Aussie Stabilizing after Strong CPI, Yen and Dollar Strong on Risk Aversion

Yen and Dollar are both staying in the driving seat as risk-off sentiment continues to dominate the markets. Sterling remains the worst performing one, followed by Euro, with selling focus mainly on them. Australian Dollar recovers mildly as stronger than expected CPI data prompted some speculations that RBA could hike next week. But it’s not too far away from Euro and Sterling in terms of weakness.

Technically, Gold is currently still struggling around 1900 handle but looks rather vulnerable. The fall from 1988.23 is seen as the third leg of the pattern from 2070.06. Deeper decline is expected as long as 1920.97 minor resistance holds. Break of 1889.79 will target 100% projection of 2070.06 to 1889.79 from 1998.23 at 1817.98. The move could be accompanied by another wave broad based buying in Dollar.

{kind=link}

In Asia, at the time of writing, Nikkei is down -1.38%. Hong Kong HSI is up 0.09%. China Shanghai SSE is up 0.38%. Singapore Strait Times is down -0.09%. Japan 10-year JGB yield is down -0.0013 at 0.246. Overnight, DOW dropped -2.38%. S&P 500 dropped -2.81%. NASDAQ dropped -3.95%. 10-year yield dropped -0.054 to 2.772.

NASDAQ hits new low as medium term correction resumes

NASDAQ lost -3.95%% overnight and closed at a new 2022 low. The development suggests that whole corrective fall from 16212.22 is resuming. More importantly, a key medium term fibonacci support at 38.2% retracement of 6631.41 to 16212.22 at 12552.35 is taken out. If this fibonacci support cannot be reclaimed soon, the decline ahead could be rather deep.

Tentatively, NASDAQ should target 100% projection of 16212.22 to 12587.88 from 14646.90 at 11022.56 next. There should be strong support around this level, and above 61.8% retracement of 6631.42 to 16212.22 at 10291.28 to contain downside to finish the correction.

Australia CPI accelerated to 2.1% qoq, 5.1% yoy, highest since 2000

Australia CPI rose 2.1% qoq in Q1, accelerated from Q3’s 1.3% qoq, above expectation of 1.7% qoq. For the 12-month period, CPI accelerated to 5.1% yoy, up from 3.5% yoy, above expectation of 4.6% yoy. RBA trimmed mean CPI also accelerated from 2.6% yoy to 3.7% yoy, above expectation of 3.4% yoy.

Head of Prices Statistics at the ABS, Michelle Marquardt, said “The CPI recorded its largest quarterly and annual rises since the introduction of the goods and services tax (GST) (in 2000)”

“Strong demand combined with material and labour supply disruptions throughout the year resulted in the highest annual inflation for new dwellings since the introduction of the GST. Annual price inflation for automotive fuel was the highest since the 1990 Iraqi invasion of Kuwait.”

Marquardt said: “Annual trimmed mean inflation was the highest since 2009. This reflected the broad-based nature of price rises, as the impacts of supply disruptions, rising shipping costs and other global and domestic inflationary factors flowed through the economy.”

Looking ahead

Germany Gfk consumer sentiment and Swiss Credit Suisse economic expectations will be featured in European session. Later in the day, US will release goods trade balance and pending home sales.

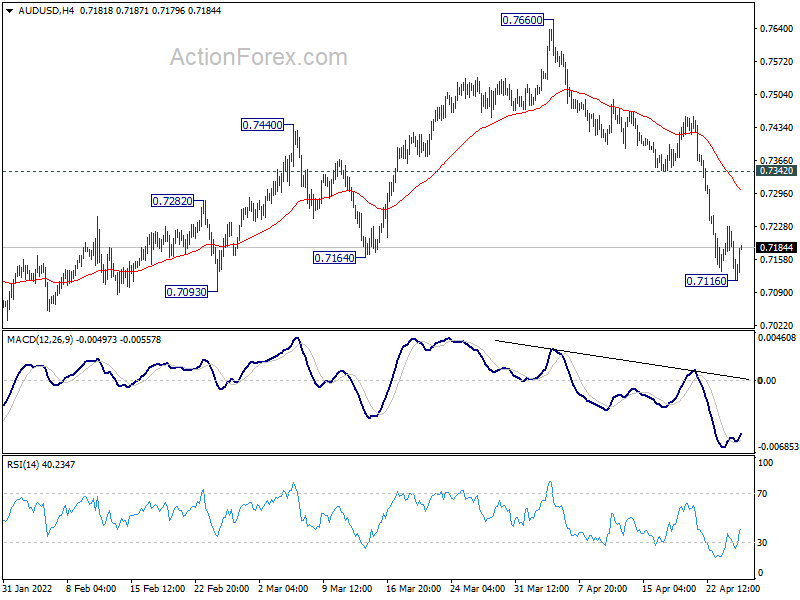

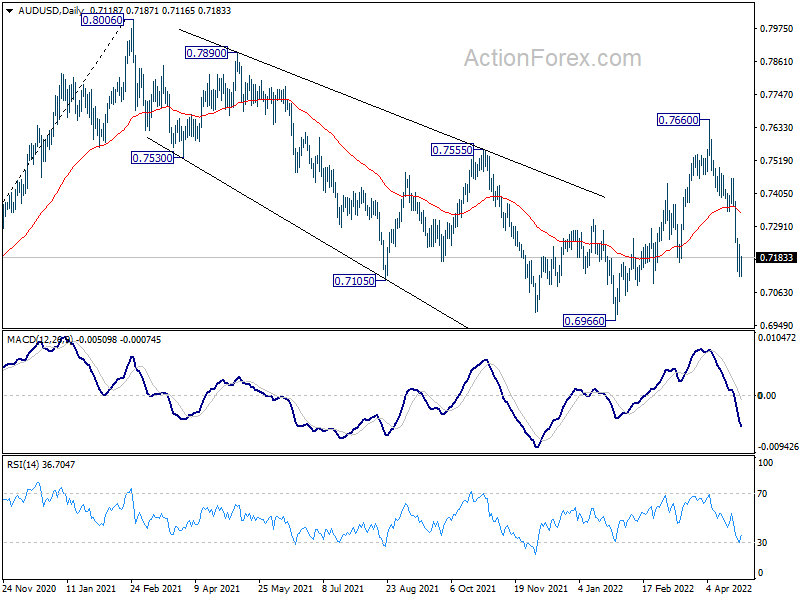

AUD/USD Daily Report

Daily Pivots: (S1) 0.7086; (P) 0.7157; (R1) 0.7196; More…

A temporary low is formed at 0.7116 in AUD/USD and intraday bias is turned neutral first. But near term outlook will remain cautiously bearish with 0.7342 support turned resistance intact. Current development argues that larger correction from 0.8006 is in its third leg. Below 0.7116 will target a retest on 0.6966 low first.

{kind=link}

In the bigger picture, price actions from 0.8006 are seen as a corrective pattern to rise from 0.5506 (2020 low). Break of 0.7164 will suggest that such correction is still in progress, with fall from 0.7660 as the third leg. Next target will be 50% retracement of 0.5506 to 0.8006 at 0.6756. On the upside, break of 0.7660 will revive that case that the correction has already completed at 0.6966.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | CPI Q/Q Q1 | 2.10% | 1.70% | 1.30% | |

| 01:30 | AUD | CPI Y/Y Q1 | 5.10% | 4.60% | 3.50% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q1 | 1.40% | 1.20% | 1.00% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q1 | 3.70% | 3.40% | 2.60% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence May | -15.7 | -15.5 | ||

| 08:00 | CHF | Credit Suisse Economic Expectations Apr | -27.8 | |||

| 12:30 | USD | Goods Trade Balance (USD) Mar P | -105.0B | -106.6B | ||

| 12:30 | USD | Wholesale Inventories Mar P | 2.30% | 2.50% | ||

| 14:00 | USD | Pending Home Sales M/M Mar | -1.00% | -4.10% | ||

| 14:30 | USD | Crude Oil Inventories | 0.1M | -8.0M |