Yen Selloff Resumes, RBNZ and BoC to Hike This Week

Yen’s selloff resumes in Asian session with USD/JPY making new recent high. The ruling coalition of Liberal Democratic Party and its junior partner Komeito scored a strong victory in Japan’s upper house elections. There might be sympathetic votes for the tragic death of former Prime Minister Shinzo Abe. But it’s also seen as a nod to Abe’s legacy on bringing Japan back as a “normal” country with stronger military and alliance with the US. Dollar is currently the stronger one, followed by Swiss Franc and then Kiwi. On the other hand, Aussie is the second weakest following Yen, followed by Sterling.

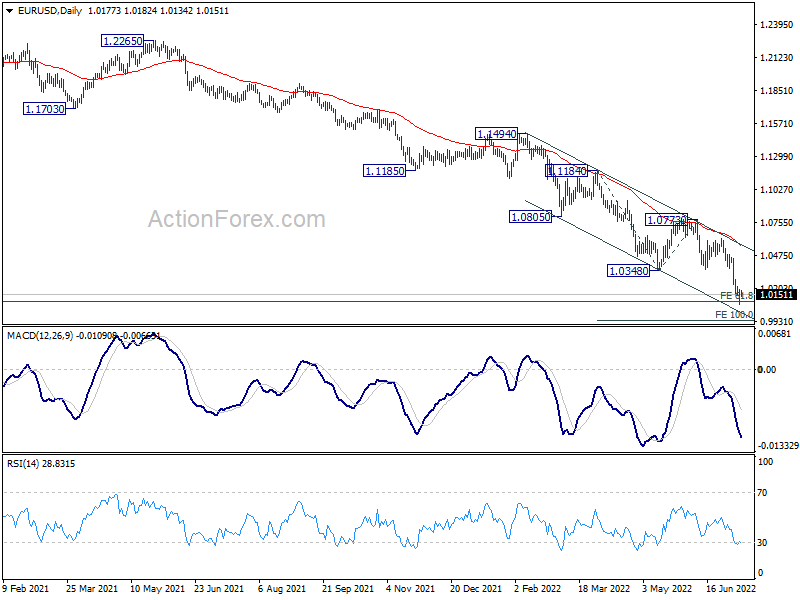

Technical, a major focus for the week is on whether EUR/USD’s down trend would pick up more momentum from the current level. The key level to watch is parity. Break of 1.0348 support turned resistance will be the first sign of stabilization, and bring consolidations. But sustained break of parity could prompt even deeper selloff, risking more downside acceleration.

{kind=link}

In Asia, at the time of writing, Nikkei is up 1.26%. Hong Kong HSI is down -2.74%. China Shanghai SSE is down -1.46%. Singapore Strait Times is up 0.06%. Japan 10-year JGB yield is down -0.005 at 0.246.

BoJ Kuroda: We won’t hesitate to take additional monetary easing steps as necessary

BoJ Governor Haruhiko Kuroda warned of the “very high uncertainty” on economic outlook due to surging commodity prices. While the economy is showing some signs of weakness, overall it’s still picking up as a trend.

“We won’t hesitate to take additional monetary easing steps as necessary,” he added, repeating that short- and long-term interest rate targets to “move at current or lower levels.”

Released from Japan, M2 rose 3.3% yoy in June versus expectation of 3.4% yoy. Machine orders dropped -5.6% mom in May, versus expectation of -5.5% mom.

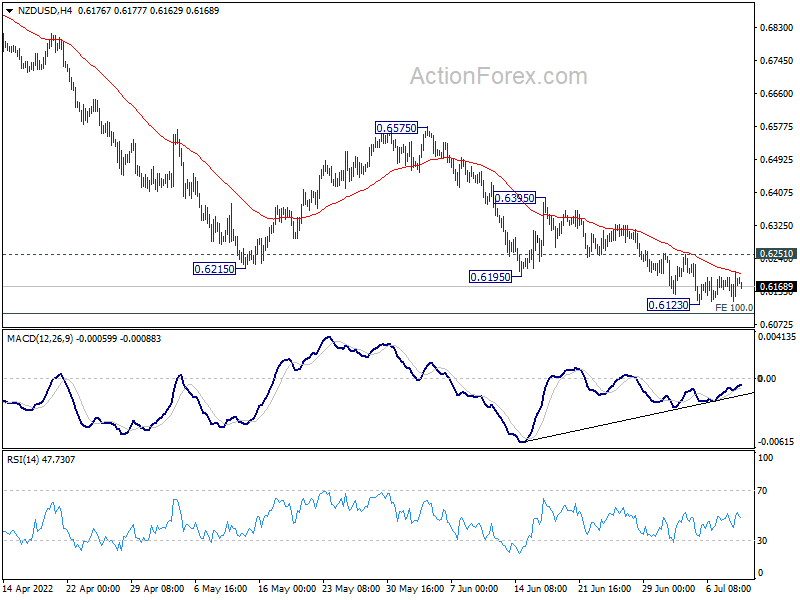

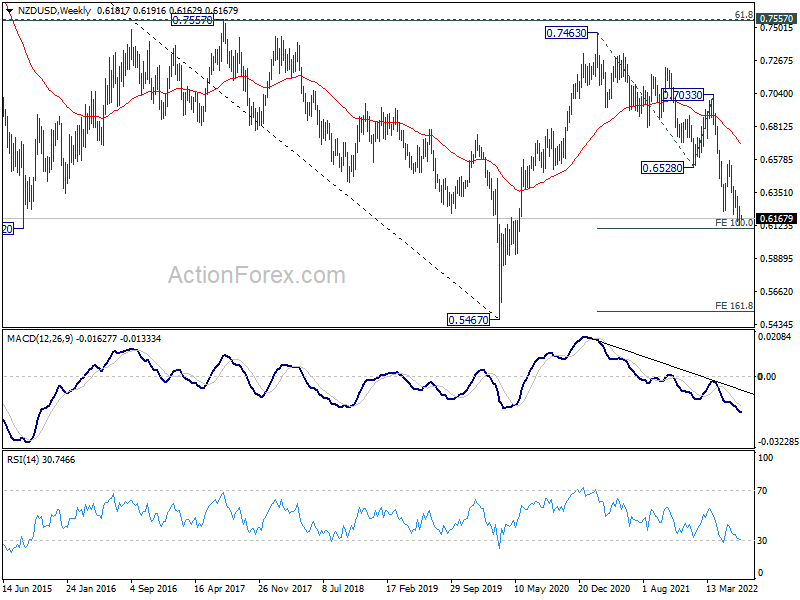

NZD/USD in tight range, eyeing support from 0.6098 projection level

NZD/USD is staying in tight range above 0.6123 temporary low, looking forward to RBNZ rate hike later in the week. There is prospect of a rebound from medium term projection level at 0.6098 (100% projection of 0.7463 to 0.6528 from 0.7033). But break of 0.6251 minor resistance is needed to be the first sign of bottoming, while firm break of 0.6395 resistance is needed to confirm. However, sustained break of 0.6098 would risk more downside acceleration to 161.% projection at 0.5520, which is close to 0.5467 (2020 low).

{kind=link}

{kind=link}

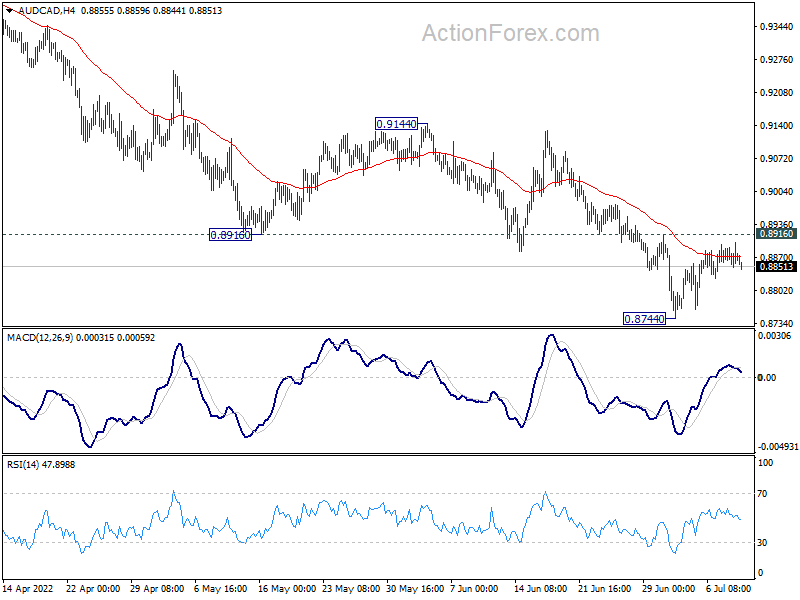

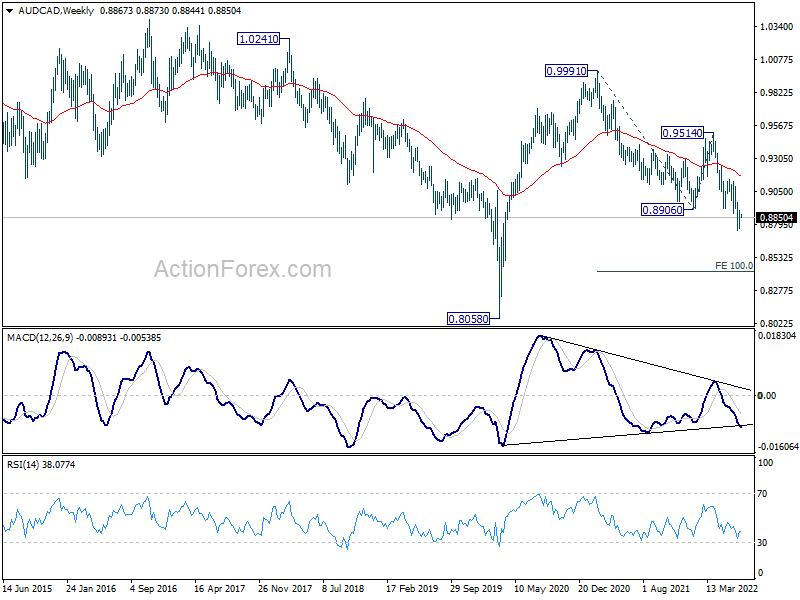

AUD/CAD staying in down trend, risks more downside

Canadian Dollar has been outperforming other commodity currencies recently and stays generally firm. There is prospect of further rally in the Loonie if BoC opts for a 75bps rate hike this week, instead of 50bps.

Looking at AUD/CAD, it’s staying well in the down trend from 0.9991 (2021 high). Outlook stays bearish as long as 0.8916 minor resistance holds. Break of 0.8744 temporary low will indicate down trend resumption. Next medium term target will be 100% projection of 0.9991 to 0.8906 from 0.9514 at 0.8429.

Nevertheless, firm break of 0.8916 will indicate short term bottoming and bring stronger rebound first.

{kind=link}

{kind=link}

RBNZ and BoC rate hike, US CPI and retail sales

Two central banks are expected to deliver rate hikes this week. RBNZ should raise the official cash rate by another 50bps to 2.50%. According to RBNZ’s own forecast variables in May, OCR could reach as high as 3.9% in Q2 2023, before gradually falling back in the second half of 2024. There is little that suggests RBNZ would deviate from is. So, a hawkish stance should be maintained.

Opinions on whether BoC would hike by 50bps or 75bps this week is divided. Governor Tiff Macklem noted back in June 9, “we may need to take more interest rate steps to get inflation back to target. Or we may need to move more quickly, we may need to take a larger step.” But ti’s unsure whether that would really translate into a larger hike this time. BoC will also publish new monetary policy report with economic projections.

On the data front, US CPI and retail sales will probably catch most attention. But attention will also be on Germany ZEW, UK GDP, and a batch of data from China, including trade balance, GDP, retail sales and industrial production. Here are some highlights for the week:

- Monday: Japan machine orders; Italy retail sales.

- Tuesday: Japan PPI; Australia Westpac consumer sentiment, NAB business confidence; Germany ZEW.

- Wednesday: RBNZ rate decision; China trade balance; Germany CPI final; UK GDP, productions, trade balance; Eurozone industrial production; US CPI; BoC rate decision; Fed’s Beige Book.

- Thursday: Australia inflation expectations, employment; Swiss PPI; Canada manufacturing sales; US PPI, jobless claims.

- Friday: New Zealand BusinessNZ manufacturing; China GDP, retail sales, industrial production, fixed asset investment; Japan tertiary industry index; Eurozone trade balance; Canada wholesales sales; US retail sales, Empire State manufacturing, import prices, industrial production, U of Michigan consumer sentiment, business inventories.

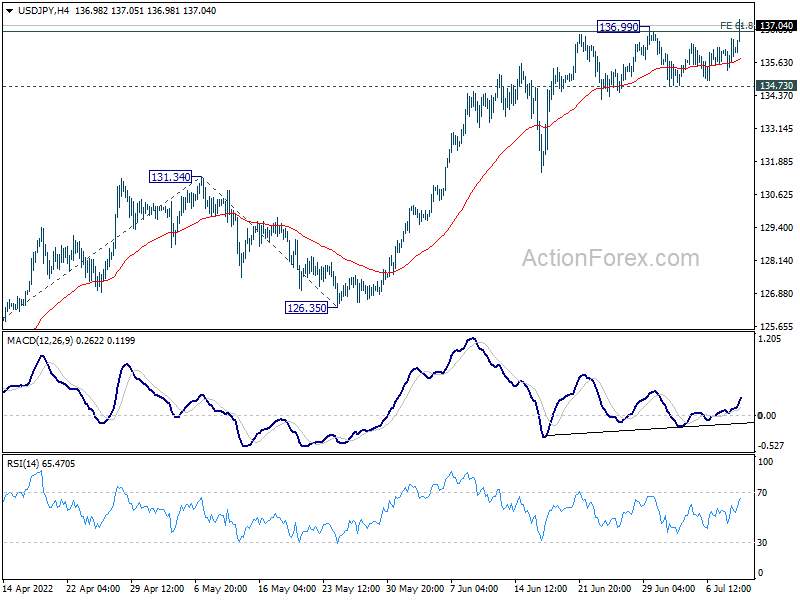

USD/JPY Daily Outlook

Daily Pivots: (S1) 135.42; (P) 136.00; (R1) 136.66; More…

Break of 136.99 suggests up trend resumption in USD/JPY and intraday bias is back on the upside. Sustained trading above 136.99 will confirm and target 100% projection of 114.40 to 131.34 from 126.35 at 143.29. For now, outlook will remain bullish as long as 134.73 support holds, in case of retreat.

{kind=link}

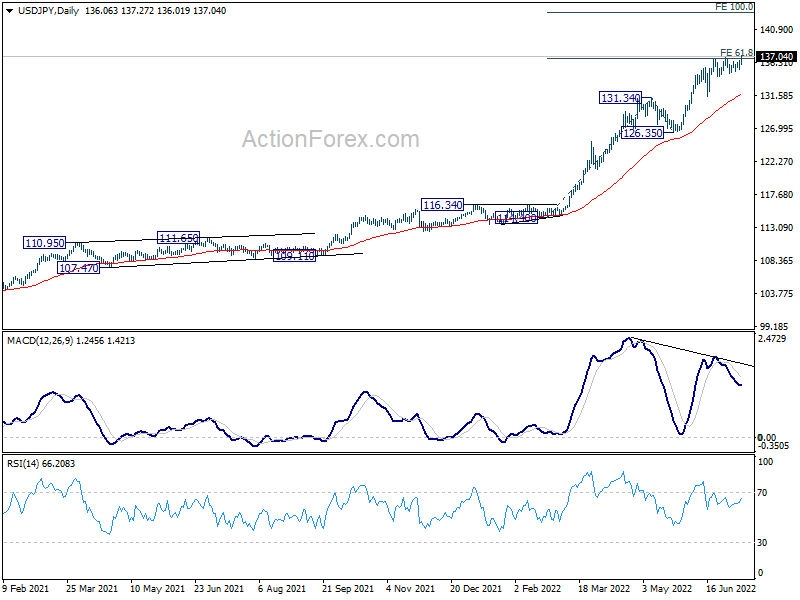

In the bigger picture, current rally is seen as part of the long term up trend from 75.56 (2011 low). Next target is 100% projection of 75.56 (2011 low) to 125.85 (2015 high) from 98.97 at 149.26, which is close to 147.68 (1998 high). This will remain the favored case as long as 126.35 support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y Jun | 3.30% | 3.40% | 3.20% | 3.10% |

| 23:50 | JPY | Machinery Orders M/M May | -5.60% | -5.50% | 10.80% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Jun P | 23.70% | |||

| 08:00 | EUR | Italy Retail Sales M/M May | 0.70% | 0.00% |