Yen Rallies Further on Falling Yields, Dollar and Euro Weak

Yen’s rally intensified overnight and continues in Asian session. The move came in particular as US 10-year yield tumbled following the poor GDP report. For now, Dollar and Euro are the worst performing ones for the week, followed by Canadian. Sterling is following Yen as the second strongest and then Aussie. A large batch of economic data will be released today including GDP and inflation data from Eurozone, GDP from Canada and more inflation data from the US. These have the potential to solidify the current trends.

Technically, EUR/USD is so far very reluctant to breakout from range. An upside breakout is still mildly in favor, and break of 1.0277 minor resistance will target 1.0348 support turned resistance and above. But even it happens, such development is unlikely to help Euro elsewhere, and pairs like EUR/CHF, EUR/GBP, EUR/JPY and EUR/AUD should continue to stay pressured.

In Asia, Nikkei dropped -0.20%. Hong Kong HSI is down -2.25%. China Shanghai SSE is down -0.63%. Singapore Strait Times is down -0.52%. Japan 10-year JGB yield is down sharply by -0.035 at 0.178. Overnight, DOW rose 1.03%. S&P 500 rose 1.21%. NASDAQ rose 1.08%. 10-year yield dropped -0.053 to 2.681.

France GDP grew 0.5% qoq in Q2 on dynamism of exports

France GDP grew 0.5% qoq in Q2, better than expectation of 0.2% qoq.

Foreign trade contributed to +0.4 points to GDP growth this quarter, after +0.1 points in the previous quarter. This large contribution is due to the dynamism of exports (+0.8% after +1.6% in Q1 2022), coupled with the decline of imports (-0.6% after +1.2%).

The contribution of final domestic demand (excluding inventories) to GDP growth was null this quarter. Household consumption expenditure fell again, but more moderately than in the previous quarter (-0.2% after -1.3%). Gross fixed capital formation (GFCF) continued to grow at a rather vigorous pace (+0.5%, as in the previous quarter).

Finally, the contribution of inventory changes to GDP growth was weakly positive this quarter (+0.1 points after +0.2 points in Q1).

BoJ opinions: Appropriate to encourage wage increases through monetary easing

In the Summary of Opinions at BoJ’s July 20 and 21 meeting, it’s noted that, “Bank should support financing, mainly of firms, and maintain stability in financial markets, and should not hesitate to take additional easing measures if necessary.” Additionally, it is “appropriate for the Bank to maintain the current forward guidance for the policy rates.”

“While Japan’s economy is on its way to recovery from the pandemic, it has been under downward pressure due to an outflow of income from Japan caused by high commodity prices,” one member noted. “In this situation, it is appropriate that the Bank encourage wage increases through monetary easing, aiming to achieve the price stability target in a sustainable and stable manner”.

Japan industrial production rose record 8.9% mom in Jun, recovery to continue

Japan industrial production rose strongly by 8.9% mom in June, well above expectation of 3.7% mom. That’s also the biggest monthly rise since data become available in 2013. Car production jumped 14.0% mom thanks to easing of lockdowns in Shanghai of China. Manufacturers surveyed by the Ministry of Economy, Trade and Industry (METI) expected output to extend its recovery by 3.8% in July and 6.0% in August.

Also released, retail sales rose 1.5% yoy in June, below expectation of 2.8% yoy. Unemployment rate was unchanged at 2.6% in June. Housing starts dropped -2.2% yoy in June, versus expectation of -1.2% yoy. Consumer confidence dropped from 32.1 to 30.2 in July, below expectation of 33.0. Tokyo CPI core accelerated from 2.1% yoy to 2.3% yoy in July, above expectation of 2.2% yoy.

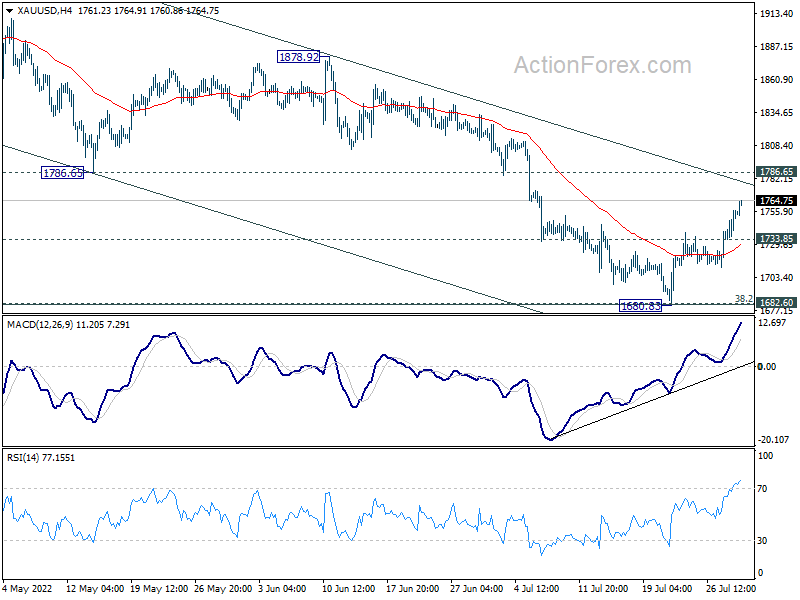

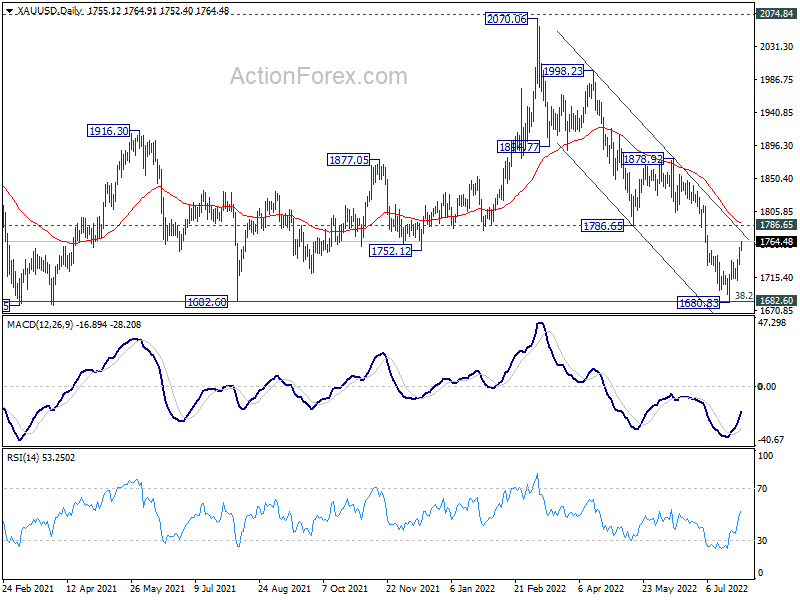

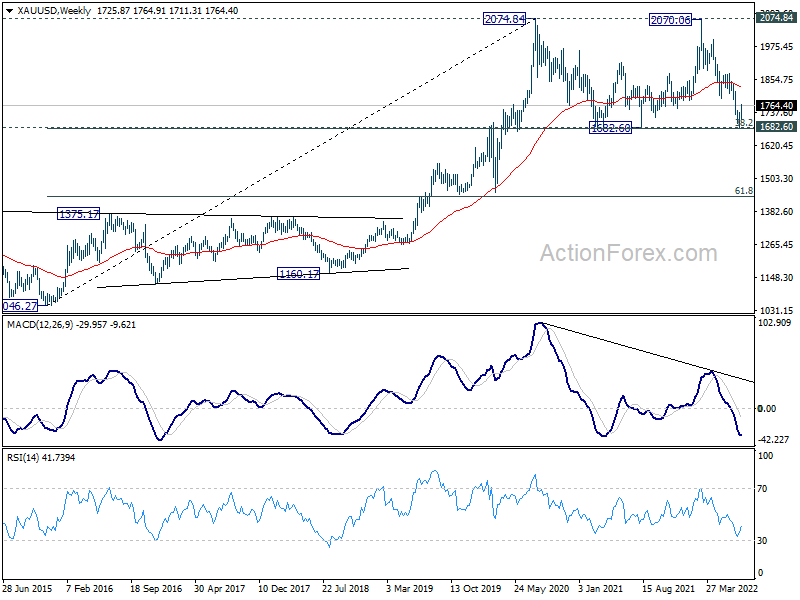

Gold tentatively bullish but 1800 region as key hurdle

Gold’s rebound from 1680.83 short term bottom picks up further momentum on broad based Dollar selling. Further rise is now expected as long as 1733.85 minor support holds, for channel resistance at 1778.91. But there are a couple of hurdles to overcome ahead, including, 1786.65 support turned resistance, 55 day EMA (now at 1791.10), 1800 psychological level, and 55 week EMA (now at 1831.13).

In the bigger picture, the view is unchanged that price actions from 2074.84 (2020 high) are in form of a three wave consolidation pattern, with fall from 2070.06 as the third leg. Strong support is expected at 1682.60, with 38.2% retracement of 1046.27 to 2074.84 at 1681.92, to complete the pattern. This is what has been happening so far. Sustained break of the above mentioned resistance zone between 1786.65 and 1831.13 will solidify this view and bring stronger rally back to retest 2074.84 high.

{kind=link}

{kind=link}

{kind=link}

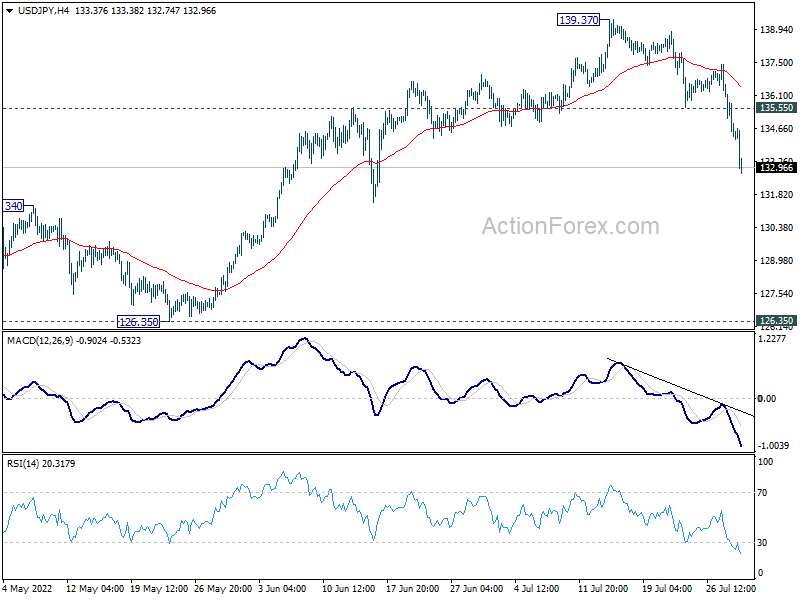

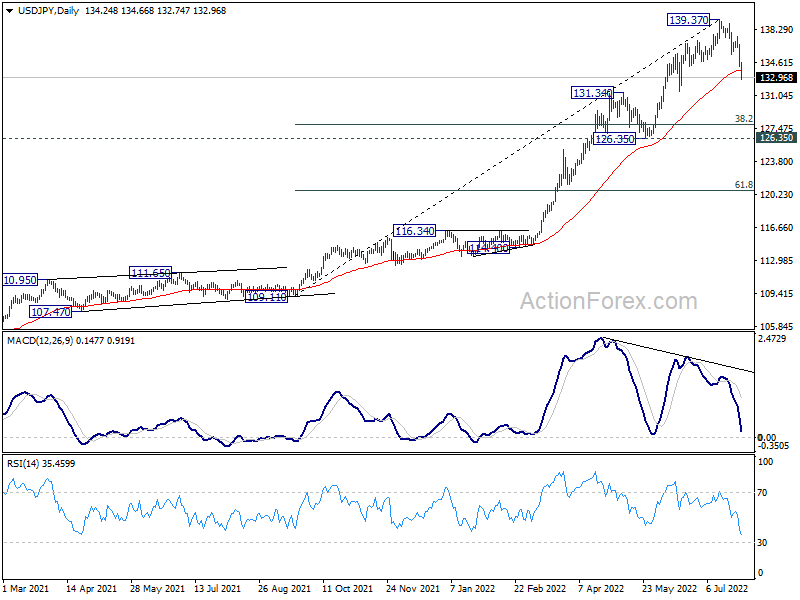

USD/JPY Daily Outlook

Daily Pivots: (S1) 133.42; (P) 135.02; (R1) 135.84; More…

USD/JPY’s decline from 139.37 medium term top continues today and hit as low as 132.74 so far. It’s now seen as in correction to medium term up trend. Intraday bias stays on the downside for 131.34 resistance turned support and below. But strong support is expected above 126.35 to contain downside, at least on first attempt, to bring rebound. But for now, risk will stay on the downside as long as 135.55 support turned resistance holds, in case of recovery.

{kind=link}

In the bigger picture, current rally is seen as part of the long term up trend from 75.56 (2011 low). Next target is 100% projection of 75.56 (2011 low) to 125.85 (2015 high) from 98.97 at 149.26, which is close to 147.68 (1998 high). This will remain the favored case as long as 126.35 support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Jul | 2.30% | 2.20% | 2.10% | |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 23:30 | JPY | Unemployment Rate Jun | 2.60% | 2.50% | 2.60% | |

| 23:50 | JPY | Industrial Production M/M Jun P | 8.90% | 3.70% | -7.50% | |

| 23:50 | JPY | Retail Trade Y/Y Jun | 1.50% | 2.80% | 3.60% | 3.70% |

| 01:30 | AUD | Private Sector Credit M/M Jun | 0.90% | 0.80% | 0.80% | |

| 01:30 | AUD | PPI Q/Q Q2 | 1.40% | 0.80% | 1.60% | |

| 01:30 | AUD | PPI Y/Y Q2 | 5.60% | 3.80% | 4.90% | |

| 05:00 | JPY | Housing Starts Y/Y Jun | -2.20% | -1.20% | -4.30% | |

| 05:00 | JPY | Consumer Confidence Index Jul | 30.2 | 33 | 32.1 | |

| 05:30 | EUR | France Consumer Spending M/M Jun | 0.20% | -1.00% | 0.70% | 0.40% |

| 05:30 | EUR | France GDP Q/Q Q2 P | 0.50% | 0.20% | -0.20% | |

| 06:00 | EUR | Germany Import Price Index M/M Jun | 1.00% | 0.80% | 0.90% | |

| 06:30 | CHF | Real Retail Sales Y/Y Jun | 1.40% | -1.60% | ||

| 07:00 | CHF | KOF Leading Indicator Jul | 95.2 | 96.9 | ||

| 07:55 | EUR | Germany Unemployment Rate Jul | 5.30% | 5.30% | ||

| 07:55 | EUR | Germany Unemployment Change Jul | 15K | 133K | ||

| 08:00 | EUR | Germany GDP Q/Q Q2 P | 0.10% | 0.20% | ||

| 08:00 | EUR | Italy GDP Q/Q Q2 P | 0.30% | 0.10% | ||

| 08:30 | GBP | Mortgage Approvals Jun | 64K | 66K | ||

| 08:30 | GBP | M4 Money Supply M/M Jun | 0.70% | 0.50% | ||

| 09:00 | EUR | Eurozone GDP Q/Q Q2 P | 0.10% | 0.60% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Jul P | 8.70% | 8.60% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Jul P | 3.80% | 3.70% | ||

| 12:30 | CAD | GDP M/M May | -0.20% | 0.30% | ||

| 12:30 | USD | Personal Income M/M Jun | 0.50% | 0.50% | ||

| 12:30 | USD | Personal Spending Jun | 0.90% | 0.20% | ||

| 12:30 | USD | PCE Price Index M/M Jun | 0.50% | 0.60% | ||

| 12:30 | USD | PCE Price Index Y/Y Jun | 6.70% | 6.30% | ||

| 12:30 | USD | PCE Core Price Index M/M Jun | 0.50% | 0.30% | ||

| 12:30 | USD | PCE Core Price Index Y/Y Jun | 4.70% | 4.70% | ||

| 12:30 | USD | Employment Cost Index Q2 | 1.20% | 1.40% | ||

| 13:45 | USD | Chicago PMI Jul | 56 | 56 | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Jul F | 51.1 | 51.1 |