Markets Tread Water ahead of US CPI, Gold and Yields Dip

The forex markets are stuck in very tight range in Asia session today, as traders are awaiting another set of consumer inflation data from the US. For now, Dollar, Euro and Yen are the stronger ones for the week, and they’re range bound against each other. Commodity currencies remain the worst performers, as led by Aussie. Sterling and Swiss Franc are mixed, with the Pound having an upper hand.

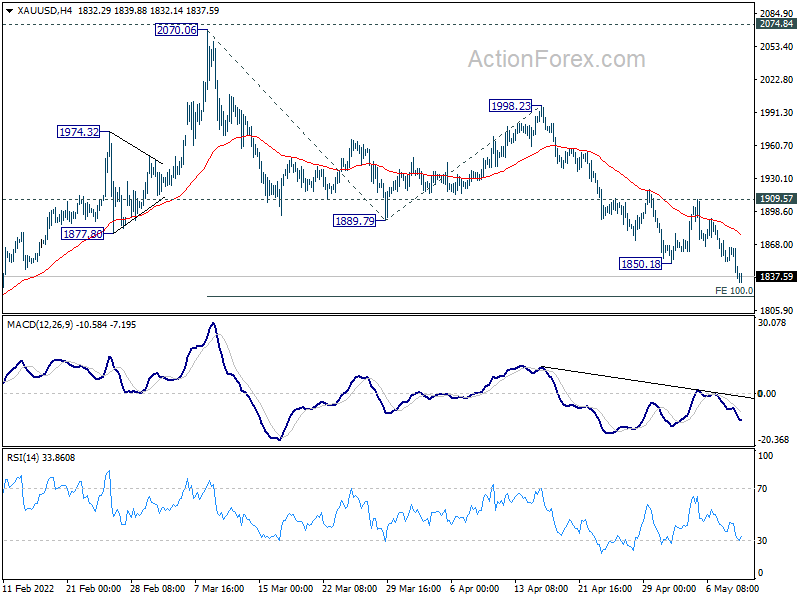

Technically, main focuses remain on range breakout in EUR/USD and USD/JPY. As for EUR/USD, the levels are 1.0470 support and 1.0641 resistance. For USD/JPY, the levels are 128.61 support and 131.34 resistance. Gold extended recent decline through 1850.18 support overnight. That gives Dollar upside breakout a slight advantage. But that’s countered by 10-year yield’s fall below 3% level.

In Asia, at the time of writing, Nikkei is up 0.14%. Hong Kong HSI is up 1.72%. China Shanghai SSE is up 1.63%. Singapore Strait Times is down -0.58%. Japan 10-year JGB yield is up 0.0035 at 0.251. Overnight, DOW dropped -0.26%. S&P 500 rose 0.25%. NASDAQ rose 0.98%. 10-year yield dropped -0.086 to 2.993, back below 3% handle.

Fed Waller: Front-load it, get it done

Fed Governor Christopher Waller said yesterday, “It’s time to raise rates now when the economy can take it. Front-load it, get it done, and then we can judge how the economy is proceeding later, and if we have to do more, we’re going to do more.”

“The labor market is strong. The economy is doing so well,” he said. “This is the time to hit it if you think there’s going to be any kind of negative reaction, because the economy can take it.”

Fed Mester: Do more upfront rather than waiting

Cleveland Fed President Loretta Mester told Reuters, “I would need to see monthly numbers coming down in a compelling way before I would want to conclude we could now rest” on raising interest rates.

“The risks to inflation are skewed to the upside and the cost of allowing that inflation to continue is high,” she said, an argument for the Fed “doing more upfront rather than waiting.”

“I don’t think it (inflation) will get back to 2% next year. But it will be well on its way, in the range of two and half percent but moving in the right direction,” she said. “And given where the economy is and all the factors affecting inflation that are outside of our realm, that is acceptable to me.”

Australia Westpac consumer sentiment dropped to 90.4 in May, lowest since Aug 2020

Australia Westpac-MI consumer sentiment index dropped from 95.8 to 90.4 in May. That’s the lowest level since August 2020. The reading was also -8.4% below the average seen in 2019. The -5.6% decline was the largest since the -6.9% fall in June 2016.

Looking at some details, family finances for the next 12 months dropped from 105.1 to 93.3. Economic conditions for the next 12 months dropped from 95.9 to 90.4. Unemployment expectations rose from 99.2 to 109.6.

Westpac said two “stunning developments are clearly unnerving consumers”. Firstly, headline inflation surged above 5% for the first time since 2007. Secondly, RBA raised interest rate for the first time since 2010.

Regarding RBA policies, Westpac said “having now begun its tightening cycle the Board is almost certain to follow up the move in May with a further move in June”. It added, “the need to avoid an over-shoot later in the cycle is why, despite this disturbing tumble in Consumer Sentiment, we believe the prudent approach in June would be to lift rates by 40bps rather than the 25 bps that is currently favoured by most analysts.

Gold extending decline towards 1817

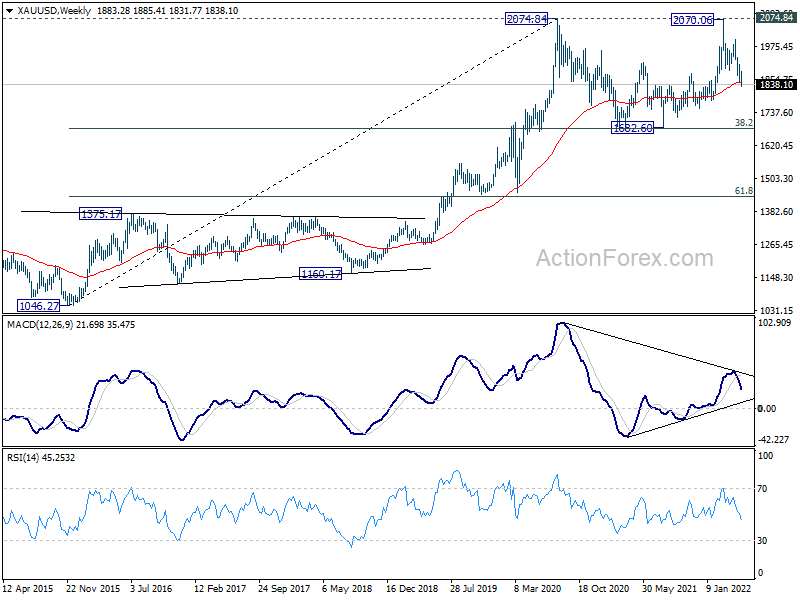

Gold’s near term decline resumed overnight and broke through 1850.18 support. Near term outlook now stays bearish as long as 1909.57 resistance holds. Next target is 100% projection of 2070.06 to 1889.79 from 1998.23 at 1817.86. The whole fall from 2070.06 is seen as the third leg of the consolidation pattern from 2074.84 (2020 high). Firm break of 1817.86 could prompt more downside acceleration towards 1682.60 to finally finish the pattern.

{kind=link}

{kind=link}

Looking ahead

Germany CPI final will be released in European session. But main focus will be on US April CPI.

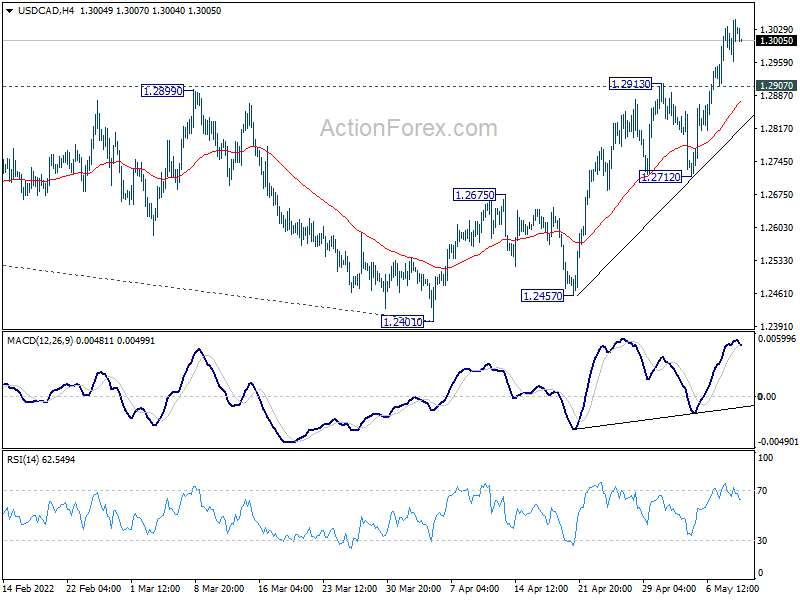

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2976; (P) 1.3014; (R1) 1.3067; More…

Intraday bias in USD/CAD stays on the upside for now, despite some loss in upside momentum. Current Sustained break of 1.3022 fibonacci level will carry larger bullish implications. Next target will be 100% projection of 1.2005 to 1.2947 from 1.2401 at 1.3343. On the downside, below 1.2907 minor support will turn intraday bias neutral first. But further rally will remain in favor as long as 1.2712 support holds.

{kind=link}

In the bigger picture, focus stays on 38.2% retracement of 1.4667 (2020 high) to 1.2005 (2021 low) at 1.3022. Sustained break there should confirm that the down trend from 1.4667 has completed after defending 1.2061 long term cluster support. Further rise would then be seen towards 61.8% retracement at 1.3650. However, rejection by 1.3022 will maintain medium term bearishness. Break of 1.2005 will resume the down trend from 1.4667 and that carries larger bearish implications too.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence May | -5.60% | -0.90% | ||

| 01:30 | CNY | CPI Y/Y Apr | 2.10% | 1.90% | 1.50% | |

| 01:30 | CNY | PPI Y/Y Apr | 8.00% | 7.80% | 8.30% | |

| 05:00 | JPY | Leading Economic Index Mar P | 101.0 | 100.4 | 100 | |

| 06:00 | EUR | Germany CPI M/M Apr F | 0.80% | 0.80% | ||

| 06:00 | EUR | Germany CPI Y/Y Apr F | 7.40% | 7.40% | ||

| 12:30 | USD | CPI M/M Apr | 0.20% | 1.20% | ||

| 12:30 | USD | CPI Y/Y Apr | 8.10% | 8.50% | ||

| 12:30 | USD | CPI Core M/M Apr | 0.40% | 0.30% | ||

| 12:30 | USD | CPI Core Y/Y Apr | 6.00% | 6.50% | ||

| 14:30 | USD | Crude Oil Inventories | -1.0M | 1.3M |