Yields Rise, Yen Falls, Euro Trying a Rebound

Yen’s weakness remains the main theme today as selloff in major global treasuries continue. US 10-year yield breaches 2.9 handle while Germany 10-year yield breaches 0.94. UK 10-year Gilt yield is also heading towards 2% handle. Swiss Franc is following as second weakest together with Canadian Dollar. On the other hand, Aussie and leading the way up, followed by Euro, which is rebounding against Sterling and Franc. Dollar is mixed in between, awaiting the next guidance.

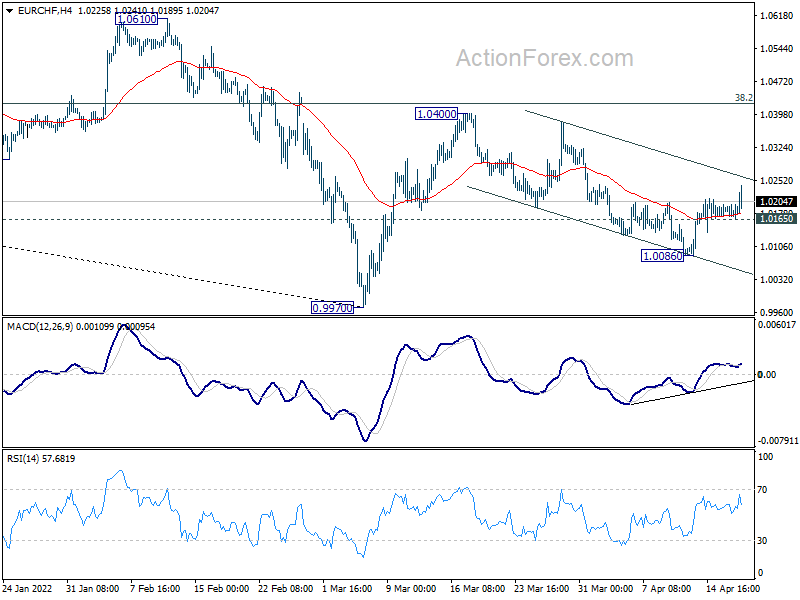

Technically, EUR/CHF’s rebound from 1.0086 extended higher today but retreated just ahead of near term falling channel resistance. For now further rise is in favor as long as 1.0165 minor support intact. Break of the channel resistance will set up further rally for 1.0400 resistance. However, break of 1.0165 will indicate rejection by the channel resistance and bring retest of 1.0086. EUR/CHF’s next move could be a hint on the sustainability of Euro’s rebound.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.42%. DAX is down -0.66%. CAC is down -1.16%. Germany 10-year yield is up 0.105 at 0.946. Earlier in Asia, Nikkei rose 0.69%. Hong Kong HSI dropped -2.28%. China Shanghai SSE dropped -0.05%. Singapore Strait Times rose 0.12%. Japan 10-year JGB yield rose 0.0033 to 0.245.

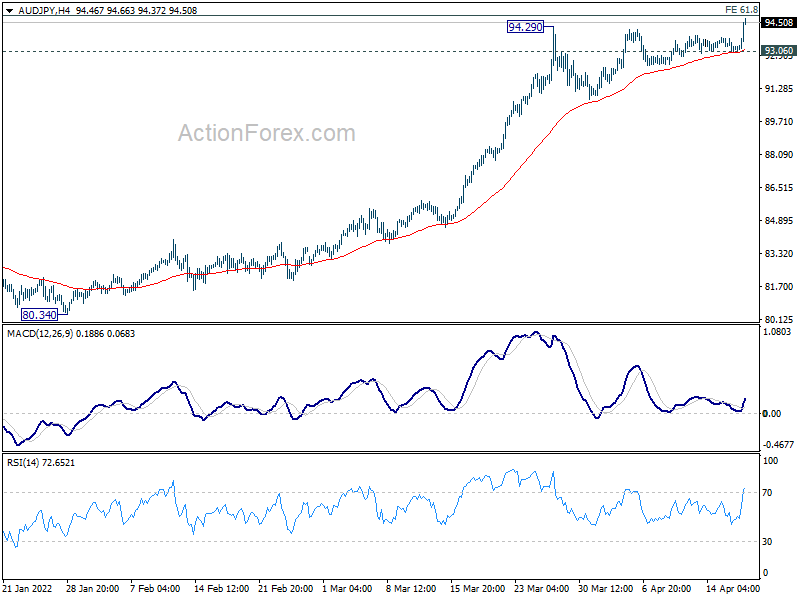

AUD/JPY resumes up trend, NZD/JPY to follow?

AUD/JPY’s up trend finally resumes today by breaking 94.29 near term resistance. Immediate focus is now on 61.8% projection of 59.85 (2020 low) to 85.78 from 78.77 at 94.79. Sustained break there could prompt upside acceleration, for next medium term target at 100% projection at 104.70, which is close to 105.42 (2013 high). However, break of 93.06 support will suggest rejection by 94.79 and bring deeper correction, back towards 55 day EMA (now at 88.55).

{kind=link}

{kind=link}

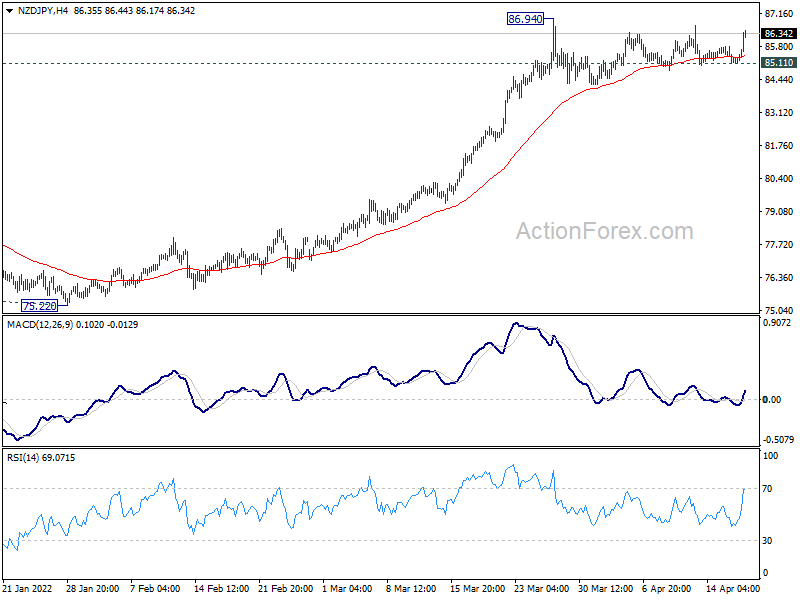

NZD/JPY is lagging behind and it’s still staying below 86.94 resistance. The next move will probably need from help from AUD/JPY. Break of 86.94 in NZD/JPY (following break of 94.79 in AUD/JPY) will resume larger up trend through 61.8% projection of 59.49 to 80.17 from 75.22 at 88.00. However, break of 85.11 (following AUD/JPY’s break of 93.06) will bring deeper pull back towards 55 day EMA (now at 82.09).

{kind=link}

{kind=link}

RBA minutes; Developments have brought forward liking timing of rate hike

In the minutes of April 5 meeting, RBA said, inflation in Australia had “picked up” and a “further increase was expected” with measures of underlying inflation in the March quarter expected to be above 3%. Wages growth had “picked up” too but “had been below rates likely to be consistent with inflation being sustainably at the target.” These developments have “brought forward the likely timing of the first increase in interest rates. ”

“Over coming months, important additional evidence will be available on both inflation and the evolution of labour costs. Consistent with its announced framework, the Board agreed that it would be appropriate to assess this evidence and other incoming information as it sets policy to support full employment in Australia and inflation outcomes consistent with the target.”

RBNZ Orr: It’s more about hiking sooner rather than more

RBNZ Governor Adrian Orr said in an IMF event, “we’ve been acting reasonably aggressively to tighten monetary conditions. We’ve provided strong forward guidance that we expect to be doing more rate rises over coming quarters.”

But he also noted, “that was more about doing it sooner rather than believing we have to do more,” he said. “It’s just getting on with it so people can understand what we are about.” Back in February, RBNZ projected that OCR would peak at 3.25% at the end of 2023.

Raising rates too high and “you really run the risk of having a sharper than needed slowdown in economic activity,” he said. “On the other hand, if you go too slow its inflation expectations that will get away from us.”

“At the moment, the balance of risks as far as the monetary policy committee is concerned is very much weighted to constraining those inflation expectations in the medium term,” he said. “We know the long-term cost of letting inflation expectations get away.”

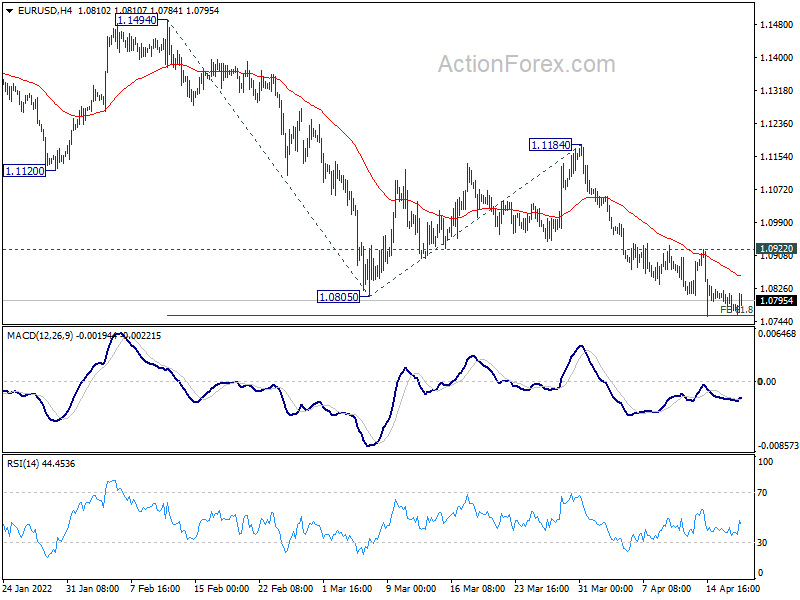

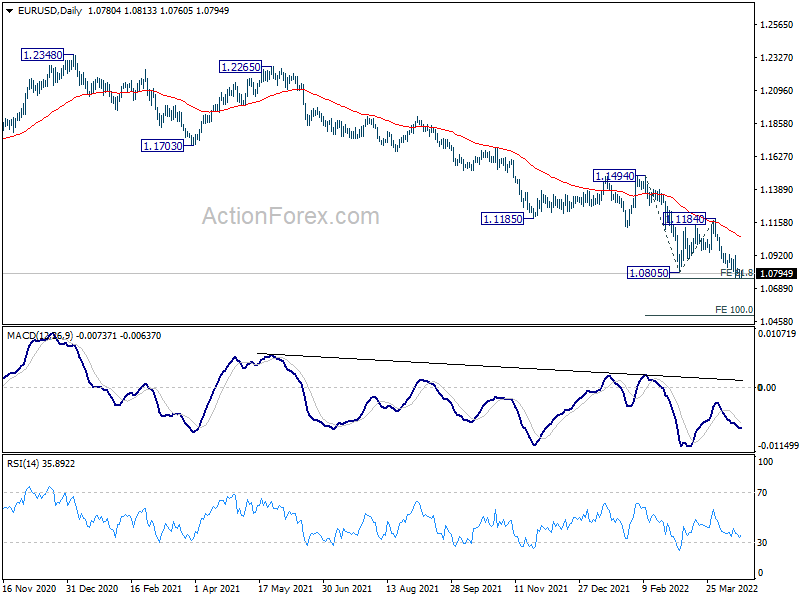

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0760; (P) 1.0791 (R1) 1.0812; More…

Intraday bias in EUR/USD is turned neutral as it recovers after hitting 61.8% projection of 1.1494 to 1.0805 from 1.1184. Further fall is expected as long as 1.0922 resistance holds. Firm break of 1.0758 will way to 100% projection at 1.0495. However, break of 1.0922 will turn bias back to the upside for stronger rebound towards 1.1184 resistance instead.

{kind=link}

In the bigger picture, the decline from 1.2348 (2021 high) is expected to continue as long as 1.1494 resistance holds. Firm break of 1.0635 (2020 low) will raise the chance of long term down trend resumption and target a retest on 1.0339 (2017 low) next. Nevertheless, break of 1.1494 will maintain medium term neutral outlook, and extending term range trading first.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Mar | 51.6 | 48.6 | 48.9 | |

| 01:30 | AUD | RBA Meeting Minutes | ||||

| 04:30 | JPY | Industrial Production M/M Feb | 2.00% | 0.10% | 0.10% | |

| 12:15 | CAD | Housing Starts Y/Y Mar | 246K | 249K | 247K | 250K |

| 12:30 | USD | Building Permits Mar | 1.87M | 1.83M | 1.86M | |

| 12:30 | USD | Housing Starts Mar | 1.79M | 1.74M | 1.77M | |

| 12:30 | CAD | Foreign Securities Purchases (CAD) Feb | 7.44B | 15.23B | 13.49B |