Dollar Rally Continues on Risk-Off Sentiment, Euro to Break Support?

Risk aversion dominates the markets in Asia with concerns on more tough lockdowns in China, including the capital city of Beijing. Dollar jumps broadly higher, with Yen and Swiss Franc as distant second and third. Aussie and Kiwi are extending last week’s decline, trading as the worst ones for today so far. Euro is the next weakest, playing catch-up, with little support from new that Emmanuel Macron was re-elected for a second term as French President. Sterling is also looking vulnerable.

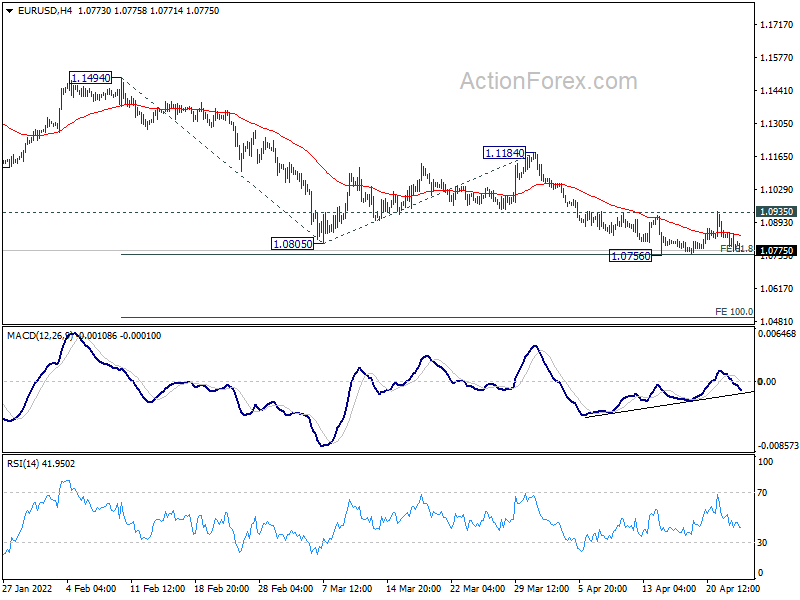

Technically, one major focus today is 1.0756 support in EUR/USD. Firm break there will resume larger down trend from 1.2348. That would align the bearish outlook with Sterling and Franc against the greenback. Such development should also seal the case for underlying bullish momentum in Dollar, probably for the medium term too.

{kind=link}

In Asia, at the time of writing, Nikkei is down -1.84%. Hong Kong HSI is down -2.86%. China Shanghai SSE is down -2.62%. Singapore Strait Times is down -0.25%. Japan 10-year JGB yield is up 0.0020 at 0.252.

Ethereum breaking down, bitcoin to follow

Ethereum follows broad based risk-off sentiment lower today and dips to as low as 2838.30 so far. The development is in-line with the view that corrective pattern from 2157.05 has completed with three waves up to 3577.70. Further decline is now expected as long as 3177.25 resistance holds.

Sustained break of near term channel support, and then 2490.05 support, should sent the stage for resumption of whole down trend form 4863.75. Next target is 61.8% projection of 4863.75 to 2157.04 from 3577.70 at 1804.95.

{kind=link}

{kind=link}

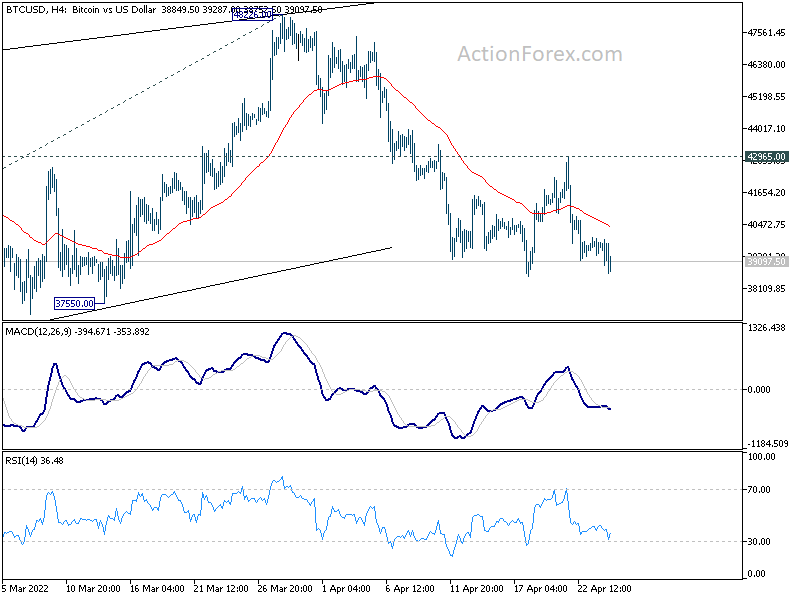

Similarly, bitcoin should follow and break through 38539 support soon, to resume the decline from 48226. Further break of 37550 support should set the stage for resumption of down trend from 68986. Next target is 61.8% projection of 68986 to 33000 from 48226 at 25986.

{kind=link}

{kind=link}

WTI crude oil falls on concern of Beijing lockdown

WTI crude oil falls notably in Asian session, following general risk-off sentiment. It’s reported that more than a dozen of buildings are now also under lockdown the largest district of Chaoyang in Beijing, China’s capital. That raised concerns that Beijing could be put under tough and continued lockdown like Shanghai soon, which would then weigh further on oil demand.

WTI crude oil is seen as in the fifth leg of a triangle corrective pattern which started at 131.82, back in early March. Deeper fall should be seen in the near term towards lower side of the pattern at 93.47. A breach of that level could be seen but it should be relatively brief, and contained above key support level at 85.92.

The main question is that after the corrective pattern completes, whether the next rally could break through 131.82 high. But in any case, the next rise should be the last in current up trend and should then set up a medium term corrective phase which lasts much longer.

{kind=link}

{kind=link}

ECB said to be keen on starting rate hike in Jul

According to a Reuters report, some unnamed ECB sources said ECB policymakers were keen to end the asset purchases in June, and start raising interest rate soon. Some expected interest hike to start as soon as in July. The main policy rate could be back to neutral at around 1.00-1.25% by the end of the year. That would also lift the deposit rate back into positive territory for the first time since 2014.

ECB President Christine Lagarde sounded more cautious with her comments, however. She just said last Friday, “If the situation continues as predicated at the moment, there is a strong likelihood that rates will be hiked before the end of the year. How much, now many times, remains to be seen and will be data dependent.”

BoJ meeting, GDP and CPI data to highlight the week

BoJ will meet this week and it’s clear that it will maintain the current ultra-loose monetary policy. Nevertheless, there is still some chance for the central bank to tweak the yield curve control parameters, by allowing the yield of 10-year JGB to “fluctuate more than +/- 0.25%”. Or, a less likely change is to target yield with shorter maturity than 10 years. So, there is still some scope of post meeting volatility.

On the data front, GDP from the US, Eurozone and Canada will be mostly watched. US will also release durable goods orders, consumer confidence, and personal income and spending. Germany Ifo business climate and Eurozone CPI flash will be watched. Australia CPI is also important as that could set the stage for a June RBA rate hike, or even earlier.

Here are some highlights for the week:

- Monday: Japan corporate services prices; Germany Ifo business climate.

- Tuesday: Japan unemployment rate; Swiss Trade balance; UK public sector net borrowing; US durable goods orders, house price index, consumer confidence, new home sales.

- Wednesday: Australia CPI; Germany Gfk consumer climate; US goods trade balance, pending homes.

- Thursday: New Zealand trade balance; BoJ rate decision, Japan industrial production, retail sales, housing starts; Germany CPI flash; ECB monthly bulletin; US GDP, jobless claims.

- Friday: Australia PPI, private sector credit; Swiss retail sales, KOF economic barometer; France GDP; Germany GDP; Eurozone M3 money supply, GDP, CPI flash; Canada GDP; US personal income and spending, Chicago PMI.

AUD/USD Daily Report

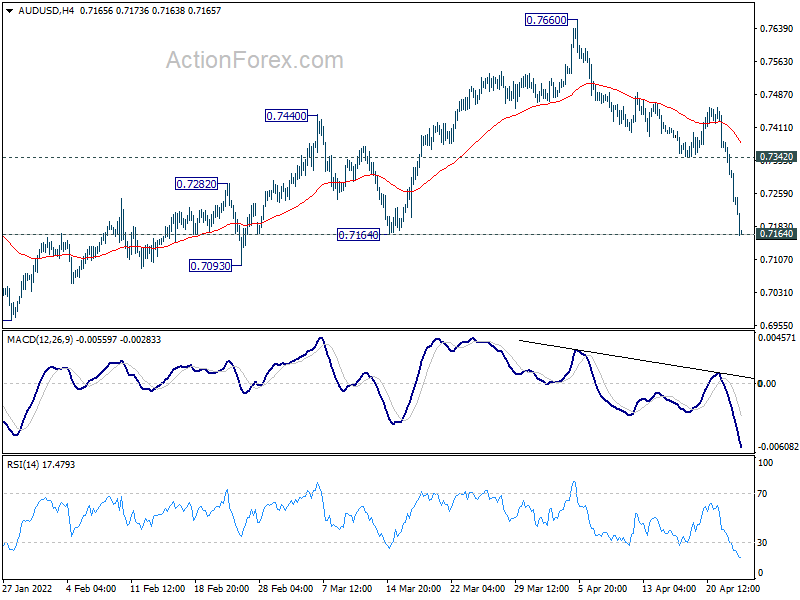

Daily Pivots: (S1) 0.7193; (P) 0.7286; (R1) 0.7338; More…

Intraday bias in AUD/USD remains on the downside with focus on 0.7164 support. Decisive break there will confirm that whole rebound from 0.6966 has completed at 0.7660. More importantly, such development will suggest that larger correction from 0.8006 has already started the third leg. Deeper decline would be seen back to retest 0.6966 low next. On the upside, break of 0.7342 support turned resistance is needed to indicate short term bottoming. Otherwise, further decline will remain in favor even in case of recovery.

{kind=link}

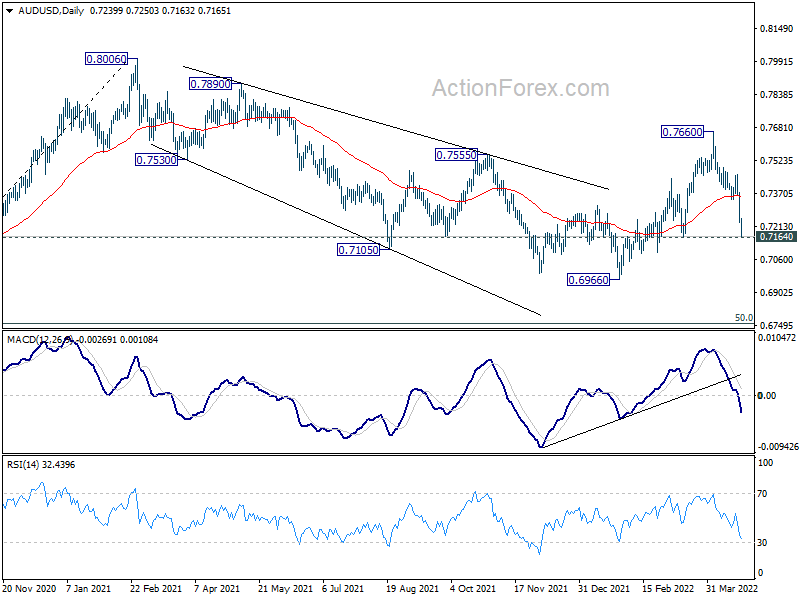

In the bigger picture, price actions from 0.8006 are seen as a corrective pattern to rise from 0.5506 (2020 low). Break of 0.7164 will suggest that such correction is still in progress, with fall from 0.7660 as the third leg. Next target will be 50% retracement of 0.5506 to 0.8006 at 0.6756. On the upside, break of 0.7660 will revive that case that the correction has already completed at 0.6966.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Mar | 1.30% | 1.20% | 1.10% | |

| 08:00 | EUR | Germany IFO Business Climate Apr | 88.1 | 90.8 | ||

| 08:00 | EUR | Germany IFO Current Assessment Apr | 95 | 97 | ||

| 08:00 | EUR | Germany IFO Expectations Apr | 82.3 | 85.1 |