Canadian Dollar Jumps With Oil Rally, Yen Staying Weak

Canadian Dollar is trading as the strongest one so far for the week. Rising oil price is giving extra support to the Loonie, on the back of improving overall risk sentiment. Aussie and Euro are firm behind too. Yen remains the worst performing one, followed by Swiss Franc and Dollar, while Sterling is mixed. US markets will be back from holiday and attention will be on whether last week’s strong rebound in stocks could extend.

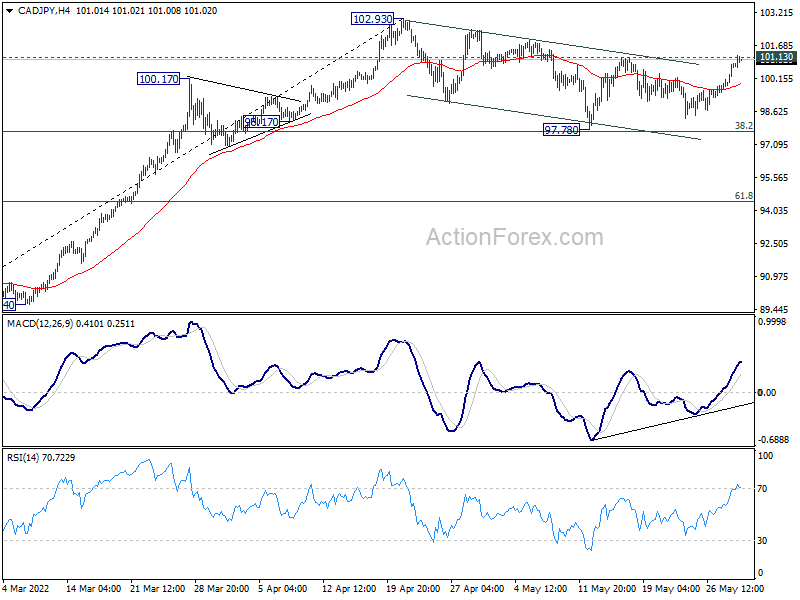

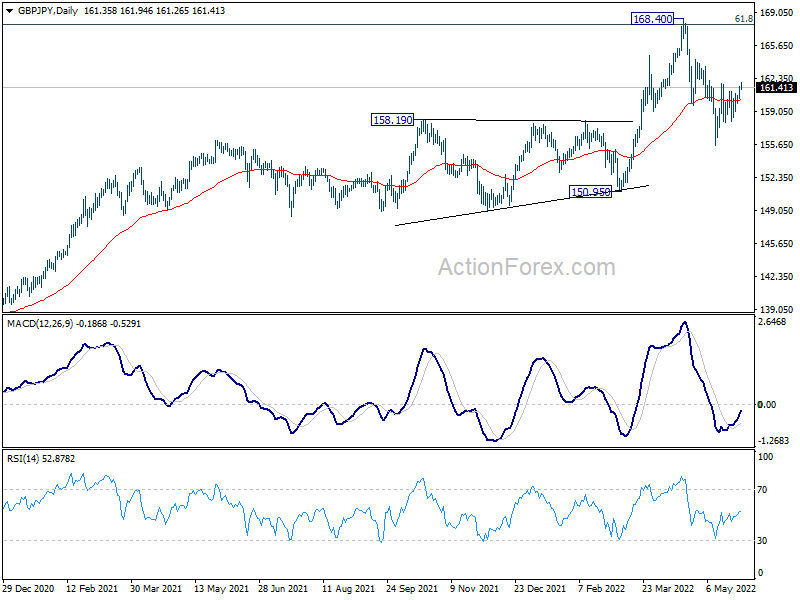

Technically, focuses will stay on the rallies in Yen pairs. CAD/JPY is now pressing 101.13 resistance while GBP/JPY is pressing 161.83. Break of these two levels will resume the rebound from 97.78 and 155.57 respectively. Such developments could trigger some upside acceleration to retest recent highs. That would also affirm that overall market sentiment continues to improve.

{kind=link}

In Asia, at the time of writing, Nikkei is down -0.19%. Hong Kong HSI is up 0.43%. China Shanghai SSE is up 0.75%. Singapore Strait Times is up 0.41%. Japan 10-year JGB yield is up 0.0138 at 0.247.

Japan industrial production dropped -1.3% mom in Apr, expected to return to growth in May

Japan industrial production dropped -1.3% mom in April, much worse than expectation of -0.2% mom. It’s also the first decline in three months. The seasonally adjusted production index for the manufacturing and mining sectors stood at 95.2 against 100 for the base year of 2015.

Manufacturers surveyed by the Ministry of Economy, Trade and Industry expected output to return to growth in May, gaining 4.8%, followed by a 8.9% rise in June.

Also from Japan, unemployment rate dropped from 2.6% to 2.5% in April, lowest in two years. Retail sales rose 2.9% yoy, above expectation of 2.6% yoy.

China PMI manufacturing rose to 49.6 in May, services rose to 47.8

The official China PMI manufacturing rose from 47.4 to 49.6 in May, matched expectations. PMI Services rose from 41.9 to 47.8, above expectation of 45.2. PMI Composite also rose from 42.7 to 48.4.

“This showed manufacturing production and demand have recovered to varying degrees, but the recovery momentum needs to be strengthened,” said Zhao Qinghe, senior statistician at the NBS.

WTI oil to clear 120 as EU bans 2/3 of Russia import immediately

WTI crude oil is extending recent rally and it’s now eyeing 120 handle. EU leaders finally agreed yesterday to embargo on seaborne oil imports from Russia, which covers more than two-thirds of the imports. Another one-third is delivered via the Druzhba pipeline. Also, the embargo would be raised to 90% once Poland and Germany, which are connected to the pipeline, stop buying by the end of the year. The remaining 10% temporarily exempt including imports to Hungary along with Slovakia and Czech.

“This immediately covers more than 2/3 of oil imports from Russia, cutting a huge source of financing for its war machine. Maximum pressure on Russia to end the war,” European Council President Charles Michel said in a tweet.

WTI crude oil’s break of the near term channel resistance suggests upside acceleration. 118.57 near term resistance is also taken out. As long as 114.27 support holds, further rally would be seen, back towards 131.82 high.

Nevertheless, current rally from 93.47 is tentatively seen as the second leg of the medium term corrective pattern from 131.82. Hence, a firm break of 131.82 is not expected for now while sideway trading could extend for some more time.

{kind=link}

{kind=link}

Bitcoin heading to 55 D EMA as near term rebound resumes

On the back of improving market sentiment, Bitcoin rises through 31407 resistance to resume the rebound from 25083. Further rally is now expected to 55 day EMA (now at 34297). Sustained break there will further affirm the case that whole decline from 68986 has completed with three waves down to 25083.

It’s still a bit too early to confirm a bullish trend reversal for the moment. But even as a corrective rebound, firm break of 44 day EMA should pave the way to 38.2% retracement of 68986 to 25083 at 41853 at least. For now, this will remain the favored case as long as 27993 support holds.

{kind=link}

{kind=link}

Looking ahead

Swiss trade balance, retail sales and GDP will be released in European session. France GDP and consumer spending, Germany employment, UK M4 and money supply will also be featured. But main focus will likely be on Eurozone CPI flash. Later in the day, Canada will release GDP. US will release house price index, Chicago PMI, and consumer confidence.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 160.71; (P) 161.12; (R1) 161.89; More…

Intraday bias in GBP/JPY remains neutral with focus on 161.83 resistance. Firm break there should confirm that correction from 168.40 has completed at 155.57 already. Intraday bias will be back on the downside for retesting 168.40 high next. nevertheless, on the downside, break of 155.57 will extend the correction towards 150.96 key structural support.

{kind=link}

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Sustained break of 61.8% retracement of 195.86 (2015 high) to 122.75 (2016 low) at 167.93 will be a long term bullish signal, and could pave the way back to 195.86 high. This will now remain the favored case as long as 150.95 support holds, even in case of deep pull back. However, firm break of 150.95 will indicate rejection by 167.93, and bearish trend reversal.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Apr | -8.50% | 5.80% | 6.20% | |

| 23:30 | JPY | Unemployment Rate Apr | 2.50% | 2.60% | 2.60% | |

| 23:50 | JPY | Industrial Production M/M Apr P | -1.30% | -0.20% | 0.30% | |

| 23:50 | JPY | Retail Trade Y/Y Apr | 2.90% | 2.60% | 0.90% | |

| 01:00 | NZD | ANZ Business Confidence May | -55.6 | -42 | ||

| 01:30 | AUD | Building Permits M/M Apr | -2.40% | 2.00% | -18.50% | -19.20% |

| 01:30 | AUD | Private Sector Credit M/M Apr | 0.80% | 0.50% | 0.40% | 0.60% |

| 01:30 | AUD | Current Account Balance (AUD) Q1 | 7.5B | 13.4B | 12.7B | 13.2B |

| 01:30 | CNY | Manufacturing PMI May | 49.6 | 49.6 | 47.4 | |

| 01:30 | CNY | Non-Manufacturing PMI May | 47.8 | 45.2 | 41.9 | |

| 05:00 | JPY | Housing Starts Y/Y Apr | 3.00% | 6.00% | ||

| 05:00 | JPY | Consumer Confidence Index May | 33.9 | 33 | ||

| 06:00 | CHF | Trade Balance (CHF) Apr | 3.50B | 2.99B | ||

| 06:30 | CHF | Real Retail Sales Y/Y Apr | -1.40% | -6.60% | ||

| 06:45 | EUR | France Consumer Spending M/M Apr | 1.30% | -1.30% | ||

| 06:45 | EUR | France GDP Q/Q Q1 | 0.00% | 0.00% | ||

| 07:00 | CHF | GDP Q/Q Q1 | 0.30% | 0.30% | ||

| 07:55 | EUR | Germany Unemployment Change May | -16K | -13K | ||

| 07:55 | EUR | Germany Unemployment Rate May | 5.00% | 5.00% | ||

| 08:30 | GBP | M4 Money Supply M/M Apr | 0.20% | 0.10% | ||

| 08:30 | GBP | Mortgage Approvals (GBP) Apr | 72K | 71K | ||

| 09:00 | EUR | Eurozone CPI Y/Y May P | 7.70% | 7.50% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y May P | 3.50% | 3.50% | ||

| 12:30 | CAD | GDP M/M Mar | 0.50% | 1.10% | ||

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Mar | 20.80% | 20.20% | ||

| 13:00 | USD | Housing Price Index M/M Mar | 1.80% | 2.10% | ||

| 13:45 | USD | Chicago PMI May | 55.8 | 56.4 | ||

| 14:00 | USD | Consumer Confidence May | 103.9 | 107.3 |