Dollar Powered Up, Fed to Hike 50bps in May and 75bps in Jun?

Speculations on aggressive Fed tightening intensified sharply last week after a chorus of hawkish comments from policy markets. Markets are indeed pricing in near 70% chance of federal funds rate at 1.50-1.75% by the end of first half, i.e., 125bps above current level. Stocks tumbled sharply towards the end, with DOW suffering the worst day since 2020 on Friday.

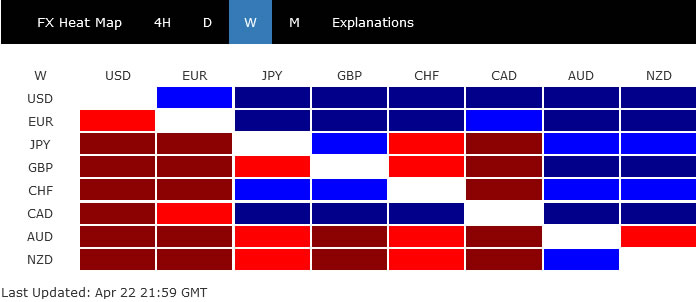

In the currency markets, Dollar ended broadly higher as the best performer, as supported by both Fed expectations and risk aversion. Euro was the second strongest after some ECB members talked up the chance of a July rate hike. Commodity Aussie and Kiwi ended as the biggest losers. Yen consolidated in tight range while European majors and Loonie were mixed.

{kind=link}

Fed to hike 50bps in May, then 75bps in June?

There should be a consensus among Fed policymakers on the need to “front-load” some of the rate hikes, to “expedite” to neutral. Whether interest will end up at 2.50% or 3.50% by the end of the year will very much depends on incoming data and developments. But the rate hikes should come in faster and earlier.

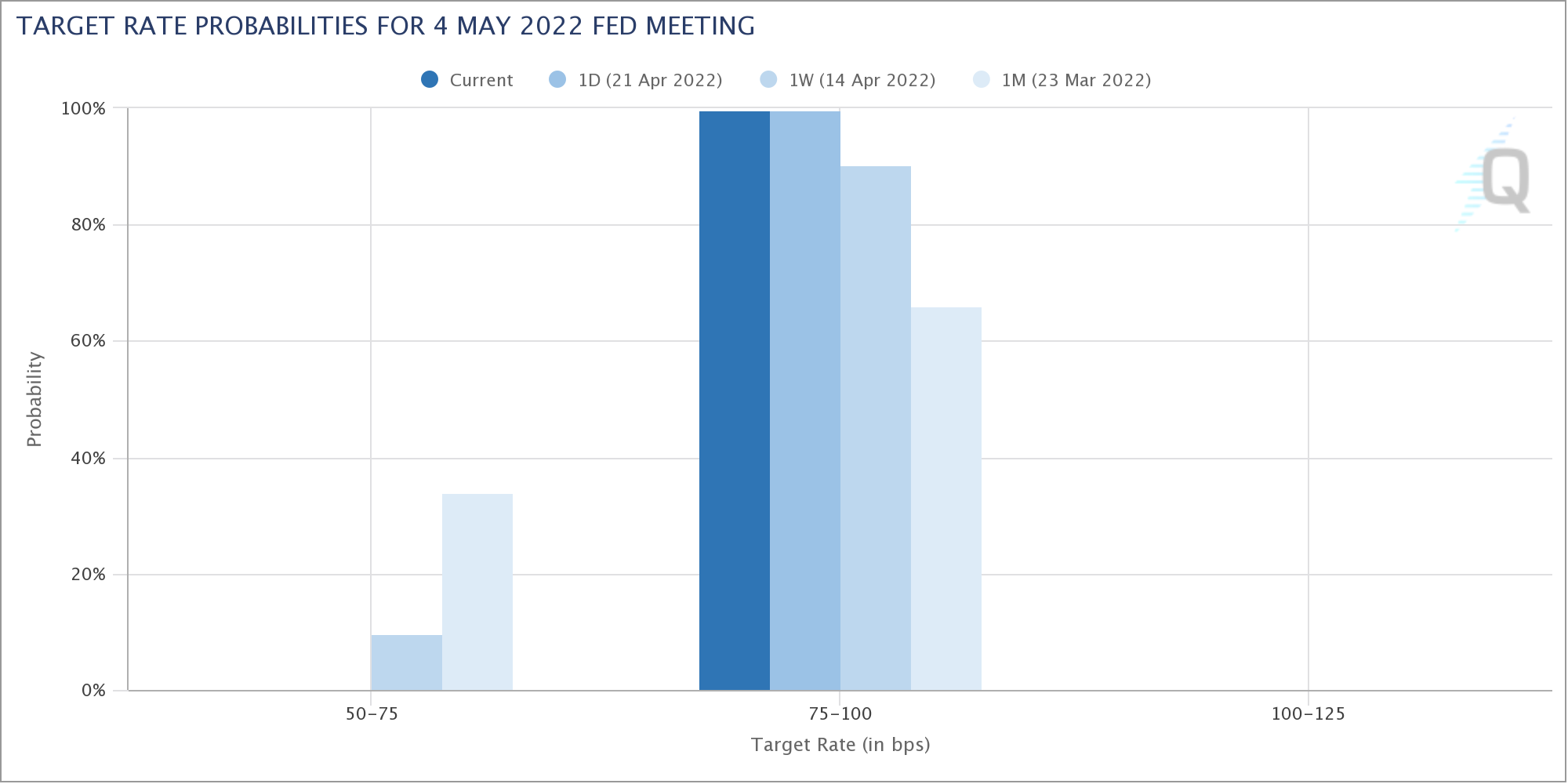

Traders added to their bets on a 50bps rate hike by Fed in May, after even Chair Jerome Powell said it’s “on the table”. Fed fund futures are now pricing in 99.6% chance of that, bring interest rate to 0.75-100%, comparing to 66% a month ago.

{kind=link}

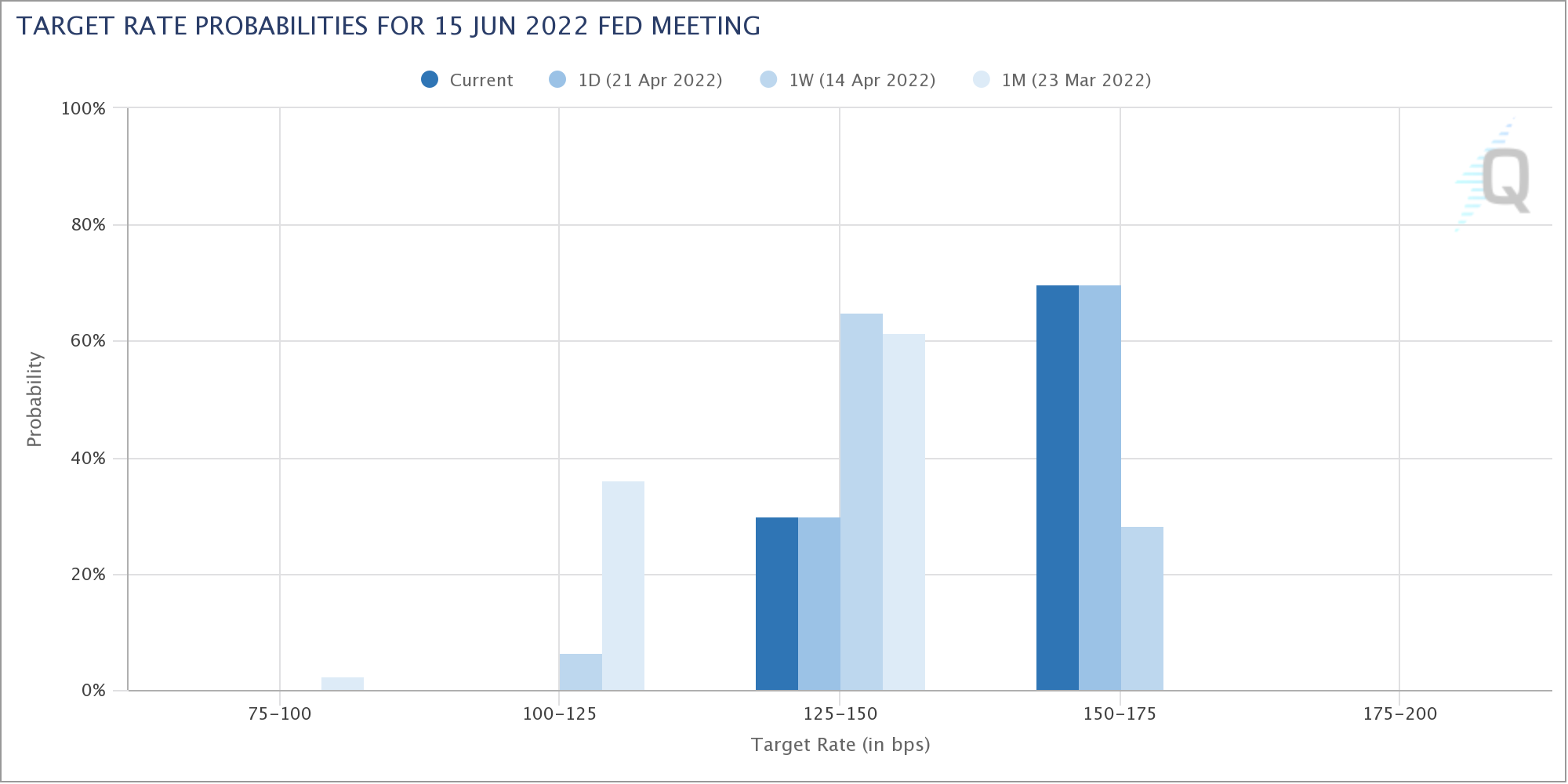

But more importantly, markets are pricing in near 70% chance of interest rate ending at 1.50-1.75% after June meeting (comparing to 0% a month ago). That is, traders are betting on a 75 bps rate hike at the June meeting. That’s pretty aggressive.

{kind=link}

S&P 500 to extend medium term correction through 4000 handle

US stocks tumbled sharply towards the end of last week, as investors finally reacted to the speculations of aggressive Fed tightening. The development in S&P 500 suggest that rebound from 4115.65, as the second leg of the corrective pattern from 4818.62, has completed at 4637.30 already.

The corrective pattern is now in its third leg. Further decline should be seen through 4114.65 low to 100% protection of 4818.62 to 4114.65 from 4637.30 at 3933.32, i.e, slightly below 4000 handle. This will remain the favored case as long as 55 day EMA (now at 4449.41) holds.

{kind=link}

But it should be emphasized that overall outlook isn’t too bearish. Price actions from 4818.62 are seen as correcting the up trend from 2191.86 (2020 low) only. As all the supply chain issues, war, inflation fade, and with monetary policy setting back to prepandemic levels (or a bit tighter), dusts will settle. Downside of SPX’s correction should be contained by 38.2% retracement of 2191.86 to 4818.62 at 3815.20 to bring rebound.

{kind=link}

10-year yield might start to feel heavy above 3%

10-year yield extended recent up trend and closed above 2.9 handle at 2.906. While some volatility cannot be ruled out, in any case, near term outlook will remain bullish as long as 2.646 support holds. But TNX could start to feel heavy between 3.0 and 3.248 (2018 high), which could limit the upside until further development. That could, nonetheless, continue to provide support to Dollar, in particular against Yen.

{kind=link}

Also, it should noted again that the multi-decade channel resistance as seen in the monthly chart is considered decisive violated already. Focus is now on 3.248. Firm break there would confirm the start of a new era, of finally a long term trend of rising treasury yield and interest rates, probably accompanied by persistently strong inflation.

{kind=link}

Dollar index done with 100 psychological level, extending up trend

Dollar index rode on risk aversion and Fed expectations and resumed recent up trend last week. It’s probably finally having the momentum to get rid of 100 handle with some conviction. In any case, outlook will stay bullish as long as 99.41 resistance turned support holds, next target is 102.99/103.82 long term resistance zone (2020 and 2016 highs respectively).

{kind=link}

More importantly, the odds of resuming the long term up trend from 70.69 (2008 low) is building up. 102.99/103.82 could still prove to be too much for DXY for the first attempt, and a set back from there cannot be ruled out. Yet, it could be just a matter of time (from medium term perspective) that this resistance zone would be taken out. In that case, the next long term target will be 61.8% projection of 72.69 to 103.82 from 89.20 at 108.43.

{kind=link}

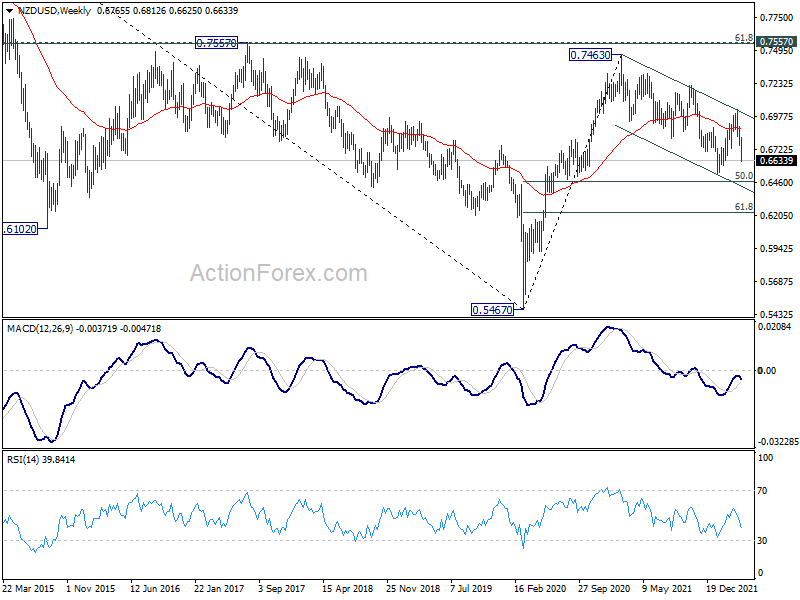

NZD/USD and AUD/USD to extend medium term correction

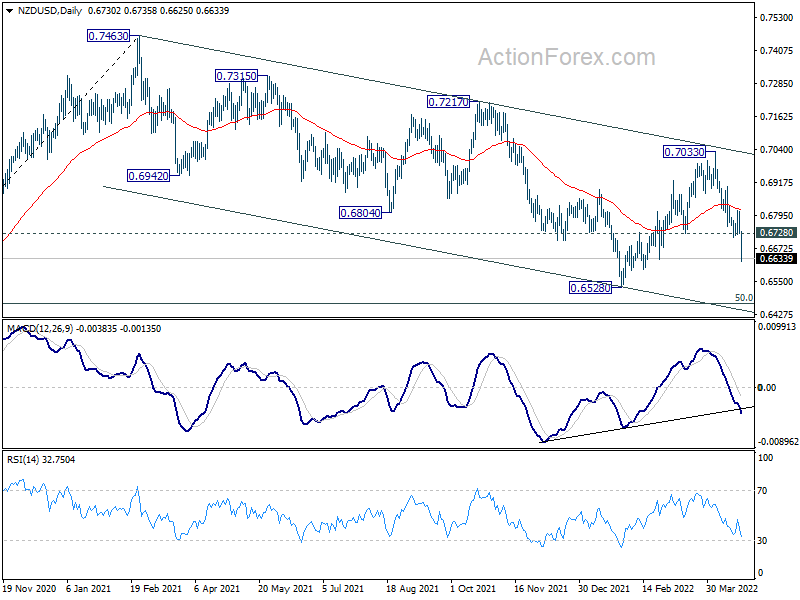

Aussie and Kiwi were the worst performers last week, suffering much from risk aversion. NZD/USD’s strong break of 0.6728 support should confirm completion of rebound from 0.6528 at 0.7033, after failing medium term channel resistance. Deeper decline is expected through 0.6528 low to resume the whole decline from 0.7463.

The fall from 0.7463 is seen as a correction to up trend from 0.5467, and could complete only after breaking 50% retracement of 0.5467 to 0.7463 at 0.6465.

{kind=link}

{kind=link}

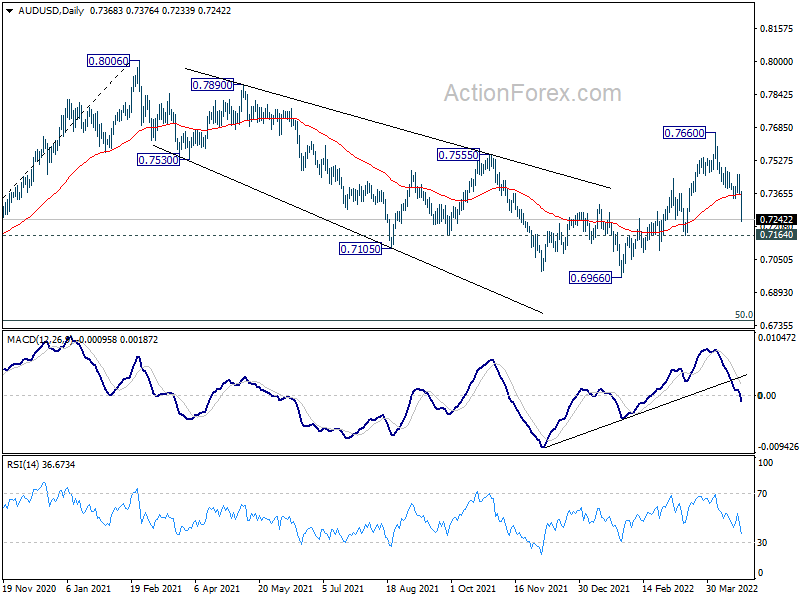

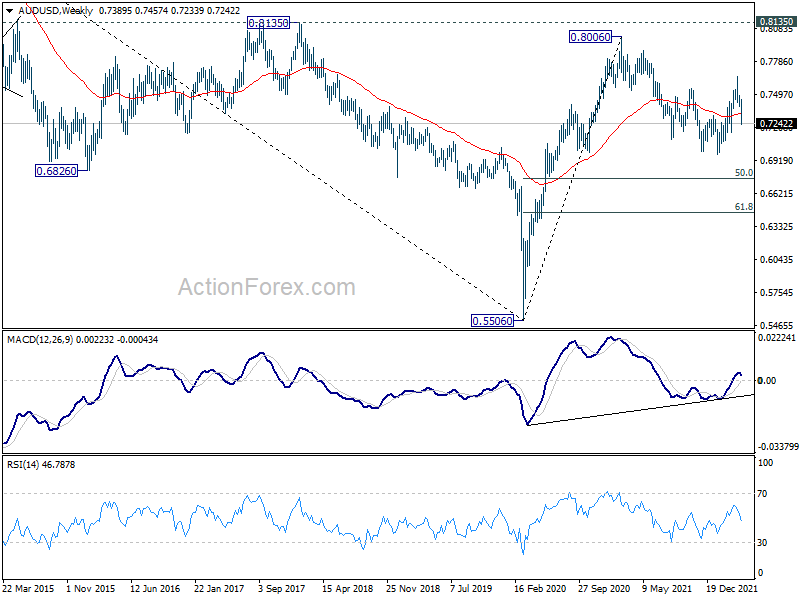

AUD/USD also tumbled sharply last week. 0.7164 structural support now looks rather shaky (considering that NZD/USD has broken corresponding level already). Break of 0.7164 will argue that the whole corrective decline from 0.8006 high is still in progress, and it’s starting the third leg. Such correction could complete only after after a take on 50% retracement of 0.5506 to 0.8006 at 0.6756.

{kind=link}

{kind=link}

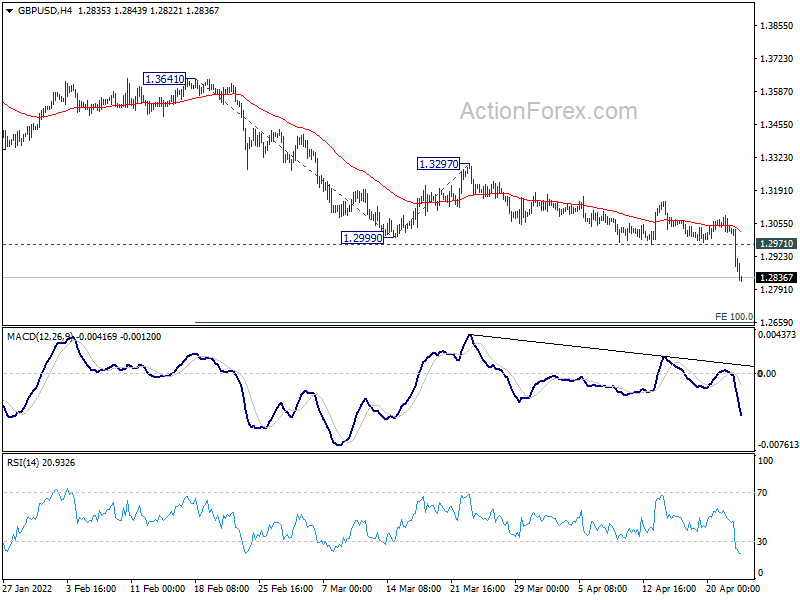

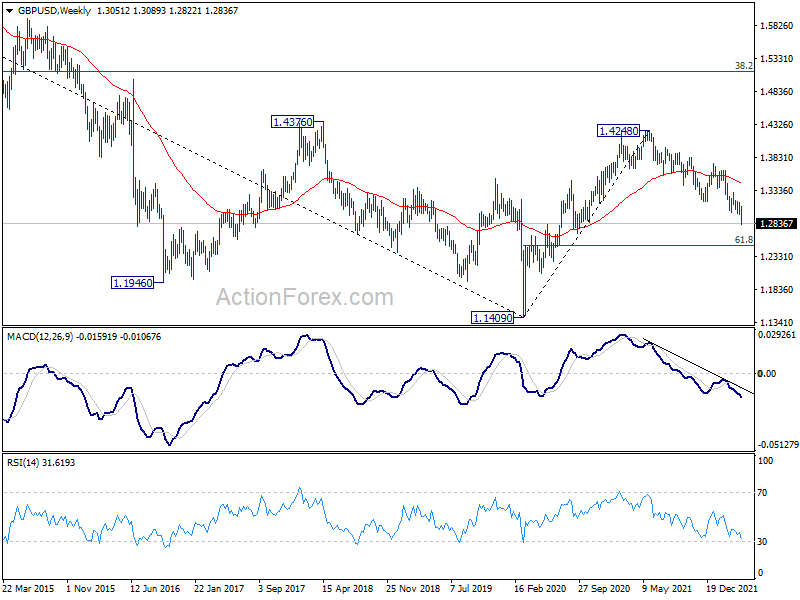

GBP/USD Weekly Outlook

GBP/USD’s down trend resumed last week and hit as low as 1.2822. Initial bias stays on the downside this week for 100% projection of 1.3641 to 1.2999 from 1.3297 at 1.2655 next. On the upside, above 1.2971 minor resistance will turn intraday bias neutral and bring consolidation first, before staging another decline.

{kind=link}

In the bigger picture, rise from 1.1409 (2020 low) has completed at 1.4248, ahead 1.4376 long term resistance (2018 high). Decline from 1.4248 could still be a corrective move, or it could be the start of a long term down trend. In either case, deeper decline would be seen back to 61.8% retracement of 2.1161 to 1.1409 at 1.2493. In any case, break of 1.3158 support turned resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish in case of rebound.

{kind=link}

In the longer term picture, rebound from 1.1409 long term bottom could have completed at 1.4248 already, well ahead of 38.2% retracement of 2.1161 to 1.1409 at 1.5134. The development argues that price actions from 1.1409 are developing into a corrective pattern only. That is, long term bearishness is retained for resuming the downside from 2.1161 (2007 high) at a later stage.

{kind=link}

{kind=link}