Dollar Turned Mixed as CPI Awaited, Yen Weakness Continues

Dollar turned a bit mixed in Asian session as markets await consumer inflation data from the US today. The greenback is losing some momentum against Yen as it’s pressing a long term resistance level at 125.85. Meanwhile, it ticks down against European majors, which are recovering. On the other hand, Dollar is extending rebound against Canadian, which is now the second weakest, even though a big 50bps rate hike is expected from BoC later in the week.

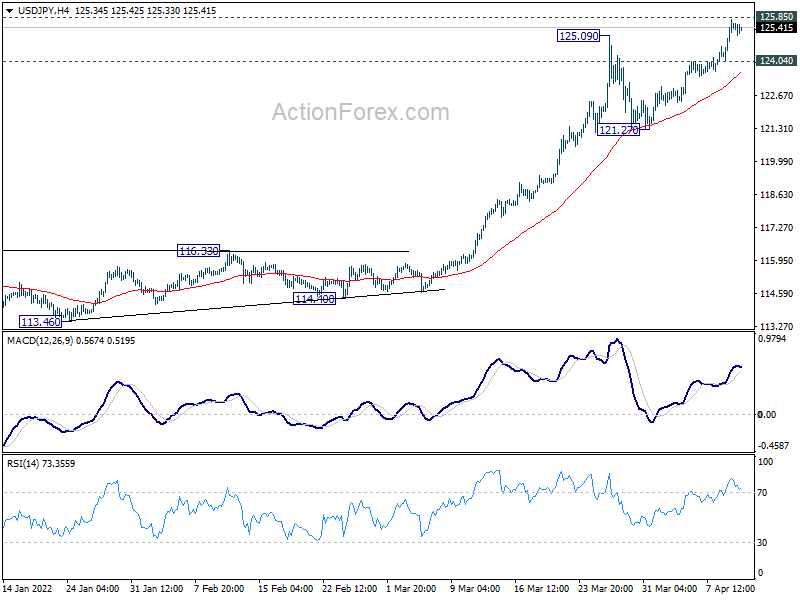

Technically, a main focus today is on USD/JPY’s reaction to 125.85 (2015 high). Strong break there will confirm resumption of up trend from 2011 low. Such development could come in reaction to strong CPI reading and extended rally in US treasury yields. Break of 124.04 minor support will turn USD/JPY into consolidations first, before setting up another attempt on 125.85.

{kind=link}

In Asia, at the time of writing, Nikkei is down -1.92%. Hong Kong HSI is down -0.36%. China Shanghai SSE is up 0.08%. Singapore Strait Times is down -0.77%. Japan 10-year JGB yield is up 0.004 at 0.243. Overnight DOW dropped -1.19%. S&P 500 dropped -1.69%. NASDAQ dropped -2.18%. 10-year yield rose 0.067 to 2.780.

Fed Evans: Optionality of not going too far too quickly is important

Chicago Fed President Charles Evans said yesterday that 50bps rate hike in May is “obviously worthy of consideration; perhaps it’s highly likely even if you want to get to neutral by December.” But he also emphasized, “the optionality of not going too far too quickly is important.”

He added that but the end of the year, Fed will know a lot more about inflation. “Is it going to be that some of these pricing pressures have crested, and they start coming down? Or are they going to stay high — or are they going to be higher?” Evans said. “And if it’s because of supply concerns, real resource pressures, there’s going to be a lot of gnashing-of-teeth angst over the inflation versus the concern for the economy. And I think finding the right balance is going to always be at a premium.”

Japan PPI rose 7.3% yoy in Mar, index at highest level since 1982

Japan corporate goods price index rose 7.3% yoy in March, slowed from 9.7% yoy but beat expectation of 9.3% yoy. The March index, at 112.0, was the highest level since December 1982. The yen-based import price index surged 33.4% yoy, signaling that Yen’s depreciation could be amplifying import inflation.

Separately, Finance Minister Shunichi Suzuki warned, “The government will closely monitor developments in the foreign exchange market, including the recent depreciation of the yen with a sense of vigilance. That includes the impact on the Japanese economy.”

Australia NAB business confidence rose to 16, strong rebound led by consumer demand

Australia NAB business confidence rose from 13 to 16 in March. Business conditions rose from 9 to 18. Looking at some details, trading conditions rose from 11 to 24. Profitability conditions rose from 5 to 13. Employment conditions rose from 8 to 12.

“A surge in business conditions headlined a really strong March survey,” said NAB Group Chief Economist Alan Oster. “Businesses reported very strong trading conditions and a sharp rise in profitability, which indicates demand is continuing to hold up as the economy rebounds from Omicron and growth gathers momentum.”

“Business confidence continued to improve in March, with little evidence of any adverse impact from events in Ukraine,” said Oster. “The outlook also strengthened in terms of forward orders which points to ongoing economic growth over coming months.”

“Overall, the results depict a very strong rebound, led by strong consumer demand.”

Looking ahead

UK employment data and Germany ZEW economic sentiment will highlight the European session. Germany will also release CPI final while France will release trade balance. Later in the day, US CPI will take center stage.

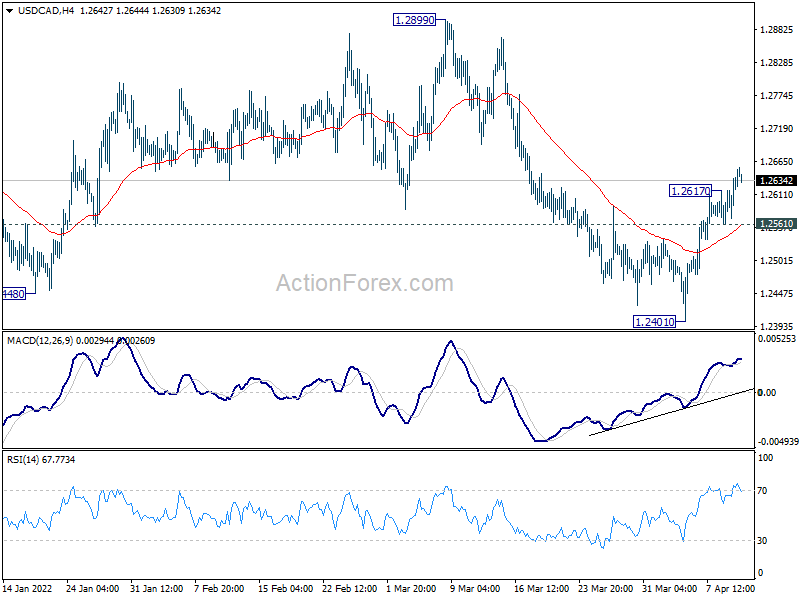

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2586; (P) 1.2614; (R1) 1.2661; More…

USD/CAD’s rebound from 1.2401 resumed by breaking through 1.2617 temporary top. Intraday bias is back on the upside. Sustained trading above 55 day EMA (now at 1.2629) will bring further rally to upper side of recent range at 1.2963. On the downside, though, below below 1.2561 minor support will turn bias back to the downside for 1.2401 support again.

{kind=link}

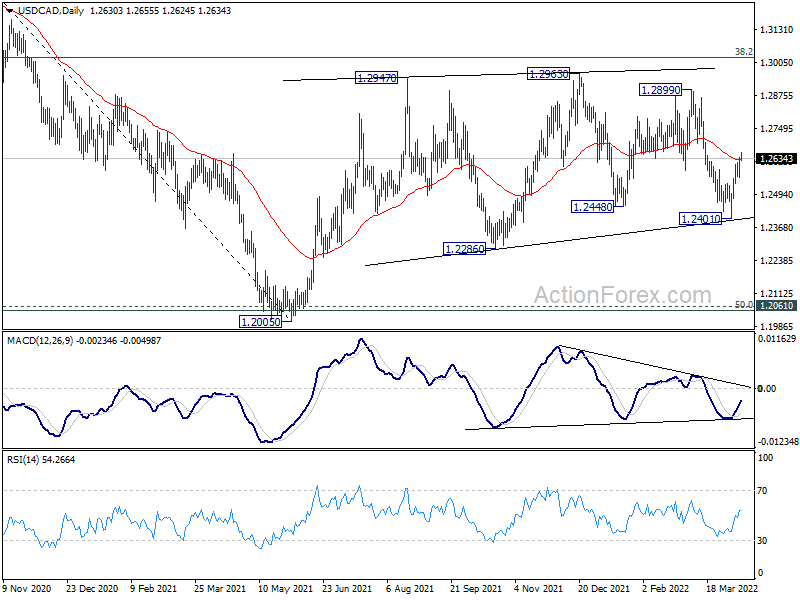

In the bigger picture, focus stays on 38.2% retracement of 1.4667 (2020 high) to 1.2005 (2021 low) at 1.3022. Sustained break there should confirm that the down trend from 1.4667 has completed after defending 1.2061 long term cluster support. Further rise would then be seen towards 61.8% retracement at 1.3650. However, rejection by 1.3022 will maintain medium term bearishness. Break of 1.2005 will resume the down trend from 1.4667 and that carries larger bearish implications too.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:00 | NZD | NZIER Business Confidence Q1 | -40 | -28 | ||

| 23:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Mar | -0.40% | 2.60% | 2.70% | |

| 23:50 | JPY | Bank Lending Y/Y Mar | 0.50% | 0.50% | 0.40% | |

| 23:50 | JPY | PPI Y/Y Mar | 9.50% | 9.30% | 9.30% | 9.70% |

| 01:30 | AUD | NAB Business Confidence Mar | 16 | 13 | ||

| 01:30 | AUD | NAB Business Conditions Mar | 18 | 9 | ||

| 06:00 | GBP | Claimant Count Change Mar | -41.1K | -48.1K | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) Feb | 3.80% | 3.90% | ||

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Feb | 5.70% | 4.80% | ||

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Feb | 3.70% | 3.80% | ||

| 06:00 | EUR | Germany CPI M/M Mar F | 2.50% | 2.50% | ||

| 06:00 | EUR | Germany CPI Y/Y Mar F | 7.30% | 7.30% | ||

| 06:45 | EUR | France Trade Balance (EUR) Feb | -9.3B | -8.0B | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment Apr | -48 | -39.3 | ||

| 09:00 | EUR | Germany ZEW Current Situation Apr | -35 | -21.4 | ||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Apr | -46.5 | -38.7 | ||

| 10:00 | USD | NFIB Business Optimism Index Mar | 95 | 95.7 | ||

| 12:30 | USD | CPI M/M Mar | 1.10% | 0.80% | ||

| 12:30 | USD | CPI Y/Y Mar | 8.30% | 7.90% | ||

| 12:30 | USD | CPI Core M/M Mar | 0.50% | 0.50% | ||

| 12:30 | USD | CPI Core Y/Y Mar | 6.60% | 6.40% |