Dollar Recovers in Tight Range, Sterling Down after CPI

Dollar and Yen are recovering mildly today but overall major pairs and crosses are stuck in very tight range. European majors are the weaker ones, with Sterling having a lower handle. Commodity currencies are mixed. Trading is also quiet in other markets with Gold continuing to hover slightly above 1800 handle. WTI crude oil is gyrating in tight range below 115. Bitcoin is flip-flopping around 30k. A surprise could be found in US 10-year yield ahead, which might reclaim 3% handle. That could help give Dollar a lift against Yen.

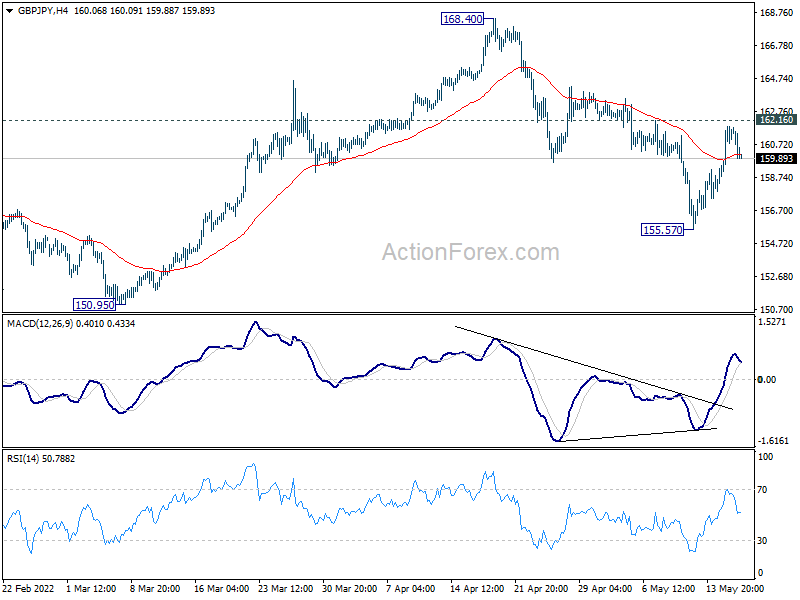

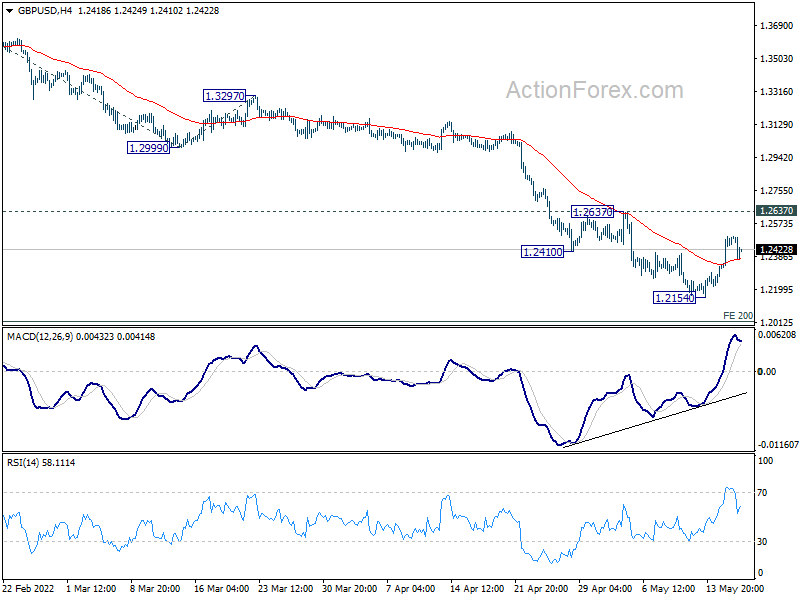

Technically, it looks like Sterling has already failed near term resistance level, after today’s CPI data provided no fuel for further rally. GBP/USD retreated well ahead of 1.2637 resistance, and GBP/JPY ahead of 161.16 minor resistance. EUR/GBP also recovered ahead of 0.8365 support. There is slightly more prospect of more downside in the pound.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.47%. DAX is down -0.50%. CAC is down -0.51%. Germany 10-year yield is up 0.0235 at 1.076. Earlier in Asia, Nikkei rose 0.94%. Hong Kong HSI rose 0.20%. China Shanghai SSE dropped -0.25%. Singapore Strait Times rose 0.73%. Japan 10-year JGB yield rose 0.0016 to 0.246.

Canada CPI ticked up to 6.8% yoy in Apr, driven by food and shelter prices

Canada CPI ticked up further to 6.8% yoy in April, up from March’s 6.7% yoy, above expectation of 6.7% yoy. CPI ex-gasoline accelerated to 5.8%, up from 5.5% yoy, fastest since the series was introduced in 1999. Statics Canada added that the year-over-year increase in April was largely driven by food and shelter prices. Gas prices increased at a slower pace.

Looking at the preferred measures of core inflation by BoC, CPI common rose from 3.0% yoy to 3.2% yoy, above expectation of 2.9% yoy. CPI median rose from 4.0% yoy to 4.4% yoy, above expectation of 3.9% yoy. CPI trimmed rose from 4.8% yoy to 5.1% yoy, above expectation of 4.7% yoy.

ECB de Cos: Further rate hikes could be made in coming quarters

ECB Governing Council member Pablo Hernandez de Cos said today, “in the coming quarters, further (rate) increases could be made to reach levels in line with the natural rate of interest if the medium-term inflation outlook remains around our target.”

But de Cos also emphasized that the process of policy normalization would be gradual. “For this gradual approach to be adopted, it is essential that inflation expectations remain anchored and that no second-round and indirect effects of a magnitude that could jeopardise this anchoring materialise,” he said.

Another Governing Council member Olli Rehn said, “It seems necessary that in our policy rates we move relatively quickly out of negative territory and continue our gradual process of monetary policy normalization.”

Eurozone CPI finalized at 7.4% yoy in Apr, core CPI at 3.5% yoy

Eurozone CPI was finalized at 7.4% yoy in April, unchanged from March’s reading. Core CPI was finalized at 3.5% yoy, up from March’s 3.0% yoy. The highest contribution to the annual Eurozone inflation rate came from energy (+3.70%), followed by services (+1.38%), food, alcohol & tobacco (+1.35%) and non-energy industrial goods (+1.02%).

EU CPI was finalized at 8.1% yoy, up from March’s 7.8% yoy. The lowest annual rates were registered in France, Malta (both 5.4%) and Finland (5.8%). The highest annual rates were recorded in Estonia (19.1%), Lithuania (16.6%) and Czechia (13.2%). Compared with March, annual inflation fell in three Member States, remained stable in two and rose in twenty-two.

UK CPI rose to 9% yoy in Apr, core CPI up to 6.2% yoy

UK CPI accelerated sharply from 7.0% yoy to 9.0% yoy in April, but missed expectation of 9.1% yoy. CPI core rose from 5.7% yoy to 6.2% yoy, matched expectations. RPI accelerated form 9.0% to 11.1% yoy, matched expectations.

Headline CPI was another record high since the National Statistics series began in 1997. It’s also the highest record rate in the constructed historical series which began in 1989.

Based on the recently published modelled consumer price inflation data by the ONS, CPI was last higher sometime around 1982, where estimates range between approximately 6.5 % in December to nearly 11% in January.

In response to the release, Chancellor of the Exchequer Rishi Sunak said: “Today’s inflation numbers are driven by the energy price cap rise in April, which in turn is driven by higher global energy prices.

“We cannot protect people completely from these global challenges but are providing significant support where we can, and stand ready to take further action.”

Also released, PPI input came in at 1.1% mom, 18.6%, versus expectation of 2.6% mom, 20.7% yoy. PPI output was at 2.3% mom, 14.0% yoy, versus expectation of 1.6% mom, 12.5% yoy. PPI output core was at 1.6% mom, 13.0% yoy, versus expectation of 1.6% mom, 12.6% yoy.

Japan GDP contracted -0.2% qoq, -1.0% annualized in Q1

Japan GDP contracted -0.2% qoq in Q1, better than expectation of -0.4% qoq. In annualized term, GDP contracted -1.0%, first negative growth in two quarters, but better than expectation of -1.8%. GDP deflator dropped -0.4% yoy, also better than expectation of -1.2% yoy.

Economy minister Daishiro Yamagiwa said the economy has not returned to pre-pandemic levels but that further downside would likely be limited. He also expected the economy to pick up even though uncertainty remains due to Ukraine situation. Also, China’s zero-covid policy is having a significant impact on supply chains.

Australia Westpac leading index dropped to 0.88%, expects 40bps RBA hike in Jun

Australia Westpac-MI leading index dropped from 1.69% to 0.88% in April. Westpac recently revised down growth forecast for 2022 from 5.5% to 4.5%, reflecting the sharp increase in cost of living, and an earlier and more rapid RBA tightening policy.

As for RBA meeting on June 7, Westpac expects the central bank to hike by a further 40bps to 0.75%, even though most analysts favored a cautious move of 25bps. Westpac said, “It is also much more prudent to front load the increases where at a stage in the cycle when rates are clearly below what might be considered a ‘neutral’ level.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2374; (P) 1.2436; (R1) 1.2557; More..

GBP/USD dips mildly today but overall, it’s staying in consolidation from 1.2154. Intraday bias remains neutral at this point and further decline will remain in favor as long as 1.2637 resistance holds. On the downside, break of 1.2154 will resume the down trend from 1.4248 to 200% projection of 1.3641 to 1.2999 from 1.3297 at 1.2013. However, considering bullish convergence condition in 4 hour MACD, break of 1.2637 will confirm short term bottoming at 1.2154. Intraday bias will be turned back to the upside for 55 day EMA (now at 1.2816).

{kind=link}

In the bigger picture, based on current momentum, fall from 1.4248 (2018 high) at least at the same degree as the rise from 1.1409 (2020 low). That is, fall from 1.4248 could be a leg inside the pattern from 1.1409, or resuming the longer term down trend. In either case, deeper decline is expected as long as 1.2999 support turned resistance holds. Next target is 1.1409 low.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Q/Q Q1 P | -0.20% | -0.40% | 1.10% | |

| 23:50 | JPY | GDP Deflator Y/Y Q1 P | -0.40% | -1.20% | -1.30% | 1.10% |

| 00:30 | AUD | Westpac Leading Index M/M Apr | -0.20% | 0.30% | ||

| 00:30 | AUD | Wage Price Index Q/Q Q1 | 0.70% | 0.80% | 0.70% | |

| 04:30 | JPY | Industrial Production M/M Mar F | 0.30% | 0.30% | 0.30% | |

| 06:00 | GBP | CPI M/M Apr | 2.50% | 2.60% | 1.10% | |

| 06:00 | GBP | CPI Y/Y Apr | 9.00% | 9.10% | 7.00% | |

| 06:00 | GBP | Core CPI Y/Y Apr | 6.20% | 6.20% | 5.70% | |

| 06:00 | GBP | RPI M/M Apr | 3.40% | 3.40% | 1.00% | |

| 06:00 | GBP | RPI Y/Y Apr | 11.10% | 11.10% | 9.00% | |

| 06:00 | GBP | PPI Input M/M Apr | 1.10% | 2.60% | 5.20% | 4.60% |

| 06:00 | GBP | PPI Input Y/Y Apr | 18.60% | 20.70% | 19.20% | 18.60% |

| 06:00 | GBP | PPI Output M/M Apr | 2.30% | 1.60% | 2.00% | 1.90% |

| 06:00 | GBP | PPI Output Y/Y Apr | 14.00% | 12.50% | 11.90% | |

| 06:00 | GBP | PPI Core Output M/M Apr | 1.60% | 1.60% | 2.00% | 1.80% |

| 06:00 | GBP | PPI Core Output Y/Y Apr | 13.00% | 12.70% | 12.00% | 11.80% |

| 09:00 | EUR | Eurozone CPI Y/Y Apr F | 7.40% | 7.50% | 7.50% | |

| 09:00 | EUR | Eurozone Core CPI Y/Y Apr F | 3.50% | 3.50% | 3.50% | |

| 12:30 | CAD | CPI M/M Apr | 0.60% | 0.70% | 1.40% | |

| 12:30 | CAD | CPI Y/Y Apr | 6.80% | 6.70% | 6.70% | |

| 12:30 | CAD | CPI Common Y/Y Apr | 3.20% | 2.90% | 2.80% | 3.00% |

| 12:30 | CAD | CPI Median Y/Y Apr | 4.40% | 3.90% | 3.80% | 4.00% |

| 12:30 | CAD | CPI Trimmed Y/Y Apr | 5.10% | 4.70% | 4.70% | 4.80% |

| 12:30 | USD | Building Permits Apr | 1.82M | 1.83M | 1.87M | 1.88M |

| 12:30 | USD | Housing Starts Apr | 1.72M | 1.77M | 1.79M | 1.73M |

| 14:30 | USD | Crude Oil Inventories | 2.1M | 8.5M |