Dollar Surges as CPI Reaccelerates on Energy and Food Prices

Dollar rises strongly in early US session after CPI data. Headline inflation reaccelerated with strong rise in energy and food prices From this perspective, there is little scope for Fed to pause tightening in September. It might instead continue its 50bps per meeting plan for longer. The greenback is now the strongest one for the week, followed by Sterling. Swiss Franc is the worst performing, followed by Yen. Euro is mixed despite ECB’s clear hawkish stance while Aussie is weighed down by risk-off sentiment.

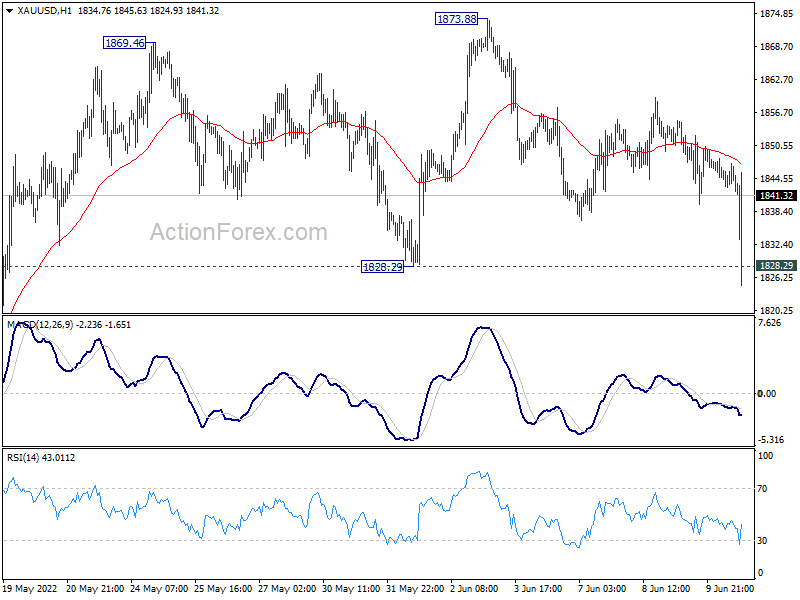

Technically, GBP/USD’s break of 1.2429 minor support is another evidence of Dollar strength. One focus before the end of the week would be 0.7034 minor support in AUD/USD. Also, there is some knee jerk actions in Gold, which breached 1828.29 support briefly. Attention will also be on whether Gold’s selloff will come back quickly on Dollar strength, and break through 1828.29 firmly.

{kind=link}

In Europe, at the time of writing, FTSE is down -1.61%. DAX is down -1.69%. CAC is down -1.90%. Germany 10-year yield is down -0.0113 at 1.421. Earlier in Asia, Nikkei dropped -1.49%. Hong Kong HSI dropped -0.29%. China Shanghai SSE rose 1.42%. Singapore Strait Times dropped -0.87%. Japan 10-year JGB yield rose 0.0038 to 0.254.

US CPI rose to 8.6% yoy, highest since 1981, food price rose 10.1% yoy

US CPI accelerated again from 8.3% yoy to 8.6% yoy in May, well above expectation of 8.2% yoy. That’s the highest level since December 1981. CPI core slowed from 6.2% yoy to 6.0% yoy, above expectation of 5.9% yoy. Energy index rose 34.6% yoy, largest 12-month increase since September 2005. Food index rose 10.1% yoy, first rise above 10% since March 1981.

CPI rose 1.0% mom, above expectation of 0.7% mom. Core CPI rose 0.6% mom, above expectation of 0.5% mom.

Canada employment rose 39.8k in May, unemployment rate dropped to 5.1% record low

Canada employment rose 39.8k in May, above expectation of 28.5k. Full time work rose 135k while part time jobs dropped -96k. Services producing jobs rose 81k while goods-producing jobs dropped -41.

Unemployment rate dropped form 5.2% to 5.1%, below expectation of 5.2%. That’s a new record low. Total hours worked rose 5.1% yoy. Average hourly wages rose 3.9% yoy.

Bundesbank: Germany inflation to hit 7% or higher, resolute action needed

Bundesbank revised down growth projection for Germany’s GDP in 2022 and 2023, and upgraded inflation projection for 2022, 2023, and 2024.

2022 GDP growth is slashed from 4.2% to just 1.9%. 2023 growth was cut from 3.2% to 2.4%. But 2024 growth was raised from 0.9% to 1.8%.

2022 HICP inflation forecast was raised from 3.6% to 7.1%. 2023 HICP forecast was raised from 2.25% to 4.5%. 2024 HICP forecast was raised from 2.2% to 2.6%.

President Joachim Nagel said: “Inflation this year will be even stronger than it was at the beginning of the 1980s. Price pressures have even intensified again recently, which is not fully reflected in the present projections. If this development is assumed to continue, the annual average HICP rate for 2022 could be considerably above 7%”.

Euro area inflation rates won’t fall by themselves,” Nagel added. “Monetary policy is called upon to reduce inflation through resolute action.”

Villeroy: ECB will pursue gradual but sustained rate hikes to neutral

ECB Governing Council member Francois Villeroy de Galhau told French radio that inflation is “not only too high but also too broad”. The ECB will purse a “gradual but sustained” rate hikes until reaching neutral range. He estimated that it’s “somewhere between 1% and 2%”.

Separately, another Governing Council member Robert Holzmann said, “financial markets reacted very well to yesterday’s announcement.” “Even if we had started with a 50 bps rate hike it might have an effect on credibility but it would have raised expectations of bigger rate rises afterwards,” he added.

China PPI slowed to 14-mth low, CPI unchanged

China PPI slowed notably from 8.0% yoy to 6.4% yoy in May, below expectation of 6.5% yoy. That’s also the lowest level in 14 months since March 2021. CPI was unchanged at 2.1% yoy, below expectation of 2.5% yoy. Core CPI, excluding food and energy, was unchanged at 0.9% yoy.

“In May, the pandemic control continued to improve, with overall sufficient supplies in the consumer market, CPI has decreased compared to last month, and the year-on-year increase remained stable,” said senior NBS statistician Dong Lijuan. “As a great amount of fresh vegetables entered the market and logistics gradually smooth, prices of fresh vegetables fell by 15 per cent”.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2469; (P) 1.2514; (R1) 1.2540; More…

GBP/USD’s break of 1.2429 minor support argues that rebound from 1.2154 has completed at 1.2666 already. Intraday bias is back on the downside for retesting 1.2154 low. Firm break there will resume larger down trend. Next target is 61.8% projection of 1.3297 to 1.2154 from 1.2666 at 1.1960. For now, risk will stay on the downside as long as 1.2666 resistance holds, in case of recovery.

{kind=link}

In the bigger picture, fall from 1.4248 (2018 high) could be a leg inside the pattern from 1.1409 (2020 low), or resuming the longer term down trend. Deeper decline is expected as long as 1.2999 support turned resistance holds. On resumption, next target is 1.1409 low.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Manufacturing Sales Q1 | 1.20% | 8.20% | 11.90% | |

| 23:50 | JPY | PPI Y/Y May | 9.10% | 9.80% | 10.00% | 9.80% |

| 01:30 | CNY | CPI Y/Y May | 2.10% | 2.50% | 2.10% | |

| 01:30 | CNY | PPI Y/Y May | 6.40% | 6.50% | 8.00% | |

| 08:00 | EUR | Italy Industrial Output M/M Apr | 1.60% | -1.60% | 0.00% | |

| 12:30 | CAD | Net Change in Employment May | 39.8K | 28.5K | 15.3K | |

| 12:30 | CAD | Unemployment Rate May | 5.10% | 5.20% | 5.20% | |

| 12:30 | USD | CPI M/M May | 1.00% | 0.70% | 0.30% | |

| 12:30 | USD | CPI Y/Y May | 8.60% | 8.20% | 8.30% | |

| 12:30 | USD | CPI Core M/M May | 0.60% | 0.50% | 0.60% | |

| 12:30 | USD | CPI Core Y/Y May | 6.00% | 5.90% | 6.20% | |

| 14:00 | USD | Michigan Consumer Sentiment Index Jun P | 56.9 | 58.4 |