Sterling Rises on PM Truss U-Turn Rumor

Sterling strengthens entering into European session, on rumors that UK Prime Minister Liz Truss to preparing to do a U-turn on tax and spending cuts. The talks came after Truss faced heavy scrutiny from Tory rebellions at the Conservative Party Conference. Markets are steady elsewhere, though. Traders are holding their bets for now, and await RBA and RBNZ rate hikes, as well as US heavy weight data in ISM and NFP later in the week.

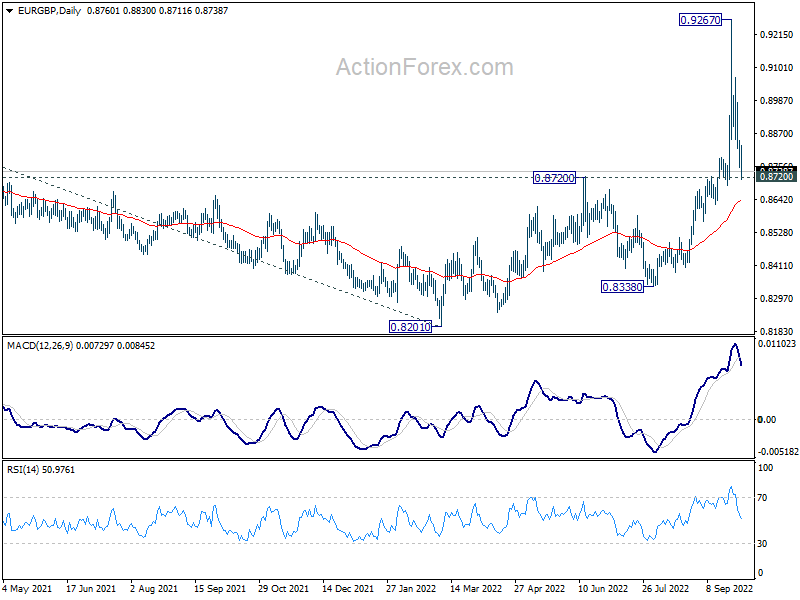

Technically, one immediate focus in EUR/GBP’s reaction to 0.8720 resistance turned support. Sustained break there will argue that rise from 0.8201 has completed at 0.9267 as a three-wave move. That would in turn argue that long term sideway pattern is extending with another falling leg. Deeper decline would be see to 55 day EMA (now at 0.8636) and below. Such development, if happens, would provide support the to Pound against other currencies.

{kind=link}

In Asia, Nikkei closed up 0.68%. Hong Kong HSI is down -1.27%. Singapore Strait Times is down -0.39%. Japan 10-year JGB yield is down -0.0091 at 0.243.

BoJ: Upside risks of inflation to be examined humbly and without any preconceptions

In the summary of opinions of BoJ’s September 21-22 meeting, it’s noted that risks of “consumer prices deviating significantly upward from the baseline scenario, including the impact of foreign exchange rates, needs to be examined humbly and without any preconceptions.”

But while a “certain degree of upside risk to prices” exists, there is a “long way to go” to achieve 2% inflation target in a “sustainable and stable manner”. Output gap has been “negative”, unemployment rate and active active job openings-to-applicants ratio “have not returned to pre-pandemic levels”. Surge in energy and raw material prices has brought about an “outflow of income” from Japan. It is “appropriate” to continue with the current monetary easing.

Regarding exchange rate, one opinion noted that ” further depreciation of the yen is partly due to differences in the direction of monetary policy between Japan and other economies.. the Bank needs to carefully explain the significance of continuing with the current monetary easing.”

Japan business outlook deteriorated in Q3

Japan Tankan large manufacturing index dropped from 9 to 8, below expectation of 11. That’s the third straight quarter of deterioration. Non-manufacturing index improve slightly from 13 to 14, above expectation of 13, and rise for the second straight quarter.

Large manufacturing outlook dropped from 10 to 9, below expectation of 11. Non-manufacturing outlook also deteriorated from 13 to 11, below expectation of 15.

Nevertheless, large companies are expected to increase capital expenditure by 21.5% in the current fiscal year ending March 2023, above expectation of 18.8%.

Meanwhile, companies expect inflation to hit 2.6% a year from now, and 2.1% three years ahead. Five years ahead inflation is also projected at 2.0%, highest since data became available in 2014.

Japan PMI manufacturing finalized at 50.8, weakness even turned worse

Japan PMI Manufacturing was finalized at 50.8 in September, down from August’s 51.5. S&P Global said high inflation and subdued global market conditions weight on order books. Output fell at sharpest pace in a year, while input buying reduced. Weak yen drove inflationary pressures higher.

Joe Hayes,, Senior Economist at S&P Global Market Intelligence, said: “Weakness in Japan’s manufacturing sector persisted in September and even turned worse. New orders fell at their sharpest rate in two years – high inflation is eroding client purchasing power, while slowing global economic growth is hurting exports. Weakness in the yen is doing little to bolster export demand either and instead is pushing imported inflation up drastically and drove domestic price pressures up even further.”

RBA and RBNZ to hike 50bps, US to release ISMs and NFP

Both RBA and RBNZ are expected to continue with tightening this week. RBA is expected to raise the cash rate by 50bps to 2.85%. Interest rate would then be at least in neutral region, if not restrictive. RBA might reinforce the signal that tightening pace would start to slow. RBNZ is also expected to hike by 50bps to 3.50%. Governor Adrian Orr has indicate that the tightening cycle is mature. Hence, there could be signals from RBNZ that the pace is going to slow ahead.

Other central bank activities include release of BoJ summary of opinions and ECB meeting accounts. Economic data events are also jam-packed, with biggest highlight in US ISMs and non-farm payroll employment.

Here are some highlights for the week:

- Monday: BoJ summary of opinions, Japan Tankan survey, PMI manufacturing final; Swiss CPI, PMI manufacturing; Eurozone PMI manufacturing final; UK PMI manufacturing final; Canada PMI manufacturing; US PMI manufacturing final, ISM manufacturing, construction spending.

- Tuesday: New Zealand NZIER business confidence; Australia AiG manufacturing, building approvals, RBA rate decision; Japan Tokyo CPI core, monetary base; Eurozone PPI; US factory orders.

- Wednesday: Australia retail sales; RBNZ rate decision; Germany trade balance; France industrial production; Eurozone PMI services final; UK PMI services final; Canada building permits, trade balance; US ADP employment, PMI services final, ISM services.

- Thursday: Australia AiG construction, trade balance; Germany factory orders; UK PMI construction; Eurozone retail sales, ECB meeting accounts; Canada Ivey PMI; US jobless claims.

- Friday: Japan average cash earnings, households spending, leading indicators; Germany import prices, industrial production, retail sales; France trade balance; Swiss foreign currency reserves; Italy retail sales; Canada employment; US non-farm payroll employment.

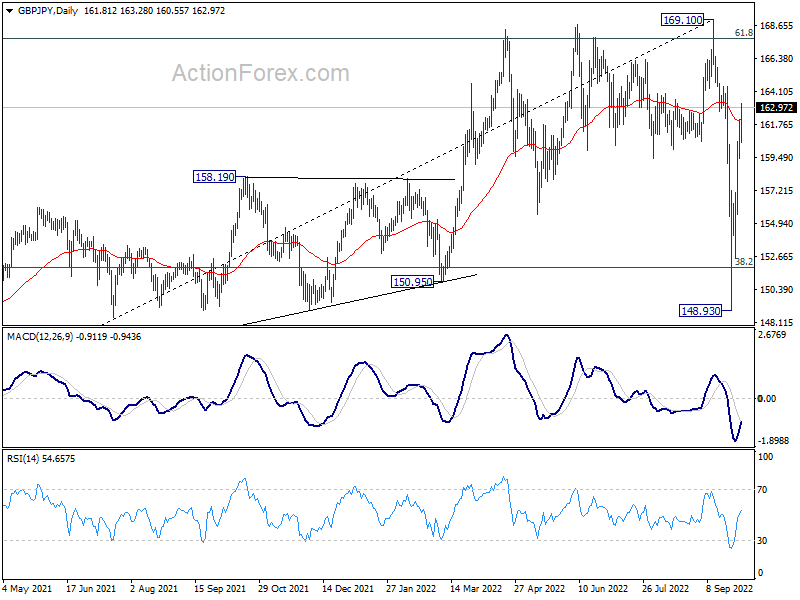

GBP/JPY Daily Outlook

Daily Pivots: (S1) 159.91; (P) 161.05; (R1) 162.65; More…

Intraday bias in GBP/JPY remains mildly on the upside as rebound from 148.93 extends higher. Further rally should be seen to retest 169.10 high. Strong resistance could be seen there to limit upside, at least on first attempt. On the downside, below 159.41 minor support will turn intraday bias neutral first.

{kind=link}

In the bigger picture, strong support from 38.2% retracement of 123.94 to 169.10 at 151.84 suggests that price actions from 169.10 are developing into a corrective pattern only. That is, rise from 123.94 (2020 low) should resume at a later stage. This will now remain the favored case as long as 148.93 support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Tankan Large Manufacturing Index Q3 | 8 | 11 | 9 | |

| 23:50 | JPY | Tankan Non-Manufacturing Index Q3 | 14 | 13 | 13 | |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q3 | 9 | 11 | 10 | |

| 23:50 | JPY | Tankan Non-Manufacturing Outlook Q3 | 11 | 15 | 13 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q3 | 21.50% | 18.80% | 18.60% | |

| 00:00 | AUD | TD Securities Inflation M/M Sep | 0.50% | -0.50% | ||

| 00:30 | JPY | Manufacturing PMI Sep F | 50.8 | 51 | 51 | |

| 06:30 | CHF | CPI M/M Sep | 0.10% | 0.30% | ||

| 06:30 | CHF | CPI Y/Y Sep | 3.50% | 3.50% | ||

| 07:30 | CHF | SVME PMI Sep | 54.6 | 56.4 | ||

| 07:45 | EUR | Italy Manufacturing PMI Sep | 47.5 | 48 | ||

| 07:50 | EUR | France Manufacturing PMI Sep F | 47.8 | 47.8 | ||

| 07:55 | EUR | Germany Manufacturing PMI Sep F | 48.3 | 48.3 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Sep F | 48.5 | 48.5 | ||

| 08:30 | GBP | Manufacturing PMI Sep | 48.5 | 48.5 | ||

| 13:30 | CAD | Manufacturing PMI Sep | 50.6 | 48.7 | ||

| 13:45 | USD | Manufacturing PMI Sep F | 51.8 | 51.8 | ||

| 14:00 | USD | ISM Manufacturing PMI Sep | 52.3 | 52.8 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Sep | 51.8 | 52.5 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Sep | 54.2 | |||

| 14:00 | USD | Construction Spending M/M Aug | -0.30% | -0.40% |