All About Euro as ECB Rate Hike Awaited, BoJ Stands Pat

The forex markets are generally steady in Asian session today, with all major pairs and crosses stuck inside yesterday’s range. BoJ’s decision to stand pat on policy triggered little reaction. Instead, focus will turn to ECB, with main question on whether a 25bps hike will be delivered as pre-committed, or a bolder 50bps hike. As for the week, Aussie and Euro are currently the strongest ones while Dollar and Yen are the weakest, together with Swiss Franc. That’s a reflection on relatively positive market sentiment.

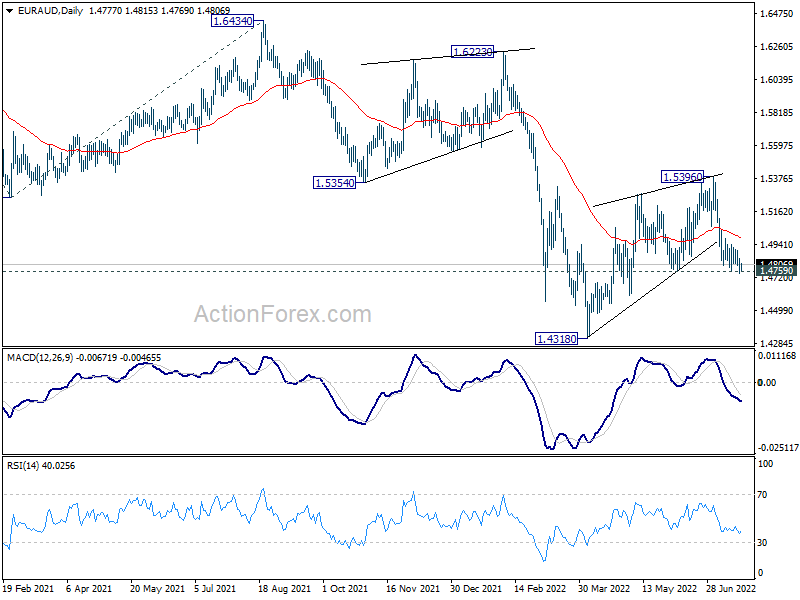

Technically, while both Euro and Aussie are firmer this week, Aussie is having a slight upper hand. Yet, it’s staying above 1.4759 minor support so far. It will be an interesting pair to watch today. Strong break of 1.4759 support will retain near term bearishness in EUR/AUD, and should send it through 1.4318 support to resume larger down trend. That could be a sign of come back of Euro bears, in particular against commodity currencies.

{kind=link}

In Asia, Nikkei closed up 0.44%. Hong Kong HSI is down -0.71%. China Shanghai SSE is down -0.40%. Singapore Strait Times is down -0.49%. Japan 10-year JGB yield is down -0.0049 at 0.239. Overnight, DOW rose 0.15%. S&P 500 rose 0.59%. NASDAQ rose 1.58%. 10-year yield rose 0.017 to 3.036.

BoJ stands part, downgrades 2022 growth forecasts, upgrades inflation

BoJ left monetary policy unchanged today as widely expected. Under the yield curve control frame work, short-term policy rate is held at -0.10%. BoJ will also will continue to purchase JGBs, without setting upper limit, to keep 10-year yield at around 0%. It will continue to offer to purchase 10-year JGBs at 0.25% yield every business day through fixed rate operations. Goushi Kataoka dissented again, pushing for further strengthening monetary easing.

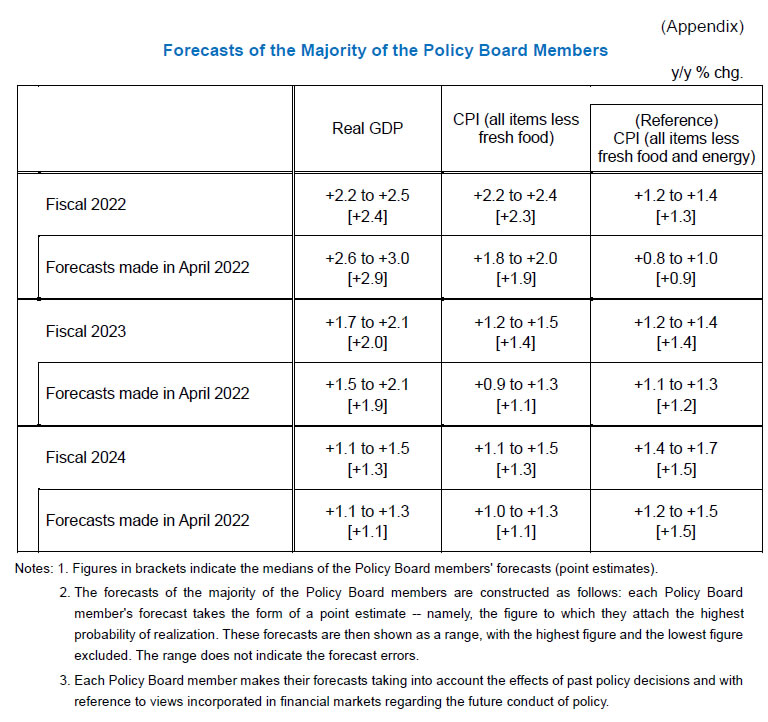

In the new economic projections, BoJ downgraded fiscal 2022 GDP forecasts, but upgraded both fiscal 2023 and 2024. CPI forecasts was upgraded across the horizon. Here are the new projections.

- Fiscal 2022 GDP growth at 2.4% (downgraded from April’s 2.9%).

- Fiscal 2023 GDP growth at 2.0% (up from 1.9%).

- Fiscal 2024 GDP growth at 1.3% (up from 1.1%).

- Fiscal 2022 CPI at 2.3% (up from 1.9%).

- Fiscal 2023 CPI at 1.4% (up from 1.1%).

- Fiscal 2024 CPI at 1.3% (up from 1.1%).

- Fiscal 2022 CPI core-core (ex-fresh food and energy) at 1.3% (up from 0.9%).

- Fiscal 2023 CPI core-core at 1.4% (up from 1.2%).

- Fiscal 2024 CPI core core at 1.5% (unchanged).

{kind=link}

New Zealand good imports jumped 25% yoy on petroleum, imports rose 7.7% yoy

New Zealand goods exports rose 7.7% yoy to NZD 6.4B in June. Goods imports rose 25.0% yoy to NZD 7.1B. Trade balance came in at NZD -701m deficit, versus expectation of NZD 204m surplus.

“Petroleum and products imports rose $795 million to reach a new high of $1.2 billion,” Stats NZ. “This rise lead the sharp increase in total imports for the month compared with June 2021.”

US leads monthly export rise, up 22%. Exports to EU were up 28% and Japan up 24%. Exports to China were down -6% and to Australia down -12%.

Import form all top partners rose, with China up 12%, EU up 11%, Australia up 6%, US up 30%, and Japan up 4.1%.

Australia NAB business condition rose to 20 in Q2, but confidence dropped to 5

Australia NAB quarterly business confidence dropped from 15 to 5 in Q2. Current business conditions rose from 11 to 20. Next 3 months business conditions was unchanged at 26. next 12 months business conditions dropped from 34 to 29. Capex plan for next 12 months dropped from 33 to 31.

Alan Oster, NAB Group Chief Economist, “Conditions strengthened in Q2 as the disruptions related to the virus receded. Trading, profitability, and employment were all higher with conditions approaching the high levels seen in early 2021.”

“Confidence eased in Q2, down to around long-run average levels,” said Oster. “That likely reflects the waning of some of the pandemic-recovery optimism, as well as the mounting challenges of rising inflation and also rising interest rates that businesses are confronting.”

ECB to hike by 25bps or 50bps? EUR/CHF to head back to parity?

ECB will finally raise interest rates for the first time in 11 years today. Opinions are divided on whether ECB would hike by 25bps as pre-committed, or opt for a larger 50bps hike this time. In addition to this question, markets will be eager to get any guidance for the size of hike in September, and any indication for October.

Here are some previews on ECB:

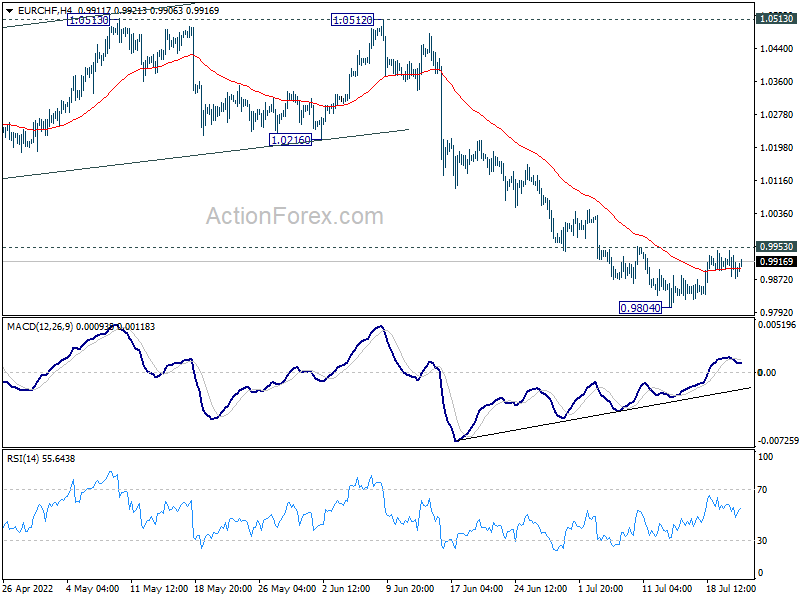

EUR/CHF is holding steady in range above 0.9804 temporary low. For now, outlook stays bearish with 0.9953 minor resistance intact. Downside breakout remains in favor. However, downside momentum has been clearly diminishing as seen in 4 hour MACD. Firm break of 0.9953 will bring stronger rebound back to 55 day EMA (now at 1.0109), that is, back above parity.

{kind=link}

{kind=link}

Elsewhere

Canada new housing price index will be released in US session. US will publish jobless claims and Philly Fed survey.

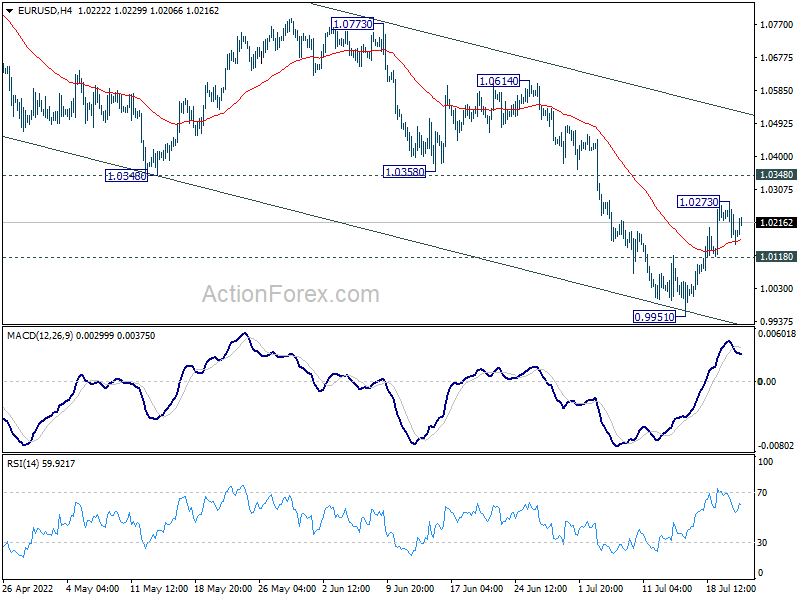

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0135; (P) 1.0204; (R1) 1.0252; More…

EUR/USD lost some upside momentum after hitting 1.0273 and intraday bias is turned neutral first. On the upside, above 1.0273 will resume the rebound form 0.9951 to 1.0348 support turned resistance, and then channel resistance at 1.0514. Nevertheless, break of 1.0118 minor support will argue that larger down trend is ready to resume, and should bring retest of 0.9951 low first.

{kind=link}

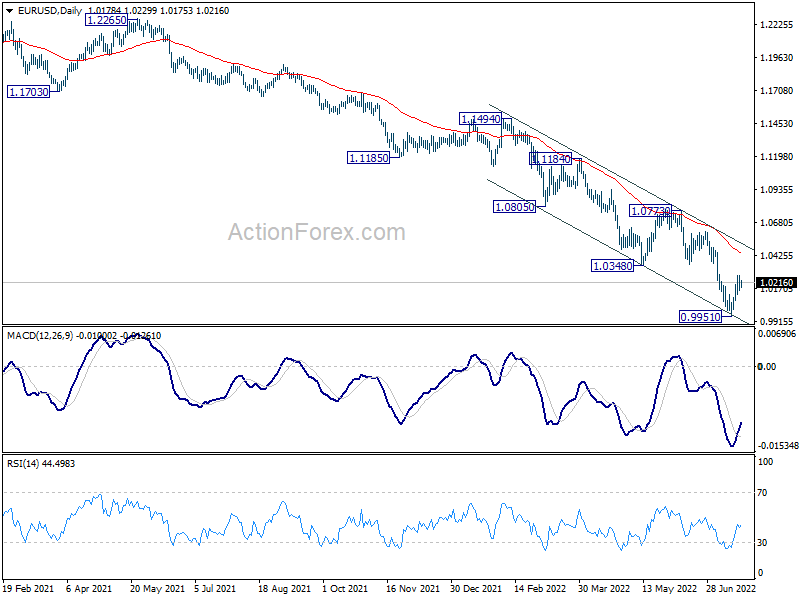

In the bigger picture, down trend from 1.6039 (2008 high) is still in progress. Next target is 100% projection of 1.3993 to 1.0339 from 1.2348 at 0.8694. In any case, outlook will stay bearish as long as 1.0773 resistance holds, in case of rebound.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Jun | -701M | 240M | 263M | 195M |

| 23:50 | JPY | Trade Balance (JPY) Jun | -1.93T | -2.01T | -1.93T | -1.89T |

| 01:30 | AUD | NAB Business Confidence Q2 | 5 | 14 | 15 | |

| 03:00 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Jun | 22.1B | 21.3B | 13.2B | 11.8B |

| 12:15 | EUR | ECB Interest Rate Decision | 0.25% | 0.00% | ||

| 12:30 | CAD | New Housing Price Index M/M Jun | 0.40% | 0.50% | ||

| 12:30 | USD | Initial Jobless Claims (Jul 15) | 240K | 244K | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Jul | -0.5 | -3.3 | ||

| 12:45 | EUR | ECB Press Conference | ||||

| 14:30 | USD | Natural Gas Storage | 45B | 58B |