Dollar Slows Against Europeans, Firm Against Commodity Currencies

Dollar remains generally firm entering into US session, even though upside momentum is diminishing slightly against European majors.

Meanwhile weakness in commodity currencies persists, with Aussie being the worst one. Yen is mixed for now but should remain vulnerable on exceptional strength in global benchmark treasury yields.

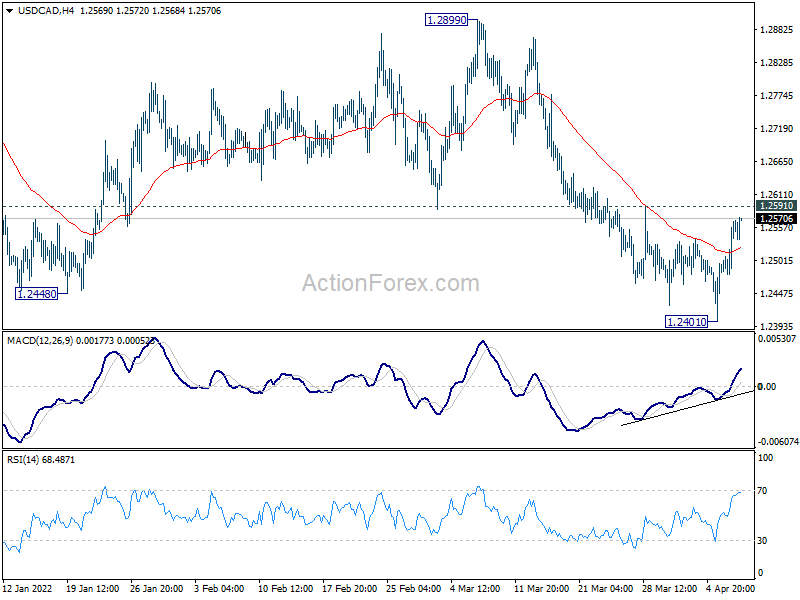

Technically, focuses firstly stays on commodity-dollar pairs. In particular, break of 0.7455 minor support in AUD/USD and 1.2591 minor resistance would indicate more upside in the greenback, possibly on some deterioration in market sentiments too. At the same time, USD/JPY could also be ready to extend rebound from 121.27 to retest 125.09 high. Break of this high would indicate return to selling in Yen.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.08%. DAX is up 0.61%. CAC is up 0.65%. Germany 10-year yield is up 0.0489 at 0.698. Earlier in Asia, Nikkei dropped -1.69%. Hong Kong HSI dropped -1.23%. China Shanghai SSE dropped -1.42%. Singapore Strait Times dropped -0.55%. Japan 10-year JGB yield dropped -0.0070 to 0.245.

US initial jobless claims dropped to 166k

US initial jobless claims dropped -5k to 166k in the week ending April 2. Four-week moving average dropped -8k to 170k. Continuing claims rose 17k to 1523k in the week ending March 26. Four-week moving average of continuing claims dropped -25k to 1541k.

It should be noted that the methodology used to seasonally adjust the numbers were revised with this release.

ECB accounts: War risks slowflation only, not stagflation

The accounts of ECB’s March 9-10 meeting noted that “while the Russian invasion of Ukraine had increased uncertainty surrounding the macroeconomic outlook, related risks to the inflation outlook were seen as largely one-sided, with experience suggesting that wars tended to be inflationary”.

“While the war would likely dent economic growth in the short term, annual growth was projected to remain positive even in the severe scenario, pointing to ‘slowflation’ rather than stagflation.”

“The greater persistence of inflation increased the probability of second-round effects via strengthening wage dynamics…. a longer period of above-target inflation would lead to an increased risk of an upward unanchoring of longer-term inflation expectations.”

Thus, the Governing Council could “no longer afford to look through higher inflation, even if it was driven by an adverse supply shock.”

ECB decided at the meeting to revise the plan for APP net purchases, with the option to end after June. “Easing bias” was removed from the forward guidance. Interest rate hike would come “shorter” after ending the net purchases, depending on incoming data.

Eurozone retail sales rose 0.3% mom in Feb, EU up 0.3% mom

Eurozone retail sales rose 0.3% mom in February, below expectation of 0.6% mom. Volume of retail trade increased by 3.2% for automotive fuels, and by 0.8% for non-food products, while it fell by 0.5% for food, drinks and tobacco.

EU retail sales also rose 0.3% mom. Among Member States for which data are available, the highest monthly increases in the total retail trade volume were registered in Slovenia (+8.0%), the Netherlands (+4.0%) and Portugal (+2.3%). The largest decreases were observed in Belgium (-1.8%), Estonia (-1.7%), and Poland (-1.6%).

Also released, Germany industrial production rose 0.2% mom in February, above expectation of 0.0% mom. Swiss unemployment rated dropped from 2.3% to 2.2% in March. Swiss foreign currency reserves dropped from CHF 938B to CHF 911B in March.

BoJ Noguchi: Takes significant time to justify stimulus withdrawal

Bank of Japan board member Asahi Noguchi said while core consumer inflation may exceed 2% from April, it’s mainly driven by external factors rather than domestic demand. He added, “Japan is not experiencing the kind of high inflation seen in many other countries.”

“In a country still mired in a sticky deflationary mindset, it will take significant time to stably achieve our 2% inflation target and justify a withdrawal of stimulus,” he added.

Australia AiG services dropped to 56.2, intensifying price and wage pressures

Australia AiG Performance of Services Index dropped -3.8 pts to 56.2 in March. Sales dropped sharply by -14.9 to 53.7. Employment dropped -0.3 to 54.4. But new orders rose 2.4 to 63.5. Input prices jumped 11.5 to 77.5. Selling prices also rose 4.2 to 64.5. Average wages surged 11.8 to 67.7.

Innes Willox, Chief Executive of the national employer association Ai Group, said: “Australia’s services sector continued its positive run in March although the pace of growth slowed in the face of intensifying input price pressures, difficulties in finding staff and further wage pressures.”

Also from Australia, goods and services export was relatively unchanged over the month at AUD28.8B in February. Goods and services imports rose 12% mom to AUD 41B. Trade surplus shrank to AUD 7.46B, smaller than expectation of AUD 11.70B.

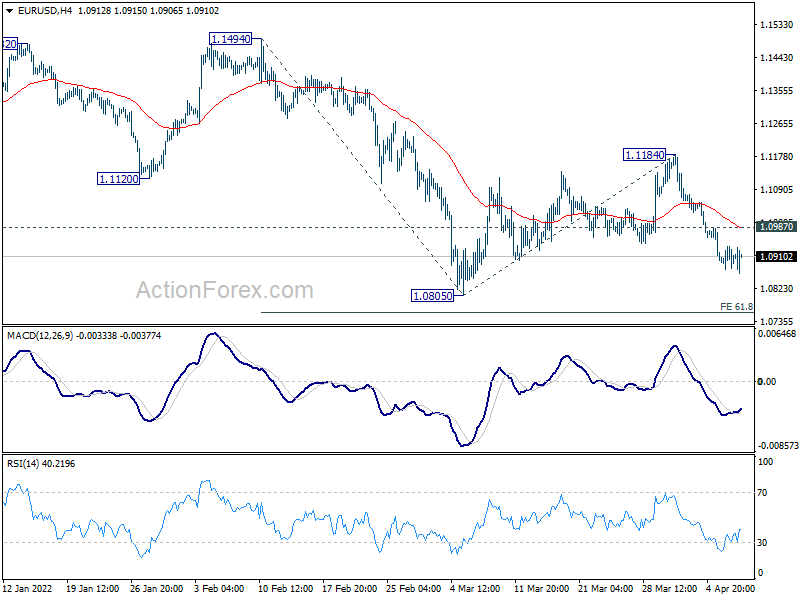

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0869; (P) 1.0903 (R1) 1.0932; More…

EUR/USD is losing some downside momentum as seen in 4 hour MACD, but further decline is expected with 1.0987 minor resistance intact. Deeper decline would be seen to 1.0805 low. Firm break there will resume larger down trend from 1.2248. Next target is 61.8% projection of 1.1494 to 1.0805 from 1.1184 at 1.0758, and then 100% projection at 1.0495. On the upside, above 1.0987 minor resistance will mix up the outlook and bring recovery.

{kind=link}

In the bigger picture, the decline from 1.2348 (2021 high) is expected to continue as long as 1.1494 resistance holds. Firm break of 1.0635 (2020 low) will raise the chance of long term down trend resumption and target a retest on 1.0339 (2017 low) next. Nevertheless, break of 1.1494 will maintain medium term neutral outlook, and extending term range trading first.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Services Index Mar | 56.2 | 60 | ||

| 01:30 | AUD | Trade Balance (AUD) Feb | 7.46B | 11.70B | 12.89B | 11.79B |

| 05:00 | JPY | Leading Economic Index Feb P | 110.9 | 103 | 102.5 | |

| 05:45 | CHF | Unemployment Rate Mar | 2.20% | 2.20% | 2.20% | 2.30% |

| 06:00 | EUR | Germany Industrial Production M/M Feb | 0.20% | 0.00% | 2.70% | |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Mar | 911B | 938B | ||

| 09:00 | EUR | Eurozone Retail Sales M/M Feb | 0.30% | 0.60% | 0.20% | |

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:30 | USD | Initial Jobless Claims (Apr 1) | 166K | 200K | 202K | 171K |

| 14:30 | USD | Natural Gas Storage | 18.0B | 26B |