Yen Surges With Falling Yields, Euro Hammered by Poor PMIs

Yen surges broadly today, together with Swiss Franc, following resumed decline in benchmark yields in US and Germany. Euro is sold off broadly, as the ECB lift faded, and as pressured by poor PMI data. Sterling is following as the second worst. Dollar is also weak on yields. For the week, Dollar is still the worst, followed by Sterling and Euro. Aussie is the best performer, followed by Kiwi. But Yen has the potential to catch up.

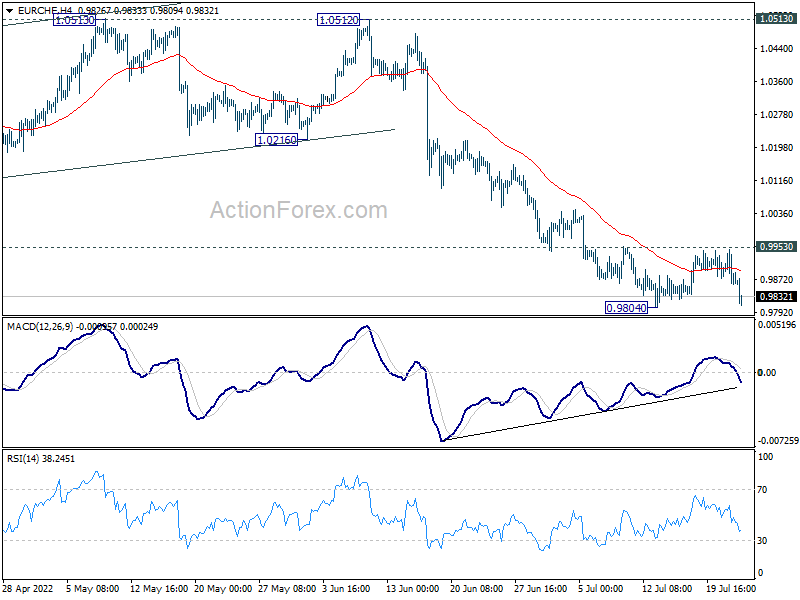

Technically, EUR/CHF will be a focus through the early half of next week. With 0.9953 minor resistance intact, outlook stays bearish. Firm break of 0.9804 will resume larger down trend. Such development, if happens, would be an indication of more broad based selloff in Euro.

{kind=link}

In Europe, at the time of the writing, FTSE is up 0.29%. DAX is up 0.56%. CAC is up 0.47%. Germany 10-year yield is down -0.1668 at 1.056. Earlier in Asia, Nikkei rose 0.40%. Hong Kong HSI rose 0.17%. China Shanghai SSE dropped -0.6%. Singapore Strait Times rose 0.92%. Japan 10-year JGB yield dropped -0.0269 at 0.214.

Canada retail sales rose 2.2% mom in May, and 0.3% mom in Jun

Canada retail sales rose 2.2% mom to CAD 62.2m in May, above expectation of 1.6% mom. That’s the fifth consecutive growth where sales were up in 8 of 11 subsectors. Excluding gasoline stations and motor vehicles and parts, sales rose 0.6% mom.

Statistics Canada estimated that sales increased 0.3% mom in June.

Eurozone PMI composite output dropped to 49.4, indicative of -0.1% quarterly GDP contraction

Eurozone PMI Manufacturing dropped from 52.1 to 49.6 in July, below expectation of 51.0. That’s the lowest level in 25 months. PMI Services dropped from 53.0 to 50.6, below expectation of 52.0. That’s the lowest level in 15 months. PMI Composite Output dropped from 52.0 to 49.4, a 17-month low.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said: “The eurozone economy looks set to contract in the third quarter as business activity slipped into decline in July and forward-looking indicators hint at worse to come in the months ahead…

“Excluding pandemic lockdown months, July’s contraction is the first signalled by the PMI since June 2013, indicative of the economy contracting at a 0.1% quarterly rate. Although only modest at present, a steep loss of new orders, falling backlogs of work and gloomier business expectations all point to the rate of decline gathering further momentum as the summer progresses…

“With the ECB raising interest rates at a time when the demand environment is one that would normally see policy being loosened, higher borrowing costs will inevitably add to recession risks.”

Germany PMI Manufacturing dropped from 52.0 to 49.2 in July, below expectation of 50.6. That’s the lowest level in 25 months. PMI Services dropped from 52.4 to 49.2, below expectation of 50.6. That’s the lowest level in 7 months. PMI Composite output dropped from 51.3 to 48.0, a 25- month low.

France PMI Manufacturing dropped from 51.4 to 49.6 in July, below expectation of 50.6. That’s the lowest level in 20 months. PMI Services dropped from 53.9 to 52.1, below expectation of 52.7. That’s the lowest level in 15 months. PMI Composite dropped from 52.5 to 50.6, a 16-month low.

ECB Villeroy: Starting rate hike faster does not mean ending higher

ECB Governing Council member Francois Villeroy de Galhau said today, “starting the increase in interest rates faster does not mean that (the cycle of increases) will end higher”.

Regarding the new Transmission Protection Instrument (TPI), Villeroy said, “if needed, we will be as determined in activating (the programme) as we have been in setting it up, and there are no pre-defined limits on the amount of possible purchases.”

Another Governing Council member Pablo Hernandez de Cos said the political crisis in Italy this week was not the reason behind the creation of anti-fragmentation tool. He added that the rate decision for September will be data-dependent.

Bundesbank: Germany inflation could rise again in September

Bundesbank said in its monthly report, “the German economy is likely to have stagnated in spring 2022.” High inflation is having a negative impact on the purchasing power of private households. Also, poor consumer mood due to the uncertainty about further economic development was noticeable in the sharp fall in sales in retail and vehicle trade

On prices, Bundesbank continues to expect high inflation rates in the coming months. Inflation could even rise again in September because the temporary relief measures will no longer apply. The further development of the energy commodity markets is very uncertain, especially with regard to natural gas deliveries from Russia. The risks for the price development are pointing upwards.

UK PMI composite output dropped to 17-mth low, growth slowed to a crawl

UK PMI Manufacturing dropped from 52.8 to 52.2 in July, above expectation of 52.0. that’s the lowest level in 24 months. PMI Services dropped from 54.3 to 53.3, above expectation of 53.2. That’s the lowest level in 17 months. PMI Composite dropped from 53.7 to 52.8, a 17-month low.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said: “UK economic growth slowed to a crawl in July, registering the slowest expansion since the lockdowns of early-2021. Although not yet in decline, with pent-up demand for vehicles and consumer-oriented services such as travel and tourism helping to sustain growth in July, the PMI is now at a level consistent with just 0.2% GDP growth….

“The concern is that rising interest rates, as the Bank of England seeks to control inflation, will cause demand growth to weaken further in the coming months. To be hiking interest rates at a time of such weak business growth is unprecedented over the past quarter-century of survey history.

UK retail sales down -0.1% mom, -5.8% yoy in volume; up 1.3% mom, 14.4 yoy in value

In volume term, UK retail sales dropped -0.1% mom in June, better than expectation of -0.3% mom. Ex-fuel sales rose 0.4% mom, above expectation of -0.3% mom.

Compared with the same period a year earlier, sales volume dropped -5.8% yoy, versus expectation of -5.3% yoy. Ex-fuel sales dropped -5.9% yoy, versus expectation of -6.2% yoy.

In value term, retail sales rose 1.3% mom, 14.4% yoy. Ex-fuel sales rose 1.3% mom, 12.9% yoy.

Japan CPI core ticked up to 2.2% yoy, core-core up to 1.0% yoy

Japan all-item CPI dropped from 2.5% yoy to 2.4% yoy in June. CPI core (all-items ex-fresh food), rose from 2.1% yoy to 2.2% yoy, matched expectations. CPI core-core (all-items ex-fresh food, energy) rose from 0.8% yoy to 1.0% yoy.

The CPI core reading has now stayed above BoJ’s 2% target for a third consecutive month. The core-core reading was also the strongest since February 2016.

BoJ left monetary policy unchanged yesterday. According to the new economic forecasts, core CPI will hit 2.3% this year, but then slowed back to 1.4% in fiscal 2023, and then 1.3% in fiscal 2024.

Japan PMI manufacturing dropped to 52.2 in July, services down to 51.2

Japan PMI Manufacturing dropped from 52.7 to 52.2 in July, below expectation of 53.1. PMI Services dropped from 54.0 to 51.2. PMI Composite output dropped from 53.0 to 50.6.

Usamah Bhatti, Economist at S&P Global Market Intelligence, said: “Flash PMI data indicated that activity at Japanese private sector businesses rose at a softer rate during July. The expansion in output was the softest recorded since March and only marginal as companies noted that shortages of raw materials and rising energy and wage costs had increasingly dampened output and new order inflows. This was notably evident at manufacturers, who recorded a reduction in production levels for the first time in five months. Service providers meanwhile reported the slowest rise in activity since April”.

Australia PMI composite dropped to 6-mnth low, further deceleration in growth

Australia PMI Manufacturing dropped from 56.2 to 55.7 in July. PMI Services dropped from 52.6 to 50.4, a 6-month low. PMI Composite dropped from 52.6 to 50.6, also a 6-month low.

Laura Denman, Economist at S&P Global Market Intelligence said: “Latest survey data has pointed to a further deceleration in the rate of private sector growth. Panellists suggested that interest rate increases, alongside persistent inflationary pressures, have been a pivotal factor contributing to the weakened private sector improvement this month. Further interest rate increases by Australia’s central bank present a downside risk to the private sector, with sentiment slipping to a 27-month low.”

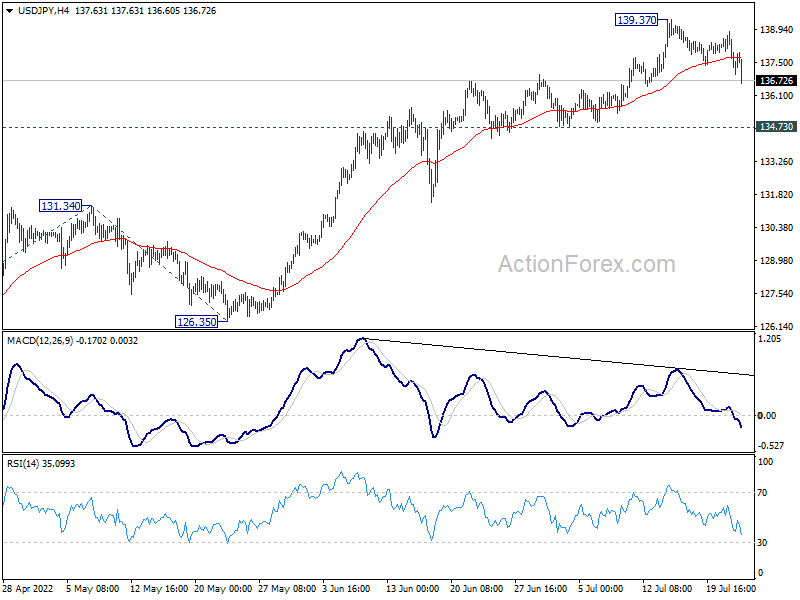

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 136.81; (P) 137.84; (R1) 138.39; More…

USD/JPY’s pull back from1 39.37 extends lower today and intraday bias stays neutral. Downside of retreat should be contained by 134.73 support. On the upside, break of 139.37 will resume larger up trend to 100% projection of 114.40 to 131.34 from 126.35 at 143.29.

{kind=link}

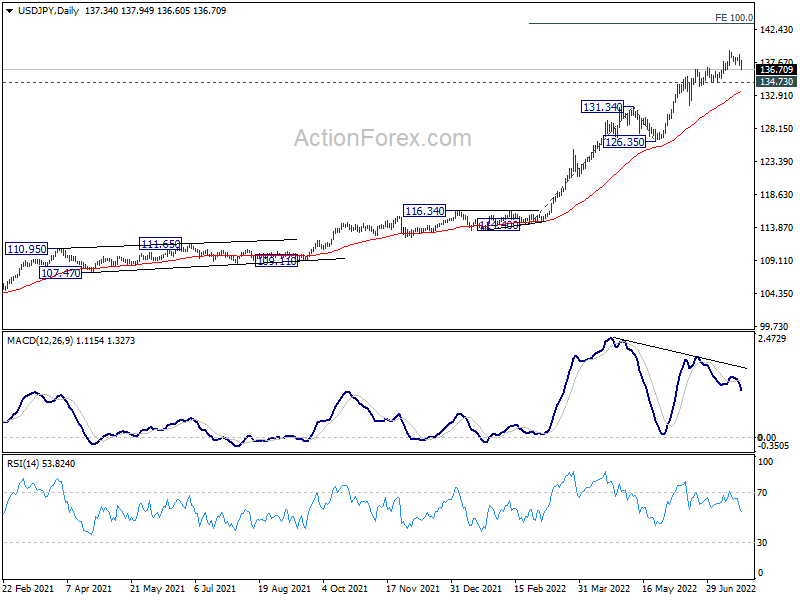

In the bigger picture, current rally is seen as part of the long term up trend from 75.56 (2011 low). Next target is 100% projection of 75.56 (2011 low) to 125.85 (2015 high) from 98.97 at 149.26, which is close to 147.68 (1998 high). This will remain the favored case as long as 126.35 support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI Jul P | 55.7 | 56.2 | ||

| 23:00 | AUD | Services PMI Jul P | 50.4 | 52.6 | ||

| 23:01 | GBP | GfK Consumer Confidence Jul | -41 | -42 | -41 | |

| 23:30 | JPY | National CPI Core Y/Y Jun | 2.20% | 2.20% | 2.10% | |

| 00:30 | JPY | Manufacturing PMI Jul P | 52.2 | 53.1 | 52.7 | |

| 06:00 | GBP | Retail Sales M/M Jun | -0.10% | -0.30% | -0.50% | |

| 06:00 | GBP | Retail Sales Y/Y Jun | -5.80% | -5.30% | -4.70% | |

| 06:00 | GBP | Retail Sales ex-Fuel M/M Jun | 0.40% | -0.30% | -0.70% | |

| 06:00 | GBP | Retail Sales ex-Fuel Y/Y Jun | -5.90% | -6.20% | -5.70% | |

| 07:15 | EUR | France Manufacturing PMI Jul P | 49.6 | 50.6 | 51.4 | |

| 07:15 | EUR | France Services PMI Jul P | 52.1 | 52.7 | 53.9 | |

| 07:30 | EUR | Germany Manufacturing PMI Jul P | 49.2 | 50.6 | 52 | |

| 07:30 | EUR | Germany Services PMI Jul P | 49.2 | 51.3 | 52.4 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Jul P | 49.6 | 51 | 52.1 | |

| 08:00 | EUR | Eurozone Services PMI Jul P | 50.6 | 52 | 53 | |

| 08:30 | GBP | Manufacturing PMI Jul P | 52.2 | 52 | 52.8 | |

| 08:30 | GBP | Services PMI Jul P | 53.3 | 53.2 | 54.3 | |

| 12:30 | CAD | Retail Sales M/M May | 2.20% | 1.60% | 0.90% | 0.70% |

| 12:30 | CAD | Retail Sales ex Autos M/M May | 1.90% | 1.80% | 1.30% | 1.10% |

| 13:45 | USD | Manufacturing PMI Jul P | 52.5 | 52.7 | ||

| 13:45 | USD | Services PMI Jul P | 52.1 | 52.7 |