Kiwi and Aussie Jump on Improving Sentiment, Dollar Correction Continues

New Zealand and Australian Dollar trade broadly higher on the back on improving market sentiment. Asia indexes are tracking US stocks higher. On the other hand, Dollar continues to extend its near term correction, in particular against commodity currencies. Yen is also under some pressure. Meanwhile, European majors are mixed for now, waiting for UK inflation data today and ECB rate decision tomorrow.

Technically, DOW’s strong close overnight suggests that rebound from 29653.29 is ready to resume. Sustained trading above 55 day EMA (now at 31837.57) will add to the case that correction from 36952.65 is over. Further rise would then be seen back to 33272.34 resistance first, and break there will open up more rally back to 35392.22/36952.65 resistance zone. Such development could happen rather quickly. And, if happens, would add more fuel to the selloff in Dollar and Yen.

{kind=link}

In Asia, at the time of writing, Nikkei is up 2.55%. Hong Kong HSI is up 1.57%. China Shanghai SSE is up 0.75%. Singapore Strait Times is up 1.18%. Japan 10-year JGB yield is up 0.0048 at 0.247. Overnight, DOW rose 2.43%. S&P 500 rose 2.76%. NASDAQ rose 3.11%. 10-year yield rose 0.059 to 3.019.

RBA Lowe: Further increase in rates required over the month ahead

RBA Governor Philip Lowe said in a speech that the robust post-COVID recovery is “now behind us” given that inflation is high and labor market is very tight. RBA thus have withdrawn some emergency insurance and raised cash rate by 125bps over the past three meetings to 1.35%.

RBA “expects that further increase will be required over the months ahead”, to “help establish a more sustainable balance between demand and supply in the Australian economy.

Australia Westpac leading index dropped to 0.40%, economic slowdown ahead

Australia Westpac leading index dropped from 0.56% to 0.40% in June, indicating economic slowdown later in the year, but momentum is still above trend in the near term.

Westpac currently expects growth to slow from 4% in 2022 to 2% in 2023, but that is highly dependent on the profile of RBA’s tightening cycle.

Westpac expects RBA to opt for a fourth successive rate hike on August 2, and a third success time by 50bps. The current cycle is the first time cash rate has been lifted by 50bps or higher since 1990.

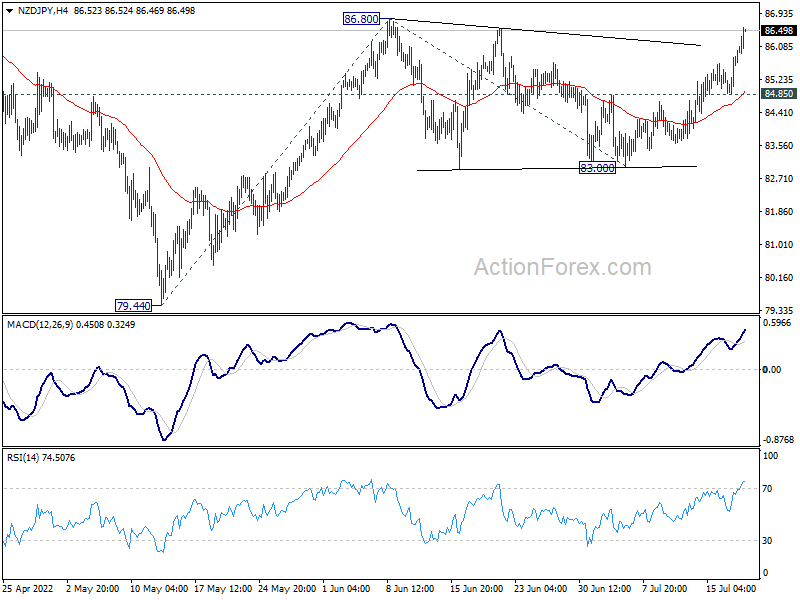

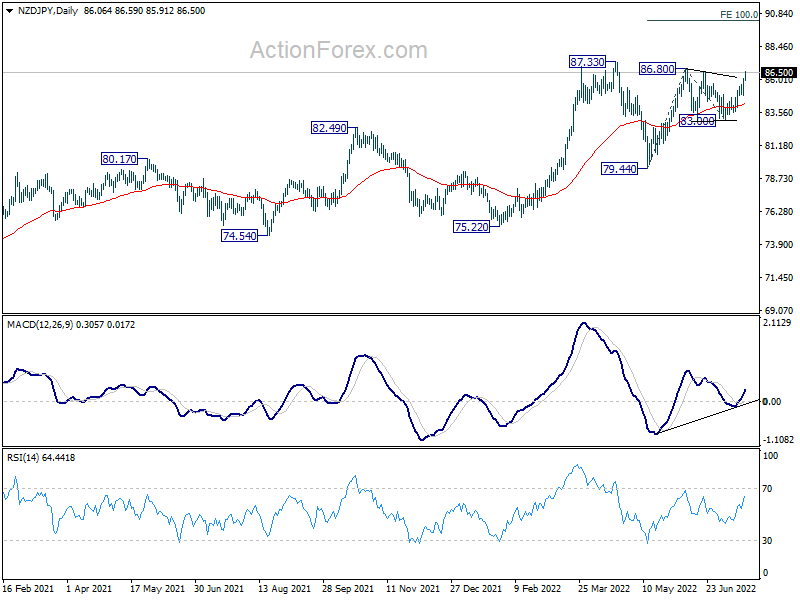

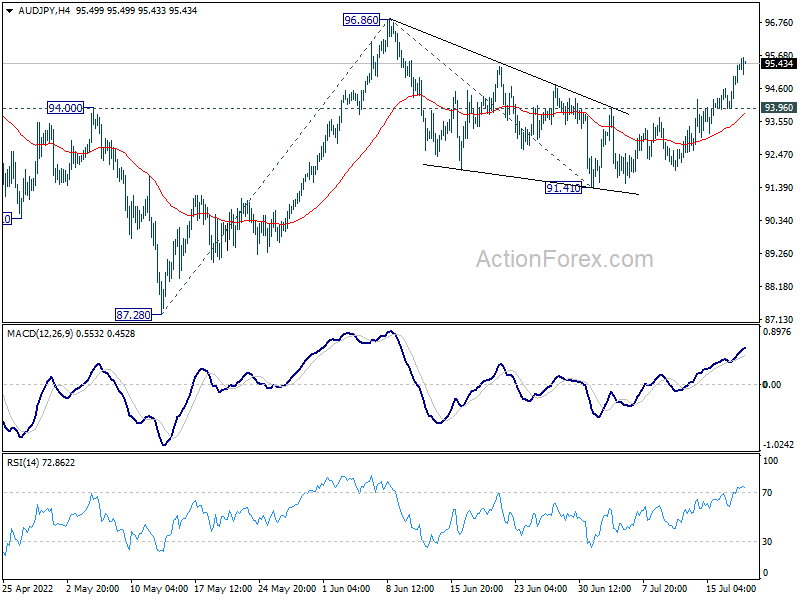

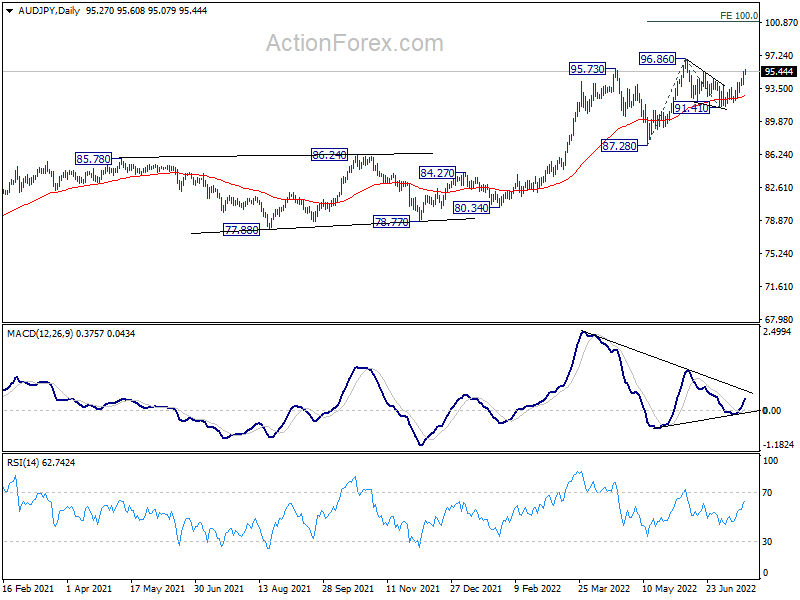

NZD/JPY ready for upside breakout, AUD/JPY to follow

Kiwi and Aussie are both trading broadly higher today, with help from improving market sentiment. Asian stocks are trading higher, following the strong rebound in US indexes overnight. Technically, speaking, NZD/JPY looks ready for an upside breakout, while AUD/JPY could follow soon.

NZD/JPY’s consolidation pattern from 86.80 should have completed 83.30, after struggling around 55 day EMA. Break of 86.80 resistance should send the cross through 87.33 high to resume larger up trend. Next target will be 100% projection of 79.44 to 86.80 from 83.00 at 90.36. But break of 84.85 will dampen this view and bring more corrective trading first.

{kind=link}

{kind=link}

AUD/JPY is lagging behind for now. But it’s also possible that corrective pattern from 96.86 is complete at 91.41. Further rise is in favor as long as 93.96 minor support holds. Break of 96.86 will confirm up trend resumption. Next target is 100% projection of 87.28 to 96.86 from 91.41 at 100.99.

{kind=link}

{kind=link}

Looking ahead

Inflation data are the main focuses for today. UK will publish CPI, RPI and PPI. Germany will release PPI. Eurozone will also release current account.

Later in the day, Canada CPI will take center stage, while IPPI and RMPI will be featured. US will release existing home sales.

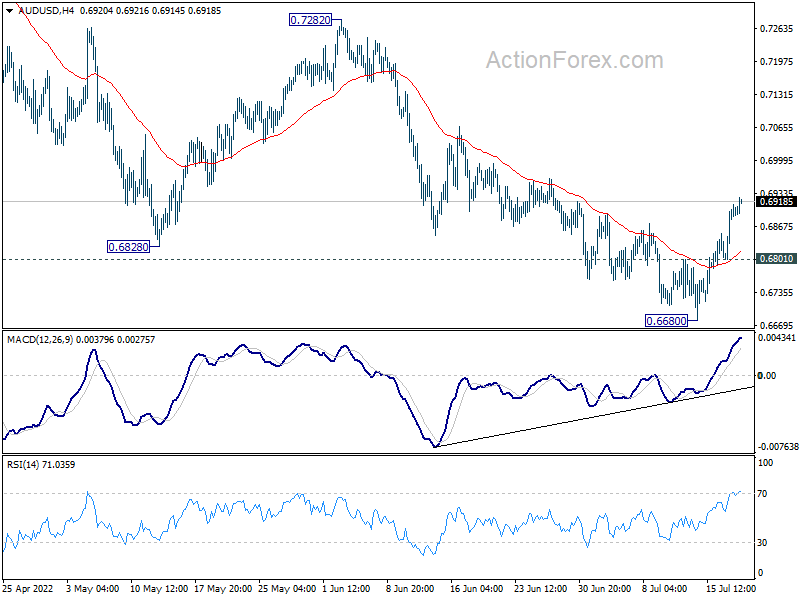

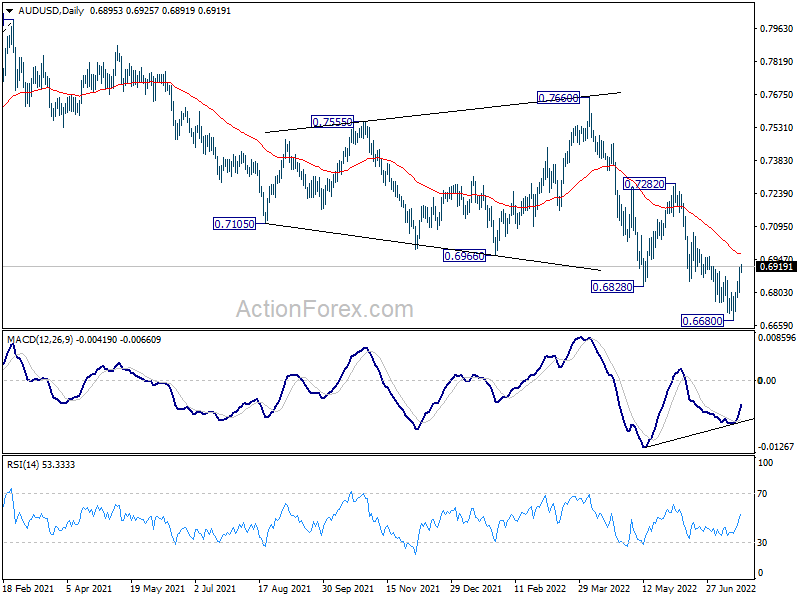

AUD/USD Daily Report

Daily Pivots: (S1) 0.6830; (P) 0.6872; (R1) 0.6940; More…

Intraday bias in AUD/USD remains on the upside, as rebound from 0.6680 short term bottom is in progress. Next target is 55 day EMA (now at 0.6973). Sustained break there will target 0.7282 structural resistance next. On the downside, however, below 0.6801 minor support will turn bias back to the downside for retesting 0.6680 low instead.

{kind=link}

In the bigger picture, price actions from 0.8006 could still be a corrective pattern to rise from 0.5506 (2020 low). But current downside acceleration is raising the chance that it’s a bearish impulsive move. In either case, outlook will remain bearish as long as 0.7282 resistance holds. Next target is 61.8% retracement of 0.5506 to 0.8006 at 0.6461.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Westpac Leading Index M/M Jun | -0.20% | -0.06% | ||

| 06:00 | EUR | Germany PPI M/M Jun | 1.00% | 1.60% | ||

| 06:00 | EUR | Germany PPI Y/Y Jun | 35.50% | 33.60% | ||

| 06:00 | GBP | CPI M/M Jun | 0.70% | 0.70% | ||

| 06:00 | GBP | CPI Y/Y Jun | 9.30% | 9.10% | ||

| 06:00 | GBP | Core CPI Y/Y Jun | 6.00% | 5.90% | ||

| 06:00 | GBP | RPI M/M Jun | 1.50% | 0.70% | ||

| 06:00 | GBP | RPI Y/Y Jun | 12.80% | 11.70% | ||

| 06:00 | GBP | PPI Input M/M Jun | 0.90% | 2.10% | ||

| 06:00 | GBP | PPI Input Y/Y Jun | 23.50% | 22.10% | ||

| 06:00 | GBP | PPI Output M/M Jun | 2.00% | 1.60% | ||

| 06:00 | GBP | PPI Output Y/Y Jun | 16.80% | 15.70% | ||

| 06:00 | GBP | PPI Core Output M/M Jun | 2.00% | 1.50% | ||

| 06:00 | GBP | PPI Core Output Y/Y Jun | 15.50% | 14.80% | ||

| 08:00 | EUR | Eurozone Current Account (EUR) May | -5.8B | |||

| 12:30 | CAD | Industrial Product Price M/M Jun | 2.60% | 1.70% | ||

| 12:30 | CAD | Raw Material Price Index Jun | 0.00% | 2.50% | ||

| 12:30 | CAD | CPI M/M Jun | 1.10% | 1.40% | ||

| 12:30 | CAD | CPI Y/Y Jun | 8.80% | 7.70% | ||

| 12:30 | CAD | CPI Common Y/Y Jun | 4.20% | 3.90% | ||

| 12:30 | CAD | CPI Median Y/Y Jun | 5.10% | 4.90% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Jun | 5.60% | 5.40% | ||

| 14:00 | USD | Existing Home Sales Jun | 5.40M | 5.41M | ||

| 14:00 | EUR | Eurozone Consumer Confidence Jul P | -25 | -23.6 | ||

| 14:30 | USD | Crude Oil Inventories | 2.1M | 3.3M |