CAD Surges after CPI Beat Expectations, Dollar Corrects Lower

Canadian Dollar surges in early US session after much stronger than expected consumer inflation data, which supports more aggressive tightening by BoC. Other commodity currencies are also strong. On the other hand, Dollar is trading broadly lower as recent rally lost momentum, in particular against Yen. Euro is also soft, together with Sterling and Swiss Franc. In other markets, European stocks are trading mildly higher while US futures point to higher open. Global benchmark treasury yields are paring recent sharp gains.

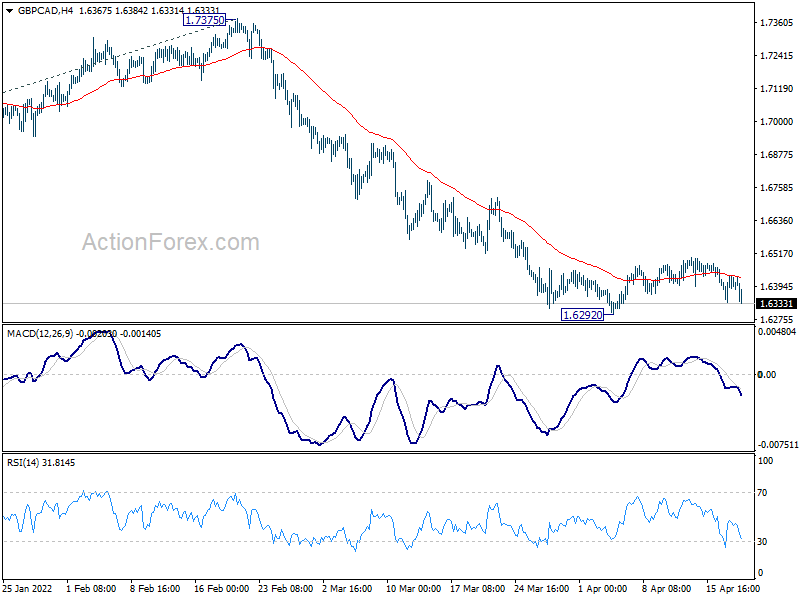

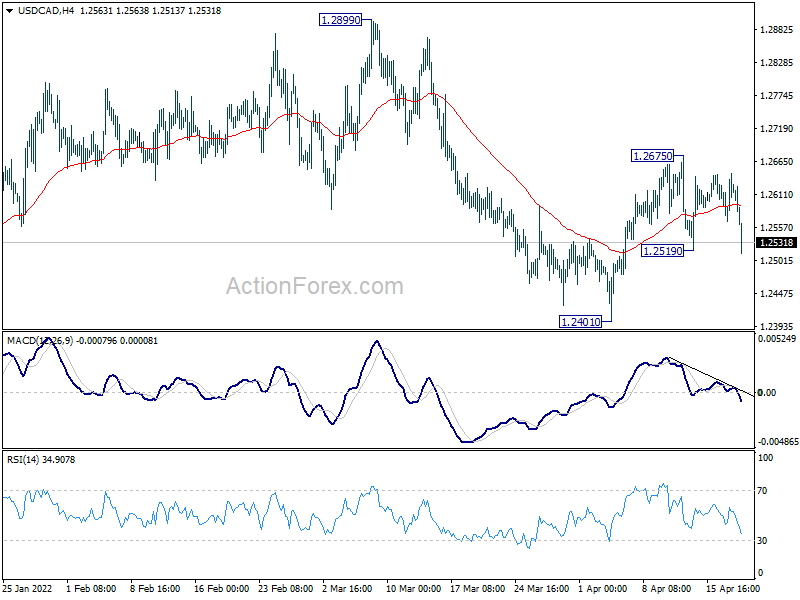

Technically, a focus for the rest of the day would be on whether Canadian Dollar could extend the post CPI rise. As for USD/CAD, it will need to break through 1.2519 minor support. EUR/CAD will need to break through 1.3541 temporary low to resume recent down trend. Similarly, GBP/CAD will also break through 1.6292 temporary low to resume down trend.

{kind=link}

In Europe, at the time of the writing, FTSE is up 0.21%. DAX is up 1.22%. CAC is up 1.44%. Germany 10-year yield is down -0.045 at 0.868. Earlier in Asia, Nikkei rose 0.86%. Hong Kong HSI dropped -0.40%. China Shanghai SSE dropped -1.35%. Singapore Strait Times rose 0.85%. Japan 10-year JGB yield rose 0.0069 to 0.248.

Canada CPI rose to 6.7% yoy in Mar, highest since 1991

Canada CPI rose 1.4% mom in March, above expectation of 0.9% mom. That’s the largest monthly increase since January 1991. For the 12-month period, CPI accelerated from 5.7% yoy to 6.7% yoy, well above expectation of 6.1% yoy. That’s also the largest annual rise since January 1991.

CPI common rose from 2.7% yoy to 2.8% yoy, above expectation of 2.7% yoy. CPI median rose from 3.5% yoy to 3.8% yoy, above expectation of 3.5% yoy. CPI trimmed rose from 4.4% yoy to 4.7% yoy, above expectation of 4.3% yoy.

Statistics Canada said: “Inflationary pressure remained widespread in March, as prices rose across all eight major components. Prices increased against the backdrop of sustained price pressure in Canadian housing markets, substantial supply constraints and geopolitical conflict, which has affected energy, commodity, and agriculture markets.”

ECB Kazaks: A rate increase in July is possible

ECB Governing Council member Martins Kazaks said in a Bloomberg interview, that it’s possible to hike interest rate in July. Meanwhile, QE could end at the end of June but the policy members will have to discuss it with new economic forecasts on hand.

“A rate increase in July is possible, and I have no reason to disagree with what markets are pricing for the second half of the year,” he said. “We are on a solid path of policy normalization” where “we step-by-step gradually get to zero and then above”.

“Gradual doesn’t mean slow,” added Kazaks. “It doesn’t mean being consciously behind the curve. No, it just means checking if taken policy measures are appropriate.”

“We haven’t seen any major elements of stress in financial markets, which makes me think that ending QE early in the third quarter is possible and appropriate,” Kazaks said. “Whether it could already happen at the end of June, we’ll have to discuss when we get new forecasts.”

Eurozone industrial production rose 0.7% mom in Feb, EU up 0.6% mom

Eurozone industrial production rose 0.7% mom in February, below expectation of 0.8% mom. Production of durable consumer goods rose by 2.7%, non-durable consumer goods by 1.9% and intermediate goods by 0.9%, while production of capital goods fell by -0.1% and energy by -1.1%.

EU industrial production rose 0.6% mom. Among Member States for which data are available, the highest monthly increases were registered in Italy (+4.0%), Croatia (+2.7%) and Ireland (+2.4%). The largest decreases were observed in Slovenia (-8.3%), Lithuania (-3.8%) and Malta (-2.7%).

Eurozone exports rose 17.0% yoy in Feb, imports rose 38.8% yoy

Eurozone goods exports rose 17.0% yoy to EUR 215.8B in February. Imports rose 38.8% yoy to EUR 223.4B. Trade deficit came in at EUR -7.6B. Intra-Eurozone trade rose 25.6% yoy to EUR 202.5B.

In seasonally adjusted term, Eurozone exports rose 0.8% mom to EUR 223.6B. Imports rose 1.5% mom to EUR 233.1B. trade deficit widened from EUR -7.7B to EUR -9.4B, larger than expectation of EUR -6.5B. Intra-Eurozone trade rose from EUR 202.7B to EUR 205.8B.

Australia Westpac leading index rose to 1.71, highest since last May

Australia Westpac-MI leading index rose from 1.02% to 1.71% in March. That’s the fastest growth rate since May 2021. The data are consistent with Westpac’s expectation of around 5.5% GDP growth in 2022, with more than 70% of that being concentrated in Q2 and Q3.

Westpac expects RBA to be on hold at May 3 meeting, but be prepared to move interest rate at June 7 meeting. It expects a hike of 15bps in June, with 25bps hikes at most subsequent meetings to reach 1.25% at the end of 2022. In 2023, it expects three further 25bps hikes with interest rate peaking at 2% in June.

Japan exports rose 14.7% yoy in Mar, imports surged 31.2% yoy

Japan exports rose 14.7% yoy to JPY 8461B in March. That’s the 13th straight month of rise, reflecting robust demand for semiconductor manufacturing devices in Taiwan and steel product shipments to Vietnam. Imports rose 31.2% yoy to JPY 8873B. Petroleum imports jumped 69.7% yoy, the 12th straight month of rise. Trade deficit came in as JPY -412B, the 8th straight month of deficit, longest streak since 2015.

In seasonally adjusted term, exports rose 1.7% mom to JPY 7570B. Imports dropped -0.5% mom to JPY 8470B. Trade deficit came in at JPY -900B.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2578; (P) 1.2612; (R1) 1.2656; More…

Immediate focus is on 1.2519 minor support in USD/CAD. Break there will target 1.2401 support first. Firm break there will resume larger decline from 1.2899 to retest 1.2005 low. On the upside, though, break of 1.2675 will flip bias back to the upside for 1.2899 resistance instead.

{kind=link}

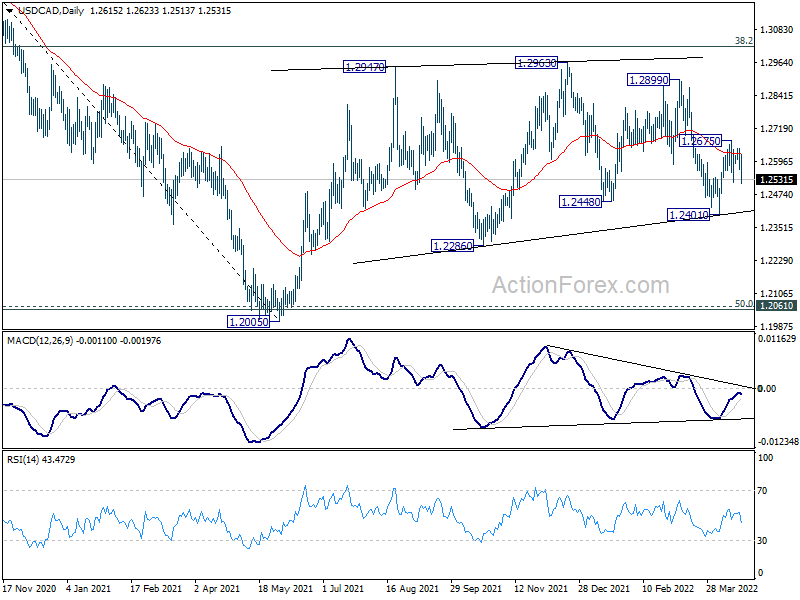

In the bigger picture, focus stays on 38.2% retracement of 1.4667 (2020 high) to 1.2005 (2021 low) at 1.3022. Sustained break there should confirm that the down trend from 1.4667 has completed after defending 1.2061 long term cluster support. Further rise would then be seen towards 61.8% retracement at 1.3650. However, rejection by 1.3022 will maintain medium term bearishness. Break of 1.2005 will resume the down trend from 1.4667 and that carries larger bearish implications too.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Mar | -0.90T | -0.48T | -1.03T | -1.07T |

| 00:30 | AUD | Westpac Leading Index M/M Mar | 0.30% | -0.20% | 0.40% | |

| 04:30 | JPY | Tertiary Industry Index M/M Feb | -1.30% | 0.30% | -0.70% | -0.20% |

| 06:00 | EUR | Germany PPI M/M Mar | 4.90% | 3.40% | 1.40% | |

| 06:00 | EUR | Germany PPI Y/Y Mar | 30.90% | 26.60% | 25.90% | |

| 08:00 | EUR | Italy Trade Balance (EUR) Feb | -1.66B | -4.23B | -5.05B | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Feb | -9.4B | -6.5B | -7.7B | |

| 09:00 | EUR | Eurozone Industrial Production M/M Feb | 0.70% | 0.80% | 0.00% | -0.70% |

| 12:30 | CAD | CPI M/M Mar | 1.40% | 0.90% | 1.00% | |

| 12:30 | CAD | CPI Y/Y Mar | 6.70% | 6.10% | 5.70% | |

| 12:30 | CAD | CPI Common Y/Y Mar | 2.80% | 2.70% | 2.60% | 2.70% |

| 12:30 | CAD | CPI Median Y/Y Mar | 3.80% | 3.50% | 3.50% | |

| 12:30 | CAD | CPI Trimmed Y/Y Mar | 4.70% | 4.30% | 4.30% | 4.40% |

| 13:30 | CAD | New Housing Price Index M/M Mar | 1.20% | 0.70% | 1.10% | |

| 14:00 | USD | Existing Home Sales Mar | 5.80M | 6.02M | ||

| 14:30 | USD | Crude Oil Inventories | 3.0M | 9.4M | ||

| 18:00 | USD | Fed’s Beige Book |