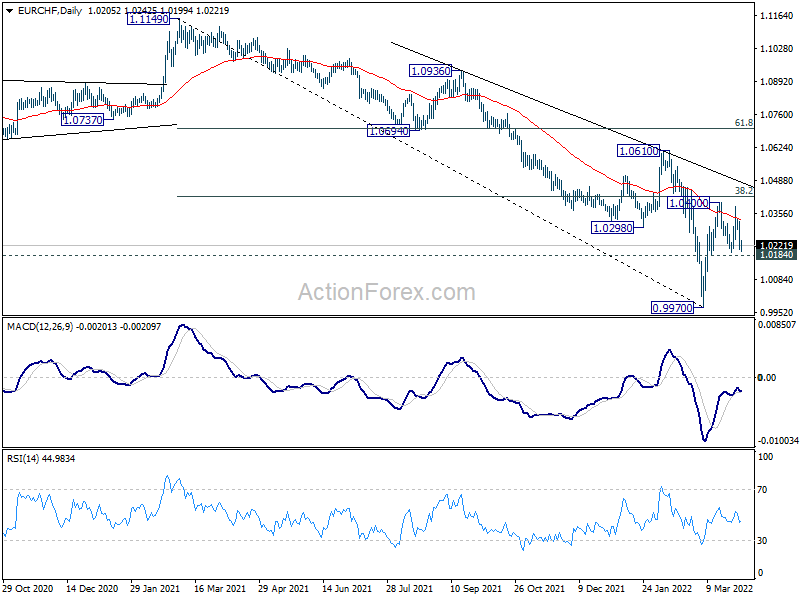

However, EUR/CHF’s rally attempt faltered below 1.0400 near term resistance. Break below 1.0184 minor support will revive near term bearishness for at least a retest on 0.9970 low. If this happens, EUR/USD and EUR/GBP could be dragged below the above mentioned support levels. That would in turn signal that Euro’s overall rebound has completed earlier than expected.

{kind=link}

Yen crosses continue to consolidate, above near term support levels

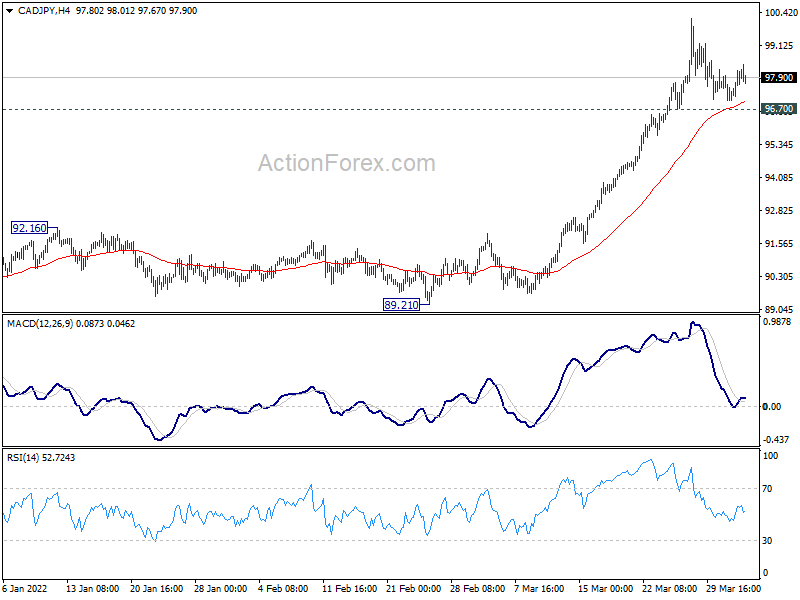

Secondly, the retreats in Yen crosses were so far rather shallow. For example, CAD/JPY is holding comfortably above 96.70 minor support.

{kind=link}

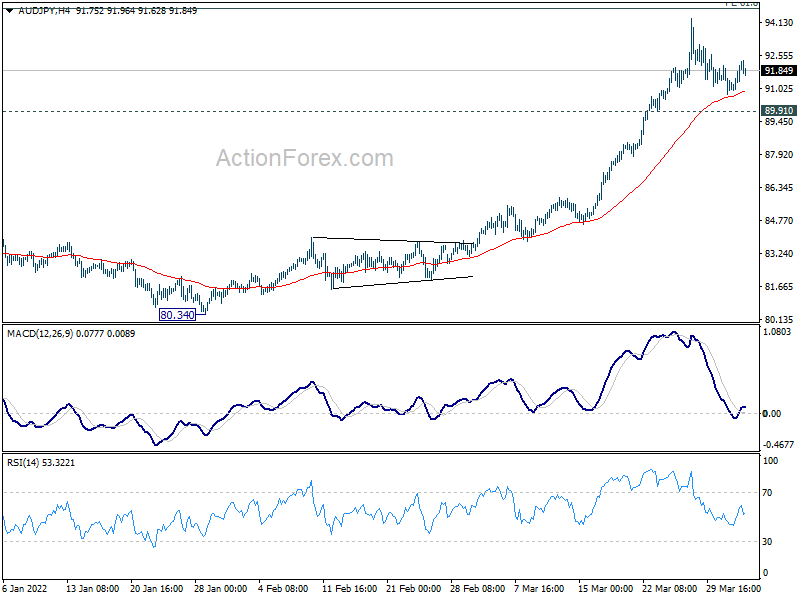

AUD/JPY is holding above 89.91 minor support too. Rallies in both crosses are expected to resume sooner rather than later.

{kind=link}

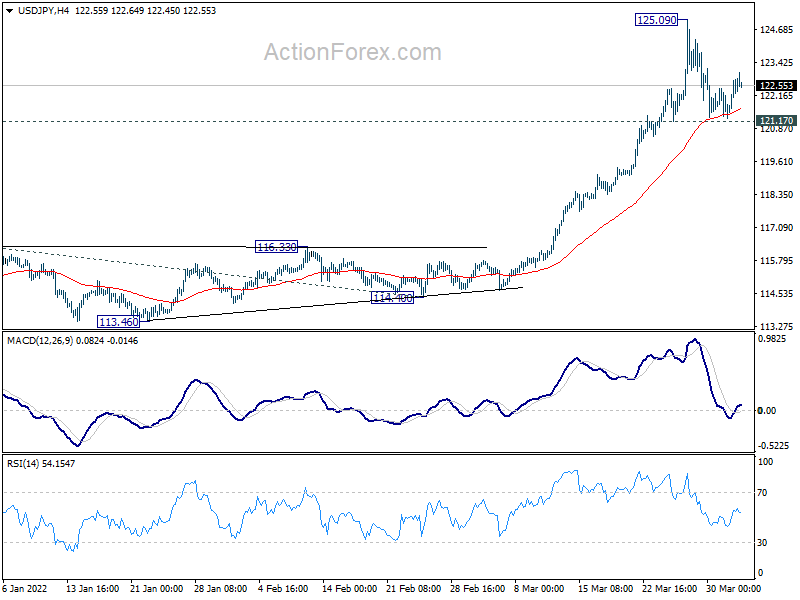

At the same time, USD/JPY is also holding above 121.17 minor support, which should theoretically set the base for up trend resumption. However, extended decline in US benchmark yield could drag USD/JPY through this 121.17 support for deeper correction. In this case, other Yen crosses could be dragged down too, which would sign a more sustainable near term rebound in Yen that could last for a while.

{kind=link}

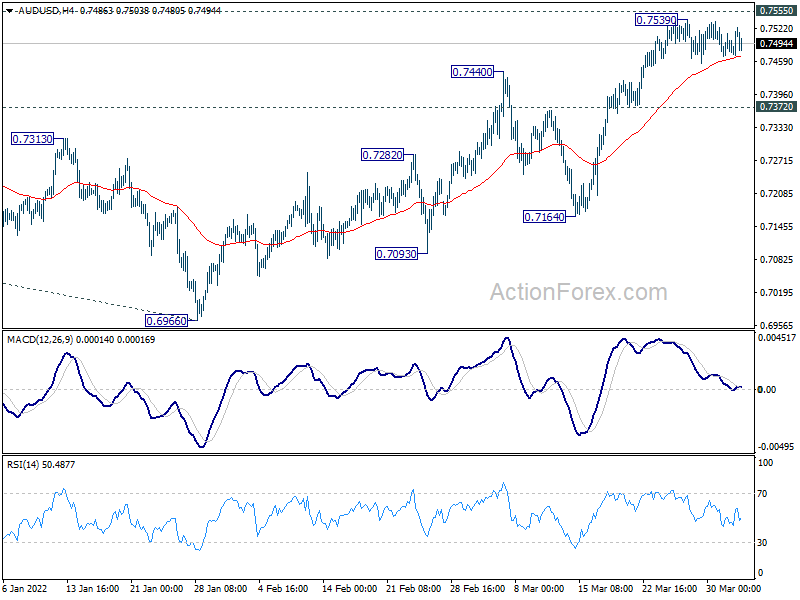

AUD/USD Weekly Outlook

AUD/USD formed a temporary top at 0.7539 last week, ahead of 0.7555 resistance, and turned sideway. Initial bias remains neutral this week and more consolidations could be seen. But further rally is expected as long as 0.7372 minor support holds. On the upside, decisive break of 0.7555 should confirm that whole corrective decline from 0.8006 has completed at 0.6966. Further rise should then be seen back to retest 0.8005. However, break of 0.7372 will dampen this bullish view and turn bias back to the downside for 0.7164 support instead.

{kind=link}

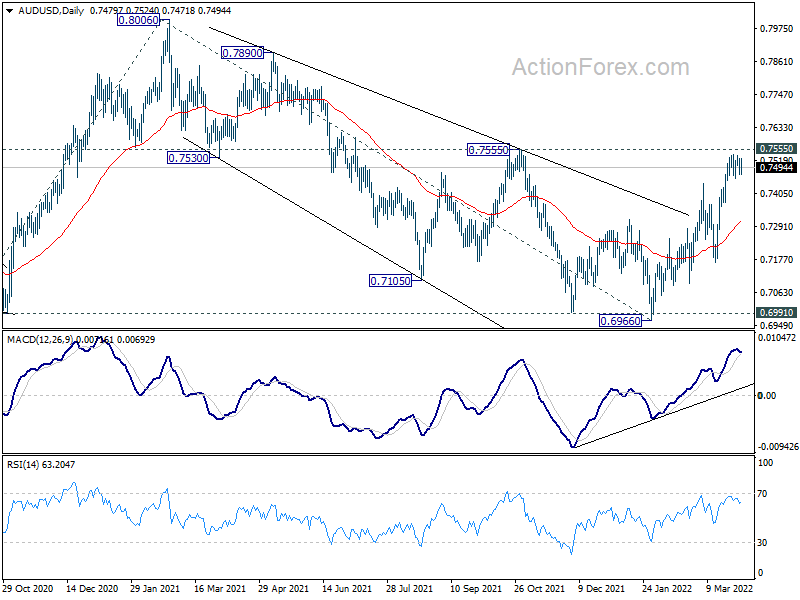

In the bigger picture, correction from 0.8006 could have completed at 0.6966, after drawing support from 0.6991. That is, up trend from 0.5506 (2020 low) might be ready to resume. Firm break of 0.8006 will target 61.8% projection of 0.5506 to 0.8006 from 0.6966 at 0.8511 next. This will remain the favored case as long as 0.7164 support holds.

{kind=link}

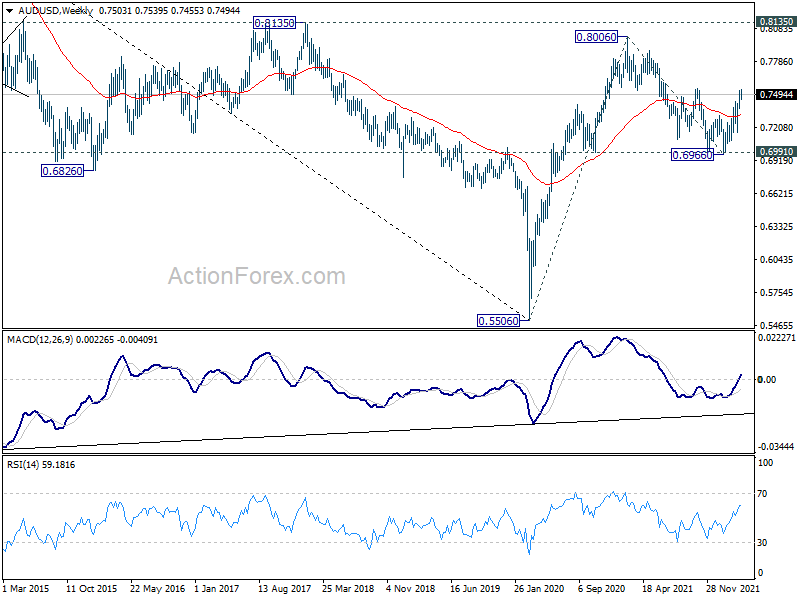

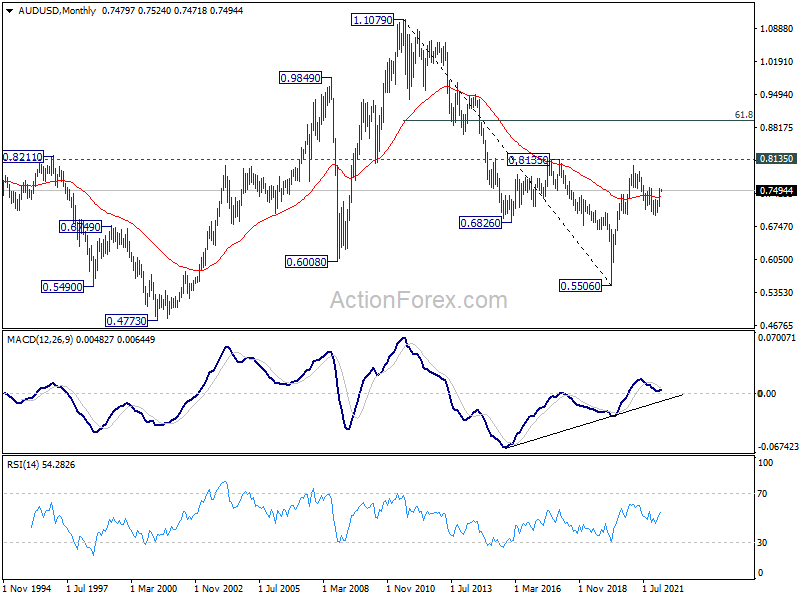

In the longer term picture, focus remains on 0.8135 structural resistance. Decisive break there will argue that rise from 0.5506 is developing into a long term up trend that reverses whole down trend from 1.1079 (2011 high). However, rejection by 0.8135 will keep long term outlook neutral at best.

{kind=link}

{kind=link}