Traders Still Betting on 75bps Hike by Fed in June, Dollar Rally Capped

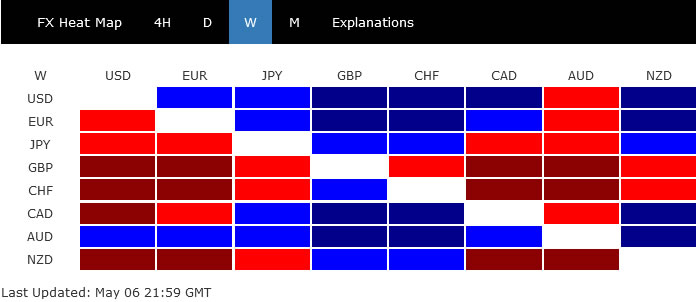

While RBA, Fed and BoE announced rate hikes last week, the impacts and reactions were rather delivered. RBA’s larger than expected hike was well received and helped Aussie secured the first place, even though it pared back much gains on risk-aversion. On the other hand, BoE’s announcement was considered dovish, with warning of recession, and hammered the Pound broadly lower as the worst performer. .

Reaction to Fed was mixed and volatile. But in the end, markets seemed to be still buying in the prospect of a 75bps hike next, as seen in the late selloff in stocks. Dollar followed sterling as the second strongest. But it’s strength against Euro was capped by hawkish ECB comments. The greenback’s rally against Yen was also capped by risk-off sentiment.

{kind=link}

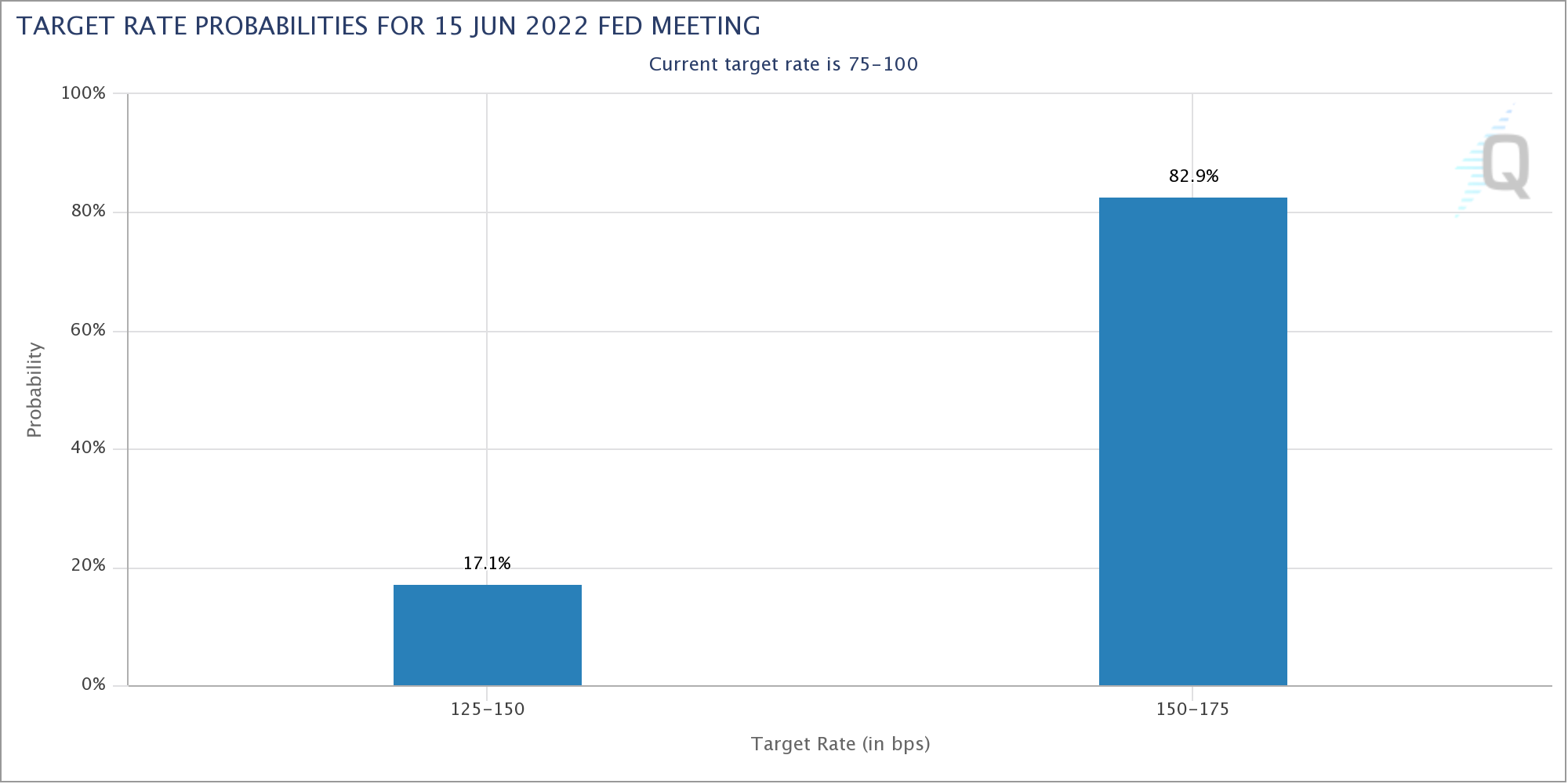

Markets still pricing in 82.9% chance of a 75bps hike at June FOMC meeting

Fed delivered the 50bps hikes as widely expected and raised federal funds rate target to 0.75-1.00%. Chair Jerome Powell shocked the markets by saying that “a 75 basis point increase is not something that the committee is actively considering,” in the post meeting press conference. Such comments triggered quick adjustment in market expectations and pushed stocks higher.

Yet, investors were quick in readjusting their expectations and markets pricings which sent stocks and bonds lower again. At the end of the week, fed fund futures are still pricing in 82.9% chance of a 75bps hike in at the June 15 FOMC meeting, to 1.50-75%. Traders will continue to tune their bets based on upcoming data like this week’s CPI, and comments from other Fed officials.

{kind=link}

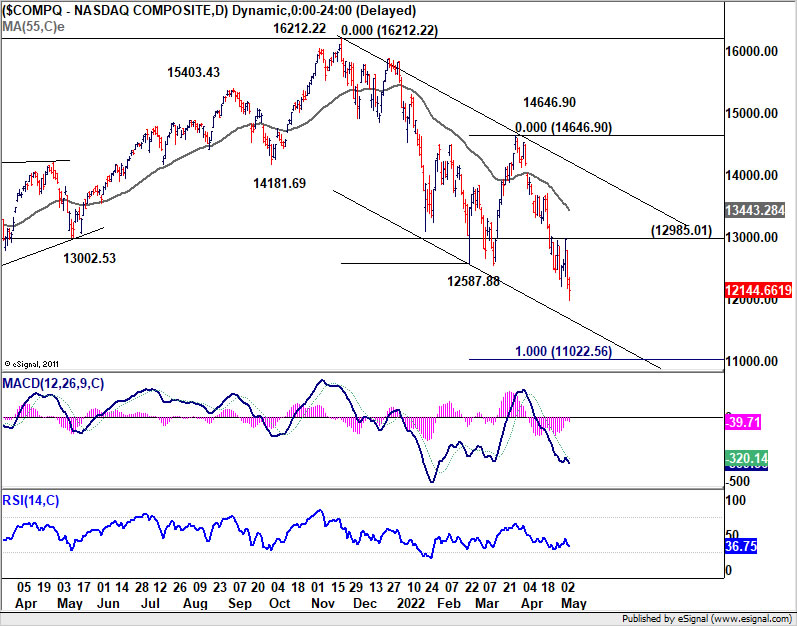

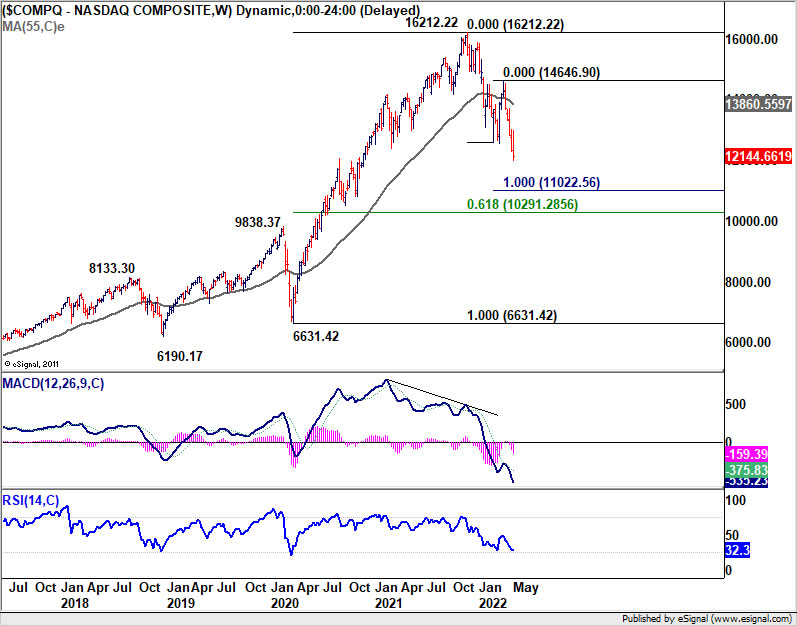

NASDAQ extended correction after brief recovery

The intra-week rebound provided false hope to stock investors. NASDAQ extended the correction from 16212.22 and closed lower at 12144.66. Near term outlook stays bearish as long as 12985.01 resistance holds. Next target is 100% projection of 16212.22 to 12587.88 from 14646.90 at 11022.56.

Still, strong support is expected around this 11022.56 level, and above 61.8% retracement of 6631.42 to 16212.22 at 10291.28 to contain downside to finish the correction.

{kind=link}

{kind=link}

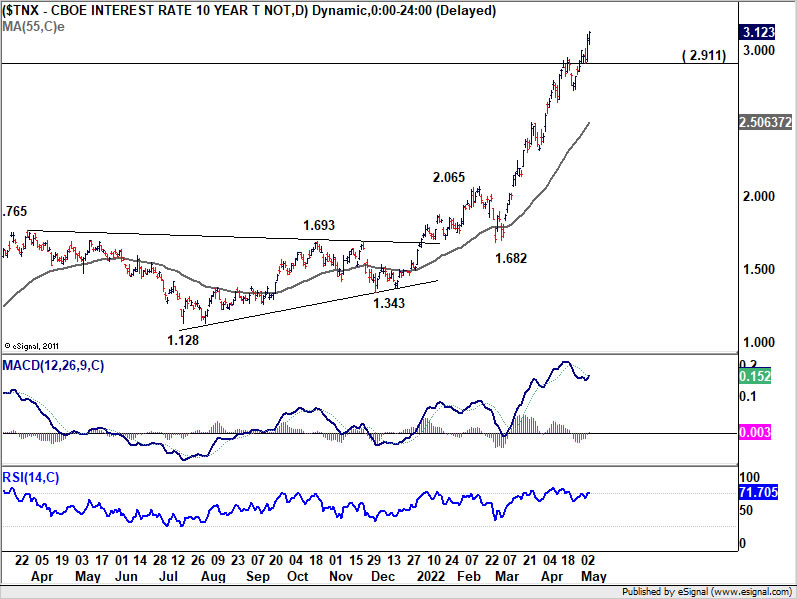

10-year yield extended up trend, closing in 3.248 key resistance

US 10-year yield continued its up trend last week and closed well above 3% handle at 3.123. Next target is 3.248 long term resistance level (2018 high). We’d stay cautious on strong resistance from there the break pull back. Break of 2.911 support level will indicate short term topping and turn into a correction phase. Nevertheless, firm break of 3.248 will target 161.8% projection of 0.398 to 1.765 from 1.343 at 3.554 next.

It should be emphasized again that sustained break of 3.248 will finally break the lower-high-lower-low pattern that started back in 1981. If could confirm the start of an era of higher yields in the long term.

{kind=link}

{kind=link}

{kind=link}

Dollar index struggled to extend gain above 2017 high

Dollar index also breached a key resistance at 103.82 (2017 high), but struggled to extend gains above there. That was a result of both resilience in Euro and Yen. Euro was firstly talked up by comments from ECB hawks. Secondly, it’s lifted by buying against the weak Sterling. Thirdly, German 10-year bund yield also closed above 1% handle for the first time since 2015, closing at 1.135. On the other hand, risk aversion is providing some support to Yen.

For now, further rise is still expected in DXY as long as 102.35 support holds. Firm break of 103.82 will resume long term up trend from 70.69 (2008 low). Next medium term target is 61.8% projection of 72.69 to 103.82 from 89.20 at 108.43. However, break of 102.35 should bring near term correction first.

{kind=link}

{kind=link}

{kind=link}

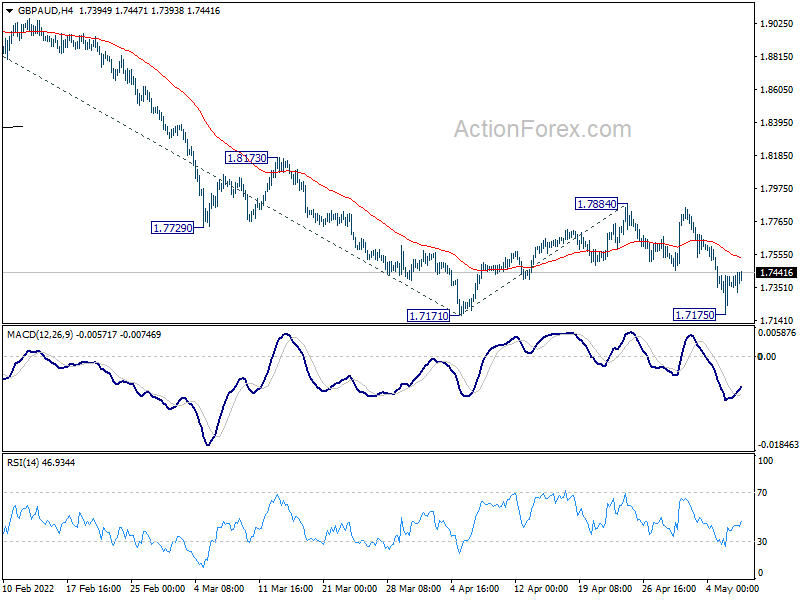

GBP/AUD the worst performer, but defended 1.7171 support

Sterling ended as the worst performing one even though BoE delivered the fourth 25bps rate hike as expected. The surprise was found in BoE’s warning of a very “sharp slowdown” in growth ahead, even with risks of recession. On the other hand, Aussie ended as the stronger, after RBA delivered a larger than expected hike of 25bps to 0.35%. That set the stage of a possible 40bps hike to 0.75% in June.

GBP/AUD, thus, ended as the biggest mover, down -2.10% for the week. However, after initial decline, it quickly recovered after just missing 1.7171 low by an inch. While outlook stays bearish with 1.7844 resistance intact, the development suggests that downside break out would only come at a slightly later stage. When that happens, next target is 61.8% projection of 1.9218 to 1.7171 from 1.7884 at 1.6619.

{kind=link}

{kind=link}

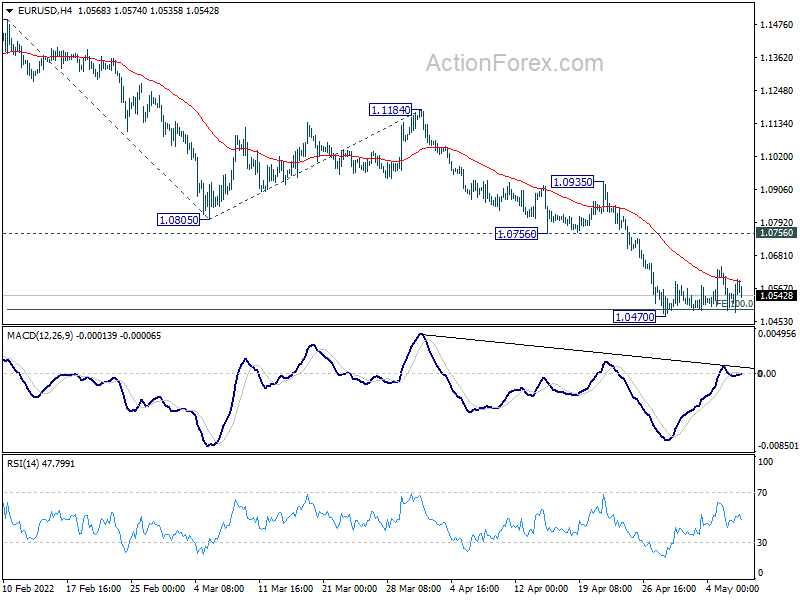

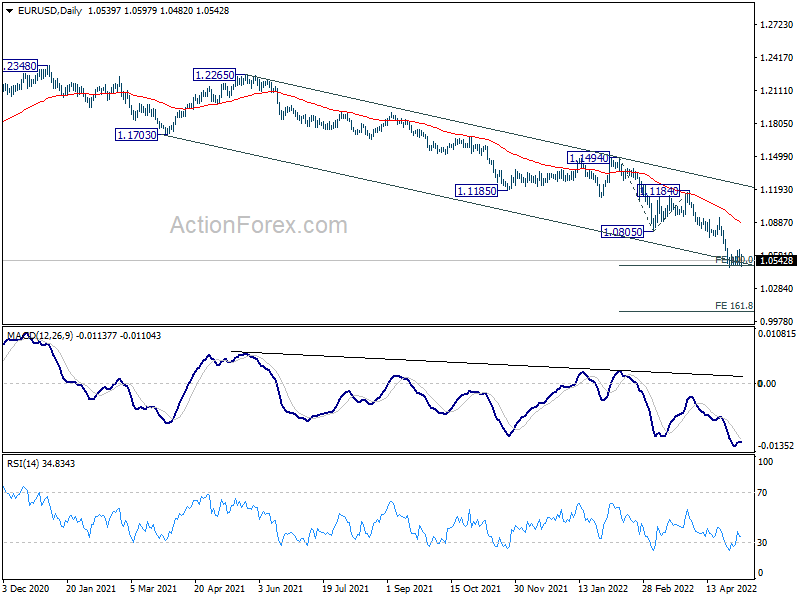

EUR/USD Weekly Outlook

EUR/USD stayed in consolidation above 1.0470 last week and outlook is unchanged. Initial bias remains neutral this week first. In case of another recovery, upside should be limited by 1.0756 support turned resistance to bring fall resumption. On the downside, firm break of 1.0470 will resume larger down trend to 161.8% projection of 1.1494 to 1.0805 from 1.1184 at 1.0069.

{kind=link}

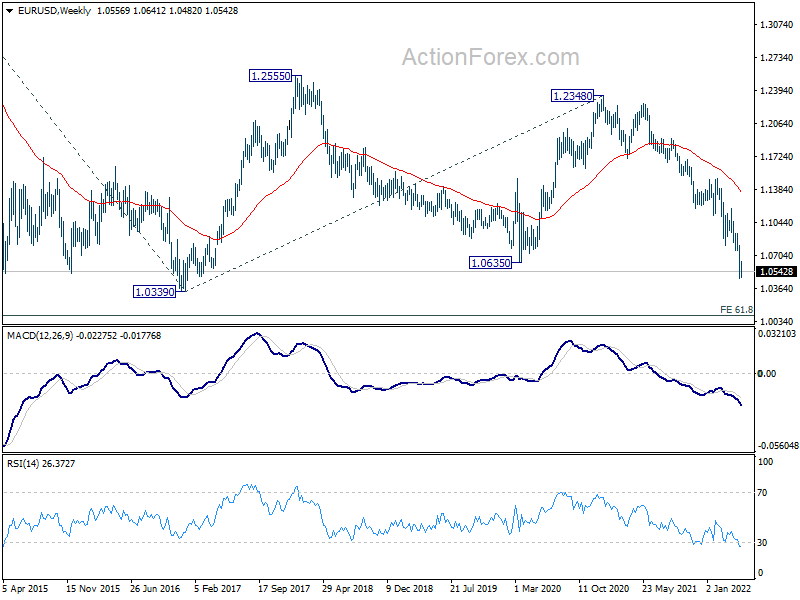

In the bigger picture, the decline from 1.2348 (2021 high) is expected to continue as long as 1.1185 support turned resistance holds. The break of 1.0635 (2020 low) now raises the chance that it’s resuming long term down trend from 1.6039 (2008 high). Retest of 1.0339 (2017 low) low should be seen next. Decisive break there will confirm this bearish case.

{kind=link}

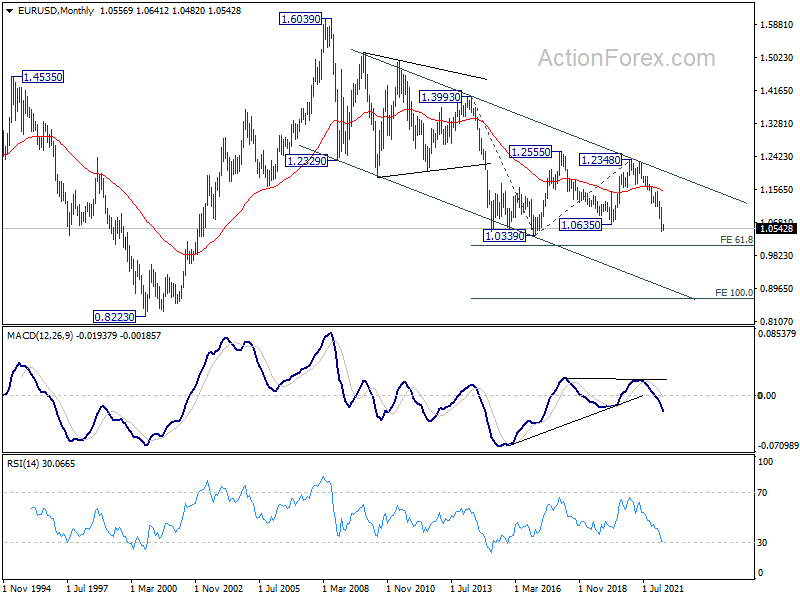

In the long term picture, current development suggests that long term down trend from 1.6039 (2008 high) is ready to resume. Break of 1.0339 will target 61.8% projection of 1.3993 to 1.0339 from 1.2348 at 1.0090. Decisive break there could bring downside acceleration towards 100% projection at 0.8694.

{kind=link}

{kind=link}