USD/JPY Retreating on Talks of BoJ Intervention, Dollar Softens Too

Japan’s benchmark 10-year JGB yield is pulled above BoJ’s cap of 0.25% in Asian session today. That triggered intervention by BoJ to defend the ceiling. At the same time, USD/JPY breached 129 handle but quickly retreated, on talks that BoJ could also intervene at around 130. But judging from overall price actions, the pull back in USD/JPY is probably more due to loss of momentum in Dollar.

The greenback is so far trading as the weakest one for today, followed by Swiss Franc and then Euro. Australian Dollar is leading New Zealand Dollar higher, but Canadian is weak. Sterling is mixed for now.

Technically, EUR/USD, GBP/USD and AUD/USD are all losing downside momentum as seen in 4 hours MACD. It’s early to call for a near term reversal. But attention will be on 1.0922 minor resistance in EUR/USD, 1.3165 minor resistance in GBP/USD, and 0.7492 minor resistance in AUD/USD. Break of these levels could prompt more sustainable selling in the greenback.

In Asia, at the time of writing, Nikkei is up 0.91%. Hong Kong HSI is up 0.82%. China Shanghai SSE is down -0.21%. Singapore Strait Times is up 0.70%. Japan 10-year JGB yield is up 0.0069 at 0.255. Overnight, DOW rose 1.45%. S&P 500 rose 1.61%. NASDAQ rose 2.15%. 10-year yield rose 0.051 to 2.913.

Fed Evans expects interest rate at 2.25-2.50% by year end

Chicago Fed President Charles Evans said yesterday that he expected interest rate to be above neutral at 2.25-2.50% by the end of the year.

“That’s my expectation, when I see that, taking out special factors, I’m still left with 3 to 3.5% inflation” by the end of 2022, he said. “That’s not what we want. If we’re at a 2.5% inflation rate, I think we have more things to ponder there.”

“By December, we’re going to get more data on the micro aspects of the high inflation, price increases, how much is it broadening out,” Evans said. “By that time, we’re at neutral, and to the extent we don’t see it coming down, we’re going beyond neutral, absolutely.”

Fed Bostic: Really important to get to neutral in expeditious way

Atlanta Fed President Raphael Bostic told CNBC yesterday, “I think it’s really important that we get to neutral and do that in an expeditious way.”

“I really have us looking at one and three-quarters by the end of the year, but it could be slower depending on how the economy evolves and we do see greater weakening than I’m seeing in my baseline model,” he said.

“This is one reason why I’m reluctant to really declare that we want to go a long way beyond our neutral place, because that may be more hikes than are warranted given sort of the economic environment.”

Australia Westpac leading index rose to 1.71, highest since last May

Australia Westpac-MI leading index rose from 1.02% to 1.71% in March. That’s the fastest growth rate since May 2021. The data are consistent with Westpac’s expectation of around 5.5% GDP growth in 2022, with more than 70% of that being concentrated in Q2 and Q3.

Westpac expects RBA to be on hold at May 3 meeting, but be prepared to move interest rate at June 7 meeting. It expects a hike of 15bps in June, with 25bps hikes at most subsequent meetings to reach 1.25% at the end of 2022. In 2023, it expects three further 25bps hikes with interest rate peaking at 2% in June.

Japan exports rose 14.7% yoy in Mar, imports surged 31.2% yoy

Japan exports rose 14.7% yoy to JPY 8461B in March. That’s the 13th straight month of rise, reflecting robust demand for semiconductor manufacturing devices in Taiwan and steel product shipments to Vietnam. Imports rose 31.2% yoy to JPY 8873B. Petroleum imports jumped 69.7% yoy, the 12th straight month of rise. Trade deficit came in as JPY -412B, the 8th straight month of deficit, longest streak since 2015.

In seasonally adjusted term, exports rose 1.7% mom to JPY 7570B. Imports dropped -0.5% mom to JPY 8470B. Trade deficit came in at JPY -900B.

Looking ahead

Germany PPI, Italy trade balance, Eurozone trade balance and industrial production will be released in European session. Later in the day, Canada CPI will take the spotlight. US will release existing home sales and Fed’s Beige book report.

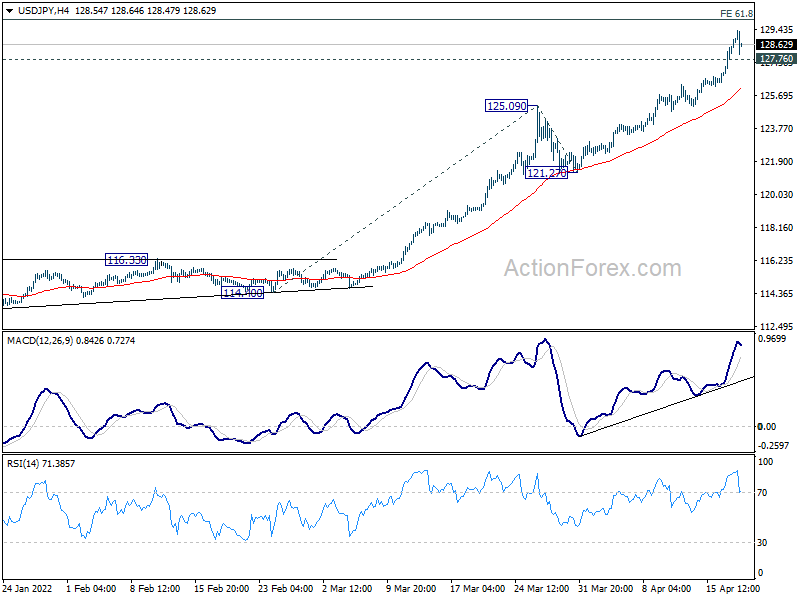

USD/JPY Daily Outlook

Daily Pivots: (S1) 127.58; (P) 128.28; (R1) 129.58; More…

USD/JPY retreats after hitting 129.39, but intraday bias stays on the upside with 127.76 minor support intact. Current up trend should target 130.04 long term projection level next. On the downside, break of 127.76 minor support will bring deeper pull back. But near term outlook will remain bullish as long as 125.09 resistance turned support holds.

{kind=link}

In the bigger picture, the break of 125.85 resistance (2015 high) suggests that whole up trend from 75.56 (2011 low) is resuming. Further rise should be seen to 61.8% projection of 75.56 (2011 low) to 125.85 (2015 high) from 98.97 at 130.04. Sustained break there wave the way to 147.68 (1998 high). For now, this will remain the favored case as long as 121.27 support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Mar | -0.90T | -0.48T | -1.03T | -1.07T |

| 00:30 | AUD | Westpac Leading Index M/M Mar | 0.30% | -0.20% | 0.40% | |

| 04:30 | JPY | Tertiary Industry Index M/M Feb | -1.30% | 0.30% | -0.70% | -0.20% |

| 06:00 | EUR | Germany PPI M/M Mar | 3.40% | 1.40% | ||

| 06:00 | EUR | Germany PPI Y/Y Mar | 26.60% | 25.90% | ||

| 08:00 | EUR | Italy Trade Balance (EUR) Feb | -4.23B | -5.05B | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Feb | -6.5B | -7.7B | ||

| 09:00 | EUR | Eurozone Industrial Production M/M Feb | 0.80% | 0.00% | ||

| 12:30 | CAD | CPI M/M Mar | 0.90% | 1.00% | ||

| 12:30 | CAD | CPI Y/Y Mar | 5.70% | |||

| 12:30 | CAD | CPI Common Y/Y Mar | 2.70% | 2.60% | ||

| 12:30 | CAD | CPI Median Y/Y Mar | 3.50% | 3.50% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Mar | 4.30% | 4.30% | ||

| 13:30 | CAD | New Housing Price Index M/M Mar | 6.10% | 1.10% | ||

| 14:00 | USD | Existing Home Sales Mar | 5.80M | 6.02M | ||

| 14:30 | USD | Crude Oil Inventories | 3.0M | 9.4M | ||

| 18:00 | USD | Fed’s Beige Book |