Markets Turn Cautious ahead of FOMC, Fed to Hike 50bps or 75bps?

The forex markets are generally staying inside yesterday’s range so far today. Stocks in Europe and US futures are recovering while treasury yields retreat. Traders are clearly turning cautious ahead of FOMC rate decision. The question is whether Fed would deliver 75bps hike as markets priced in, or stick to its 50bps per meeting plan. Euro’s recovery attempt was brief as ECB delivered nothing special after the ad hoc meeting on fragmentation.

Technically, focuses remain on some levels to confirm Dollar’s underlying strength, if it attempts to rally after FOMC. The levels include 1.0348 in EUR/USD, 0.6828 support in AUD/USD, 1.0063 resistance in USD/CHF and 1.3075 resistance in USD/CAD.

In Europe, at the time of writing, FTSE is up 0.99%. DAX is up 0.97%. CAC is up 0.78%. Germany 10-yaer yield is down -0.132 at 1.620. Earlier in Asia, Nikkei dropped -1.14%. Hong Kong HSI rose 1.14%. China Shanghai SSE rose 0.50%. Singapore Strait Times dropped -0.10%. Japan 10-year JGB yield dropped -0.0008 to 0.256.

Some readings on Fed:

US retail sales dropped -0.3% mom in May, ex-auto sales up 0.5% mom

US retail sales dropped -0.3% mom to USD 672.9B in May, worse than expectation of 0.2% mom rise. Ex-auto sales rose 0.5% mom, below expectation of 0.8% mom. Ex-gasoline sales dropped -0.7% mom. Ex-auto, ex-gasoline sales rose 0.1% mom. Retail trade sales were down -0.4% mom.

For the 12-month period, retail sales rose 8.1% yoy. Gasoline station jumped 43.2% yoy. Food & beverage stores rose 7.9% yoy.

Also released, import price index rose 0.6% mom in May, versus expectation of 1.1% mom. Empire State Manufacturing index rose from -11.6 to -1.2, below expectation of 5.0.

ECB to apply flexibility in PEPP reinvestment, design new anti-fragmentation instrument

ECB said the Governing Council in an ad hoc meeting today to “exchange views on the current market situation” and reiterated the pledged to “act against resurgent fragmentation risks”.

The council decided to “apply flexibility in reinvesting redemptions coming due in the PEPP portfolio, with a view to preserving the functioning of the monetary policy transmission mechanism”.

Also, it decided to “mandate the relevant Eurosystem Committees together with the ECB services to accelerate the completion of the design of a new anti-fragmentation instrument”.

Eurozone industrial production rose 0.4% mom in Apr, EU up 0.3% mom

Eurozone industrial production rose 0.4% mom in April, below expectation of 0.5% mom. Production of energy rose by 5.4%, intermediate goods by 0.7%, non-durable consumer goods by 0.4% and durable consumer goods by 0.2%, while production of capital goods fell by -0.2%.

EU industrial production rose 0.3% mom. Among Member States for which data are available, the highest monthly increases were registered in the Netherlands (+5.6%), Finland (+3.5%) and Luxembourg (+3.2%). The largest decreases were observed in Ireland (-9.6%), Greece (-7.4%) and Lithuania (-7.1%).

Eurozone goods exports rose 12.6% yoy in Apr, imports rose 39.4% yoy

Eurozone goods exports rose 12.6% yoy in April to EUR 223.9B. Imports rose 39.4% yoy to EUR 256.4B. Trade deficit came in at EUR -32.4B. Intra-Eurozone trade rose 20.8% yoy to EUR 212.1B.

In seasonally adjusted term, exports rose 1.5% mom to EUR 229.7B. Imports rose 7.1% mom to EUR 261.4%. Trade deficit widened to EUR -31.7B, much larger than expectation of EUR -14.5B. Intra-Eurozone trade rose slightly from 211.2B to 215.1B.

SECO downgrades Swiss GDP forecasts, upgrades inflation

Swiss SECO downgraded 2022 GDP growth forecasts (sport event adjusted) from 2.8% to 2.6%. 2023 GDP growth was also lowered from 2.0% to 1.9%. On the other hand, CPI forecast for 2022 was raised from 1.9% to 2.5%. CPI for 2023 was also raised from 0.7% to 1.4%. Unemployment rate forecast was left unchanged at 2.1% in 2022 and 2.0% in 2023.

SECO said: “The Swiss economy made a solid start to the year, but prospects for the international environment have waned. In particular, the global economy is at risk from the war in Ukraine and developments in China.”

It also warned: “The Swiss economy would be significantly affected if its key trading partners were to suffer a major economic downturn. This could happen, for example, as a result of widespread short-falls in energy supplies from Russia… In the face of rising interest rates, the risks associated with the surge in international debt levels are intensifying. There is an increased probability of financial market corrections.”

Australia Westpac consumer sentiment dropped to 86.5, on inflation and interest rate

Australia Westpac Consumer Sentiment dropped from 90.4 to 86.5 in June. Over the 46-year history of the survey, the reading was only at or below this level during “major economic dislocations”, including during COVID-19, the Global Financial Crisis, early 90s recession, mid-80s slowdown and early 80s recession.

Westpac said: “The survey detail shows a clear picture of a slump in sentiment being driven by rising inflation; an associated lift in interest rates; and a loss of confidence around the economic outlook, both here and abroad.”

Regarding RBA policy, Westpac expects another 50bps rate hike in July, as the central bank needs to move quickly in the early stages in a tightening cycle when interest rates are clearly below neutral and risk of over-tightening is moderate.

China industrial production rose 0.7% yoy in May, retail sales down -6.7% yoy

China industrial production rose 0.7% yoy in May, much better than expectation of -1.0% yoy decline. Retail sales dropped -6.7% yoy, above expectation of -7.3% yoy. Fixed asset investment rose 6.2% ytd yoy, above expectation of 6.0%.

The National Bureau of Statistics said the economy “showed a good momentum of recovery” in the month, “with negative effects from Covid-19 pandemic gradually overcome and major indicators improved marginally.”

Still, it warned, “we must be aware that the international environment is to be even more complicated and grim, and the domestic economy is still facing difficulties and challenges for recovery.”

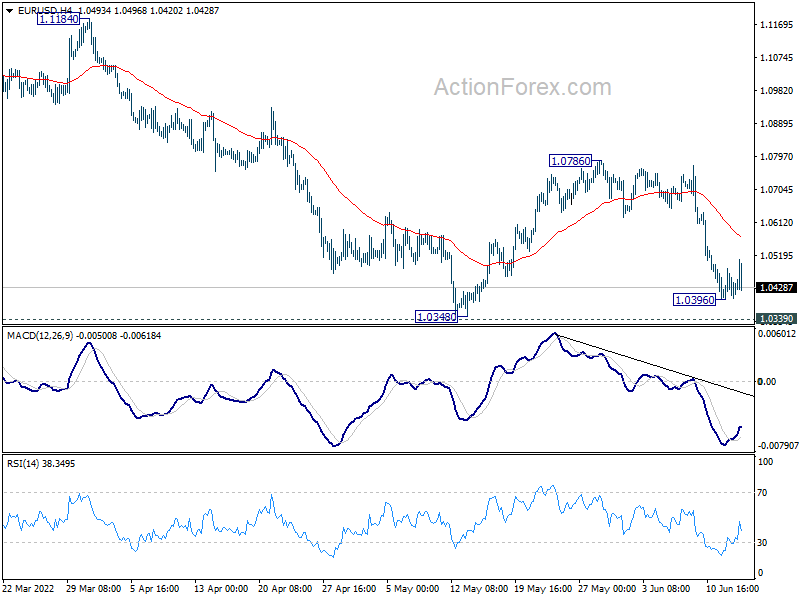

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0382; (P) 1.0434 (R1) 1.0470; More…

Intraday bias in EUR/USD remains neutral for the moment. Risk stays on the downside as long as 1.0786 resistance holds. Below 1.0396 will target 1.0339 long term support. Decisive break there will resume larger down trend. Next target is long term projection level at 1.0090.

{kind=link}

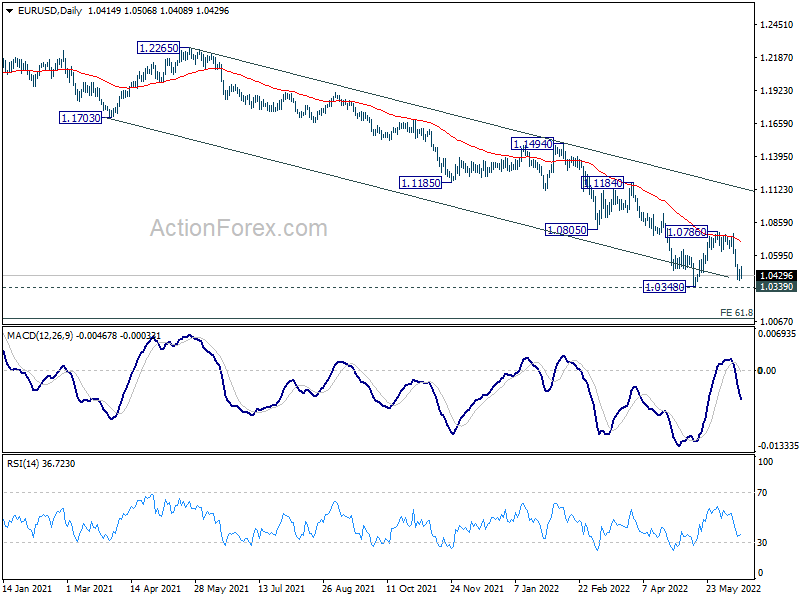

In the bigger picture, focus stays on 1.0339 long term support (2017 low). Decisive break there will resume whole down trend from 1.6039 (2008 high). Next target is 61.8% projection of 1.3993 to 1.0339 from 1.2348 at 1.0090. However, firm break of 1.0805 support turned resistance will delay this bearish case, and bring stronger rebound first.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Current Account (NZD) Q1 | -6.14B | -5.96B | -7.26B | -7.34B |

| 23:50 | JPY | Machinery Orders M/M Apr | 10.80% | -1.50% | 7.10% | |

| 00:30 | AUD | Westpac Consumer Confidence Jun | -4.50% | -5.60% | ||

| 02:00 | CNY | Industrial Production Y/Y May | 0.70% | -1.00% | -2.90% | |

| 02:00 | CNY | Retail Sales Y/Y May | -6.70% | -7.30% | -11.10% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y May | 6.20% | 6.00% | 6.80% | |

| 04:30 | JPY | Tertiary Industry Index M/M Apr | 0.70% | 0.80% | 1.30% | 1.70% |

| 06:30 | CHF | Producer and Import Prices M/M May | 0.90% | 0.60% | 1.30% | |

| 06:30 | CHF | Producer and Import Prices Y/Y May | 6.90% | 6.90% | 6.70% | |

| 07:00 | CHF | SECO Economic Forecasts | ||||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Apr | -31.7B | -14.5B | -17.6B | |

| 09:00 | EUR | Eurozone Industrial Production M/M Apr | 0.40% | 0.50% | -1.80% | |

| 12:15 | CAD | Housing Starts May | 287K | 265K | 267K | |

| 12:30 | USD | NY Empire State Manufacturing Index Jun | -1.2 | 5 | -11.6 | |

| 12:30 | USD | Retail Sales M/M May | -0.30% | 0.20% | 0.90% | 0.70% |

| 12:30 | USD | Retail Sales ex Autos M/M May | 0.50% | 0.80% | 0.60% | 0.40% |

| 12:30 | USD | Import Price Index M/M May | 0.60% | 1.10% | 0.00% | |

| 14:00 | USD | Business Inventories Apr | 1.20% | 2.00% | ||

| 14:00 | USD | NAHB Housing Market Index Jun | 68 | 69 | ||

| 14:30 | USD | Crude Oil Inventories | -2.3M | 2.0M | ||

| 18:00 | USD | Fed Interest Rate Decision | 1.50% | 1.00% | ||

| 18:30 | USD | FOMC Press Conference |