EUR/USD Downside Breakout, Yen in Upside Acceleration

Yen is the runaway winner today on massive safe-haven flows, which also pushed up treasury bonds. Meltdown in cryptocurrencies intensified further, as bitcoin barely holds on to 25k. Major European indexes are in deep red while US futures, in particular NASDAQ, are pointing to lower open. Benchmark treasury yields extend pull back, as US 10-year yield is back at 2.83 while Germany 10-yearly yield is back at 0.85.

Back in the currency markets, Dollar is following Yen as the second strongest. Aussie is the worst performing so far. But Euro’s selloff is worth more of a mention, despite hawkish comments from ECB officials. The weakness in Euro is somewhat amplified by the selloff against Sterling and Swiss Franc.

Technically, AUD/JPY’s fall from 95.73 extends to as low as 87.94 so far today. The break of near term falling channel support suggests downside acceleration. The break of 100% projection of 95.73 to 90.41 from 94.00 at 88.68 also raises the chance that 95.73 is already a medium term top. Next line of defense is in 86.24 resistance turned support. Firm break there will argue that it’s already correcting the whole up trend from 2020 low at 59.85 already. Such development, if happens, could be reflected in global stocks and even bond markets too.

{kind=link}

In Europe, at the time of writing, FTSE is down -2.12%. DAX is down -2.30%. CAC is down -2.56%. Germany 10-year yield is down -0.131 at 0.860. Earlier in Asia, Nikkei dropped -1.77%. Hong Kong HSI dropped -2.24%. China Shanghai SSE dropped -0.12%. Singapore Strait Times dropped -1.89%. Japan 10-yaer JGB yield rose 0.0026 to 0.251.

US PPI up 0.5% mom, 11.0% yoy in Apr, above expectations

US PPI for final demand rose 0.5% mom in April, matched expectations. PPI final demand for goods rose 1.3% mom, for construction dropped -4.0%, while for services was unchanged. For the 12-month period, PPI rose 11.0% yoy, down from 11.2% yoy, above expectation of 10.7% yoy.

PPI less foods, energy, and trade services rose 0.6% mom. For the 12-month period, PPI for less foods, energy, and trade services rose 6.9% yoy.

US initial jobless claims rose to 203k, continuing claims dropped to 1.343m

US initial jobless claims rose 1k to 203k in the week ending May 7, above expectation of 190k. Four-week moving average of initial claims rose 4k to 193k.

Continuing claims dropped -44k to 1343k in the week ending April 30, lowest since January 3, 1970 when it was 1332k. Four-week moving average of initial claims dropped -33k to 1385k, lowest since January 31, 1970 when it was 1374k.

ECB Makhlouf: The era of negative rates is reaching its conclusion

ECB Governing Council member Gabriel Makhlouf said today, ECB has reached the point “act”. And, “the balance of advantage has tilted decisively towards the need for further action, albeit not necessarily at a similar pace to that of other central banks”.

“Our objective is for inflation to be at 2% over the medium term – levels are significantly above that now, and it is time for the Council to move to end net asset purchases under the asset purchase programme next month or in July,” he said.

Makhlouf added, it’s “realistic to expect that the first move in the ECB’s interest rates will happen soon after net asset purchases end and that rates are likely to be in positive territory by early next year.” But he didn’t specify when the rate hike would occurs.

“The era of negative rates is reaching its conclusion,” he said.

BoE Ramsden: I don’t think we’ve gone far enough yet on bank rate

BoE Deputy Governor Governor Dave Ramsden told Bloomberg that stronger than expected job market could push inflation further higher from current 7% to 10% before year end. “Given what we know about the UK labor market, I wouldn’t be surprised if it turned out to be a bit tighter,” he said. “I think there are upside risks on inflation the medium term.”

“Certainly on the basis of my current assessment of prospects, we’re not there yet in terms of how far monetary policy has to tighten,” he said. “I’m still very, very supportive of the forward guidance that there may well need to be further tightening in the coming months.”

June “will be a chance to take stock — in this extraordinary period we really are learning things everyday,” he said. “I don’t think we’ve gone far enough yet on bank rate, but I do think that what we’ve already done is having an impact.”

UK GDP contracted -0.1% mom in Mar, up 0.8% qoq in Q1

UK GDP contracted -0.1% mom in March, worse than expectation of 0.1% mom growth. That came after no growth in February (revised down from 0.1%). For the month, services dropped -0.2%. Production dropped -0.2%. Construction grew 1.7%. Monthly GDP is still 1.2% above pre-coronavirus levels, with services 1.5% above, construction 3.7% above and production -1.6% below.

For Q1, GDP grew 0.8% qoq, below expectation of 1.0% qoq. Services rose 0.4% qoq. Production rose 1.2% qoq. Construction rose 3.8% qoq. Quarterly GDP was 0.7% above pre-coronavirus level.

Also released, manufacturing production came in at -0.2% mom, 1.9% yoy in March, versus expectation of 0.0% mom, 2.3% yoy. Industrial production was at -0.2% mom, 0.7% yoy, versus expectation of 0.1% mom, 0.4% yoy. Goods trade deficit widened to GBP -23.9B, versus expectation of GBP -18.5B.

BoJ: Necessary to continue with current powerful monetary easing

In the Summary of Opinions of the April 27-28 meeting, BoJ noted that “as Japan is a commodity importer, the rise in commodity prices leads to an outflow of income from Japan and thus exerts downward pressure on the economy.” And, “it is necessary for the Bank to continue with the current powerful monetary easing and thereby firmly support the economy”

One opinion noted that “one reason for the yen’s recent depreciation is that economic conditions in Japan have been different from those in the United States and Europe, and it is not appropriate that the Bank change its policy with the aim of controlling foreign exchange rates.”

“With a view to clarifying the Bank’s stance to date of not accepting the long-term interest rate exceeding 0.25 percent and to avoiding a situation where daily operations are unnecessarily factored in by the market, it is appropriate for the Bank to announce in advance that it will conduct fixed-rate purchase operations at 0.25 percent every business day, unless it is highly likely that no bids will be submitted.”

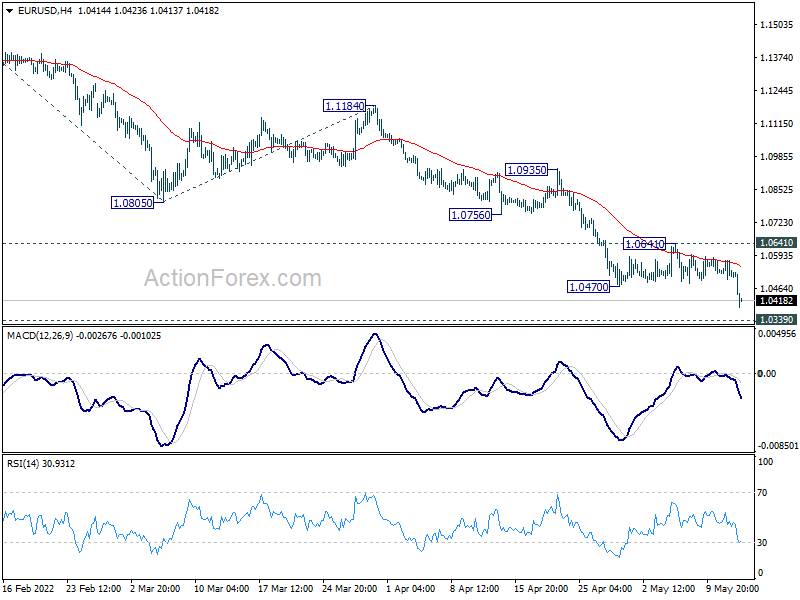

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0485; (P) 1.0531 (R1) 1.0560; More…

EUR/USD finally breaks through 1.0470 support today as larger down trend resumes. Intraday bias is back on the downside with focus on 1.0339 long term support. Firm break there will carry larger bearish implication and target 161.8% projection of 1.1494 to 1.0805 from 1.1184 at 1.0069. On the upside, break of 1.0641 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

{kind=link}

In the bigger picture, break of medium term channel support suggests downside acceleration. Current decline from 1.2348 (2021 high) is probably resuming long term down trend from 1.6039 (2008 high). Retest of 1.0339 (2017 low) low should be seen next. Decisive break there will confirm this bearish case. This will now remain the favored case as long as 1.0805 support turned resistance holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS Housing Price Balance Apr | 80% | 71% | 74% | |

| 23:50 | JPY | Bank Lending Y/Y Apr | 0.90% | 0.40% | 0.50% | |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 23:50 | JPY | Current Account (JPY) Mar | 1.56T | 0.63T | 0.52T | |

| 01:00 | AUD | Consumer Inflation Expectations May | 5.00% | 5.20% | ||

| 03:00 | NZD | RBNZ Inflation Expectations Q/Q Q2 | 3.29% | 3.27% | ||

| 05:00 | JPY | Eco Watchers Survey: Current Apr | 51.3 | 47.8 | ||

| 06:00 | GBP | GDP M/M Mar | -0.10% | 0.10% | 0.10% | 0.00% |

| 06:00 | GBP | GDP Q/Q Q1 P | 0.80% | 1.00% | 1.30% | |

| 06:00 | GBP | Manufacturing Production M/M Mar | -0.20% | 0.00% | -0.40% | -0.60% |

| 06:00 | GBP | Manufacturing Production Y/Y Mar | 1.90% | 2.30% | 3.60% | 3.50% |

| 06:00 | GBP | Industrial Production M/M Mar | -0.20% | 0.10% | -0.60% | -0.30% |

| 06:00 | GBP | Industrial Production Y/Y Mar | 0.70% | 0.40% | 1.60% | 2.10% |

| 06:00 | GBP | Index of Services 3M/3M Mar | 0.40% | 0.90% | 0.80% | |

| 06:00 | GBP | Goods Trade Balance (GBP) Mar | -23.9B | -18.5B | -20.6B | |

| 06:30 | CHF | Producer and Import Prices M/M Apr | 1.30% | 0.90% | 0.80% | |

| 06:30 | CHF | Producer and Import Prices Y/Y Apr | 6.70% | 5.80% | 6.10% | |

| 11:31 | GBP | NIESR GDP Estimate (3M) Apr | 0.30% | 1.00% | 0.80% | |

| 12:30 | USD | PPI M/M Apr | 0.50% | 0.50% | 1.40% | 1.60% |

| 12:30 | USD | PPI Y/Y Apr | 11.00% | 10.70% | 11.20% | |

| 12:30 | USD | PPI Core M/M Apr | 0.40% | 0.60% | 1.00% | 1.20% |

| 12:30 | USD | PPI Core Y/Y Apr | 8.80% | 8.90% | 9.20% | |

| 12:30 | USD | Initial Jobless Claims (May 6) | 203K | 190K | 200K | 202K |

| 14:30 | USD | Natural Gas Storage | 82B | 77B |