Selloff in Aussie Intensifies With Commodity Prices

Selloff in Aussie and Kiwi intensifies today following the steep decline in commodities. Safe-have flows continue to boost the Japanese Yen, which is additionally lifted by extended pull back in US and European benchmark yields. As for the week, Dollar is the strongest one, but the second placed Yen has the potential to overtake it. There is little chance for Aussie and Kiwi to reverse their worst performer places for the week.

In Europe, at the time of writing, FTSE is down -0.04%. DAX is flat, CAC is up 0.06%. Germany 10-year yield is down -0.074 at 1.265. Earlier in Asia, Nikkei dropped -1.73%. China Shanghai SSE dropped -0.32%. Singapore Strait Times dropped -0.21%. Japan 10-year JGB yield dropped -0.010 to 0.221.

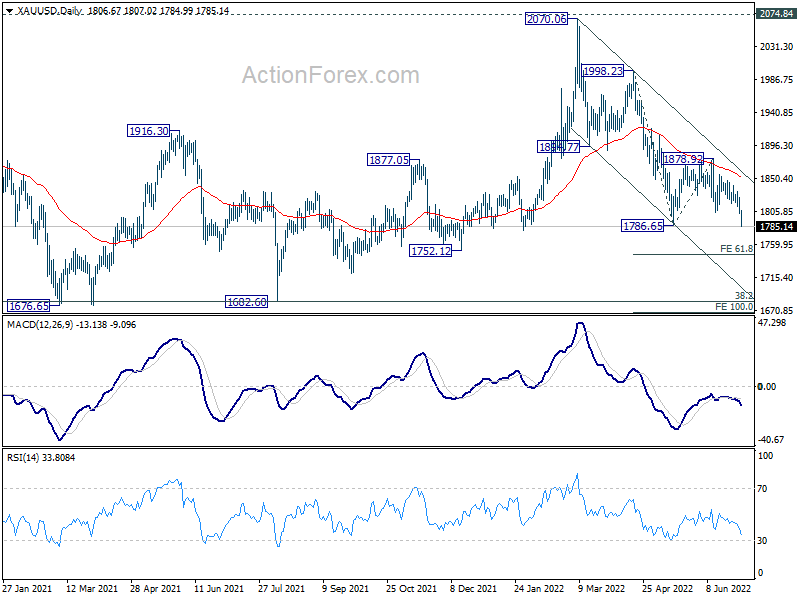

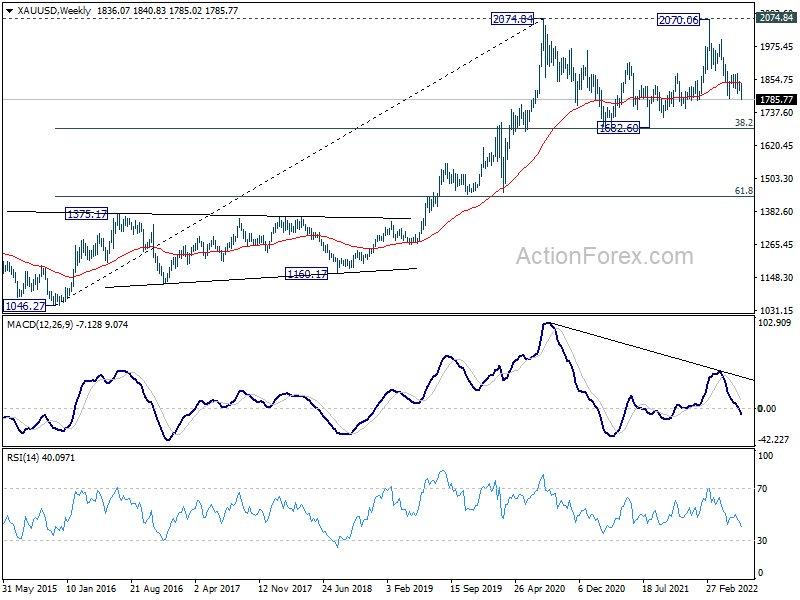

Gold downside breakout, targets 1748

Gold’s selloff is finally picking up momentum today and breach of 1786.65 support indicates resumption of whole decline from 2070.06. Further fall should be seen to 61.8% projection of 1998.23 to 1786.65 from 1878.92 at 1748.16.

It should be noted that fall from 1786.65 should now be in its fifth leg. That is, it should be near completion. Also, such decline is seen as the third leg of the consolidation pattern from 2074.84 (2020 high). Based on current structure, while break of 1748.16 cannot be ruled out, downside should be contained above 1682.60 support (38.2% retracement of 1046.27 to 2074.84 at 1681.92).

{kind=link}

{kind=link}

Eurozone CPI accelerated to 8.6% yoy in Jun, but core CPI slowed to 3.7% yoy

Eurozone CPI accelerated from 8.1% yoy to 8.6% yoy in June, above expectation of 8.3% yoy. However, CPI core slowed from 3.8% yoy to 3.7% yoy, below expectation of 3.9% yoy.

Looking at the main components, energy is expected to have the highest annual rate in June (41.9%, compared with 39.1% in May), followed by food, alcohol & tobacco (8.9%, compared with 7.5% in May), non-energy industrial goods (4.3%, compared with 4.2% in May) and services (3.4%, compared with 3.5% in May).

Eurozone PMI manufacturing finalized at 22-mth low at 52.1, increasing likelihood of manufacturing recession

Eurozone PMI Manufacturing was finalized at 52.1 in June, down from April’s 54.6. That’s also the lowest level in 22 months. Readings of the member states were also weak, with the Netherlands at 19-month low of 55.9, Ireland at 16-month low at 53.1, Spain at 17-month low at 52.6, Germany at 23-month low at 52.0, France at 18-month low at 51.4, Austria at 22-month low at 51.2, Greece at 16-month low at 51.1, Italy at 24-month low at 50.9.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said: “Eurozone manufacturing has moved into decline in June, with production dropping for the first time for two years amid a steepening downturn in demand…. The downturn looks set to gain momentum in coming months…. One upside to the recent weakening of demand is an alleviation of some supply chain constraints, which has in turn helped cool inflationary pressures for industrial goods. With the survey data indicating an increasing likelihood of the manufacturing sector slipping into a recession, these price pressures should ease further in the third quarter.”

UK PMI manufacturing finalized at 52.8 in Jun, economic backdrop to darken further in H2

UK PMI Manufacturing was finalized at 52.8 in June, down from May’s 54.6, a two-year low. S&P Global said output growth slowed to near-stagnation pace as new orders intakes fell for the first time since January 2021. Price inflation remained elevated despite further easing.

Rob Dobson, Director at S&P Global Market Intelligence, said: “UK manufacturing output growth ground to a near standstill in June, as intakes of new work contracted for the first time since January 2021. Domestic market conditions became increasingly difficult and foreign demand fell sharply again… Business confidence took a hit as a result, dipping to its gloomiest since mid-2020… “There were some welcome signs that supply-chain constraints and cost inflationary pressures may have passed their peaks. However, with these constraints still elevated overall and demand headwinds rising, it is likely that UK manufacturing will see the economic backdrop darken further in the second half of the year.”

Japan Tankan large manufacturing index dropped to 9 in Q2

Japan Tankan survey showed that large manufacturer sentiment dropped to lowest in more than a year. But note improvement was seen in the non-manufacturing sector. Also, the strong capital expenditure plan was a big surprise, showing that corporate spending was still robust despite increasing uncertainty.

Large manufacturing index dropped from 14 to 9 in Q2, below expectation of 13. That’s the lowest level since Q1 2021. Large manufacturing outlook improved from 9 to 10, below expectation of 14.

Non-manufacturing index rose from 9 to 13, below expectation of 14. Non-manufacturing outlook rose from 7 to 13, below expectation of 17.

Capex plans for big firms seen rising 18.6% yoy in fiscal 2022, well above expectation of 8.9%.

Consumer inflation expectations rose from 1.8% to 2.4%. Three years ahead, consumer prices are expected to rise 2%, up from 1.6%.

Japan PMI manufacturing finalized at 52.7, optimism improved

Japan PMI Manufacturing was finalized at 52.7 in June, down from May’s 53.3. S&P Global said output growth slowed amid near-stagnation in new orders. Prices charged for goods rose at sharpest pace on record. Business optimism improved to three-month high.

Usamah Bhatti, Economist at S&P Global Market Intelligence, said: “June PMI data pointed to a softer expansion of the Japanese manufacturing sector… Panel members often commented that rising price and supply pressures amid sustained disruption and delays had held back activity in the sector… That said, the degree of optimism regarding the 12-month outlook for output strengthened to a three-month high in June… This is broadly in line with the estimate for industrial production to grow just 2% in 2022 before an acceleration in 2023.”

China Caixin PMI manufacturing rose to 51.7, restoration in the post-pandemic era

China Caixin PMI Manufacturing rose from 48.1 to 51.7 in June, above expectation of 50.2. Caixin said production increased at quickest rate for 19 months, as total new work and export sales returned to growth. Supplier performance stabilized.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Restoration in the post-pandemic era remained the focus of the current economy, yet its base was far from strong. Deteriorating household income and expectations caused by a weak labor market dampened the demand recovery. Correspondingly, supportive policies should target employees, gig workers and low-income groups impacted by the outbreaks.”

Australia AiG manufacturing rose to 54, exports jumped but domestic sales fell

Australia AiG Performance of Manufacturing rose 1.6 pts to 54.0 in June. Looking at some details, production rose 2.4 to 54.7. Employment rose 0.8 to 51.0. New orders rose 0.7 to 55.7. Exports jumped 10.1 to 53.0. Sales dropped -2.6 to 45.0. Input prices rose 2.1 to 89.3. Selling prices rose 2.1 to 67.8. Average wages dropped -5.5 to 69.3.

Innes Willox, Chief Executive of Ai Group said: “Although input price pressures continued to accumulate, Australia’s manufacturing sector expanded again in June with solid increases in production and new orders and a slight lift in employment. While export sales were up, domestic sales fell reflecting the decline in consumer and business confidence in the face of concerns about inflation, interest rates and asset values. Selling prices were higher in June but by a smaller amount than input costs as less robust demand inhibited the ability of manufacturers to fully recover their higher costs in the market.”

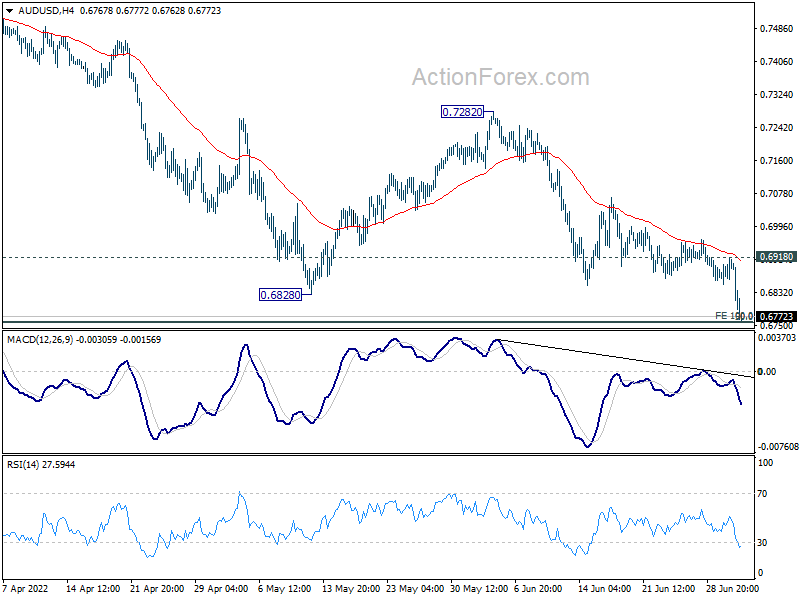

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6866; (P) 0.6893; (R1) 0.6931; More…

Intraday bias in AUD/USD stays on the downside with focus on 0.6756/60 cluster fibonacci level. Strong support is still expected there to bring rebound. Break of 0.6918 resistance will indicate short term bottoming and turn bias back to the downside. However, sustained break of 0.6756/60 will carry larger bearish implication and target 0.6461 fibonacci level next.

{kind=link}

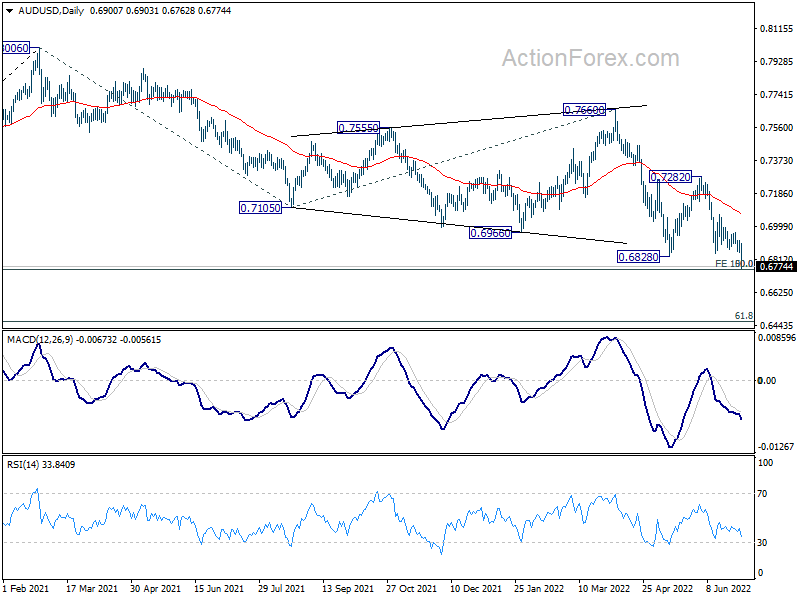

In the bigger picture, price actions from 0.8006 are seen as a corrective pattern to rise from 0.5506 (2020 low). Strong support is expected from 50% retracement of 0.5506 to 0.8006 at 0.6756 to complete the pattern. This coincides with 100% projection of 0.8006 to 0.7105 from 0.7660 at 0.6760. However firm break of 0.6756/60 will raise the chance of bearish reversal and target 61.8% retracement at 0.6461.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Mfg Index Jun | 54 | 52.4 | ||

| 22:45 | NZD | Building Permits M/M May | -0.50% | -8.50% | -8.60% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Jun | 2.10% | 2.10% | 0.90% | 1.90% |

| 23:30 | JPY | Unemployment Rate May | 2.60% | 2.50% | 2.50% | |

| 23:50 | JPY | Tankan Large Manufacturing Index Q2 | 9 | 13 | 14 | |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q2 | 10 | 14 | 9 | |

| 23:50 | JPY | Tankan Non – Manufacturing Index Q2 | 13 | 14 | 9 | |

| 23:50 | JPY | Tankan Non – Manufacturing Outlook Q2 | 13 | 17 | 7 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q2 | 18.60% | 8.90% | 2.20% | |

| 00:30 | JPY | Manufacturing PMI Jun F | 52.7 | 52.7 | 52.7 | |

| 01:45 | CNY | Caixin Manufacturing PMI Jun | 51.7 | 50.2 | 48.1 | |

| 07:30 | CHF | SVME PMI Jun | 59.1 | 57.3 | 60 | |

| 07:45 | EUR | Italy Manufacturing PMI Jun | 50.9 | 50.7 | 51.9 | |

| 07:50 | EUR | France Manufacturing PMI Jun F | 51.4 | 51 | 51 | |

| 07:55 | EUR | Germany Manufacturing PMI Jun F | 52 | 52 | 52 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Jun F | 52.1 | 52 | 52 | |

| 08:30 | GBP | Manufacturing PMI Jun F | 52.8 | 53.4 | 53.4 | |

| 08:30 | GBP | Mortgage Approvals May | 66K | 64K | 66K | |

| 08:30 | GBP | M4 Money Supply M/M May | 0.50% | 0.40% | 0.00% | |

| 09:00 | EUR | Eurozone CPI Y/Y Jun P | 8.60% | 8.30% | 8.10% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun P | 3.70% | 3.90% | 3.80% | |

| 13:45 | USD | Manufacturing PMI Jun F | 52.4 | 52.4 | ||

| 14:00 | USD | ISM Manufacturing PMI Jun | 55 | 56.1 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Jun | 80 | 82.2 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Jun | 49.6 | |||

| 14:00 | USD | Construction Spending M/M May | 0.40% | 0.20% |