Dollar Selling Takes Off, EUR/USD Back Above Parity – Action Forex

Dollar’s decline takes off today on talks that poor economic data would prompt Fed to slow down the tightening pace sooner than earlier expected. Treasury yields also tumbled, adding some more weight to the greenback. Yet, it should be noted that inflation remains Fed’s biggest worry. There is little room for a pause if inflation plateaus at a high level. As for today, Australian Dollar is the strongest one, followed by Sterling, and Kiwi. Euro is back above pairty against the greenback. Swiss Franc is second worst, following Dollar, followed by Loonie. Canadian Dollar will look to BoC rate hike for some support.

Technically, current decline in 10-year yield is seen as a near term retreat for now. As long as 3.992 resistance turned support holds, things are disastrous. Another rally through 4.333 is expected and that would give the greenback a lift when happens. Nevertheless, considering bearish divergence condition in daily MACD, firm break of 3.992 would indicate that a larger correction is underway towards 55 day EMA (now at 3.614). But that might not happen before rate hike and statement next week.

In Europe, at the time of writing, FTSE is down -0.67%. DAX is up 0.06%. CAC is down -0.32%. Germany 10-year yield is up 0.006 at 2.181. Earlier in Asia, Nikkei rose 0.67%. Hong Kong HSI rose 1.00%. China Shanghai SSE rose 0.78%. Singapore Strait Times rose 0.81%. Japan 10-year JGB yield dropped -0.001 to 0.258.

IMF Georgieva urges patience as benefit of rates hikes not instantaneous

IMF Managing Director Kristalina Georgieva said that central banks should keep raising interest rates until they reach “neutral level”. “At this point we look for getting to a neutral mode, and in most places we are not quite yet there,” she added.

She explained that rates has to go up since “when inflation runs high, that undermines growth, it hits the poorest parts of the population the hardest.”

Georgieva also said “the benefits (of rate hikes) would come but they are not instantaneous, this requires some patience in society.” IMF projected that tightening will continue until 2024 when central banks are “seeing the impact of their actions”.

US goods trade deficit widened to USD 92.2B in Sep

US goods exports dropped USD -2.8B to USD 177.6B in September. Goods imports rose USD 2.2B to USD 269.8B. Trade deficit came in at USD -92.2B, larger than expectation of USD -87.8B.

Wholesale inventories rose 0.8% mom to USD 921.7B, below expectation of 1.3% mom. Retail inventories rose 0.4% mom to USD 744.0B.

Australia CPI jumped to 7.3% yoy in Q3, highest since 1990

Australia CPI rose 1.8% qoq in Q3, above expectation of 1.5% qoq. Annual rate accelerated from 6.1% yoy to 7.3% yoy, above expectation of 6.9% yoy. That’s the highest annual rise since 1990. Trimmed mean CPI, which excludes large price rises and falls, accelerated from 4.9% yoy to 6.1% yoy, highest since the data first published in 2003.

For the quarter, the most significant contributors to the rise were new dwellings (+3.7%), gas (+10.9%) and furniture (+6.6%). Annually, new dwellings (+20.7%) and automotive fuel (+18.0%) were the most significant contributors.

NZ ANZ business confidence fell to -42.7, murky outlook but resilient

New Zealand ANZ Business Confidence fell from -36.7 to -42.7 in October. Looking at some details, Own Activity Outlook dropped from -1.8 to -2.5. Cost expectations dropped from 89.8 to 88.6. Employment intentions dropped from 5.9 to 5.0. Price intentions dropped from 68.0 to 64.5. Inflation expectations rebounded from 5.98 to 6.13.

ANZ said: “The economic outlook is certainly murky, but the New Zealand economy has a lot going for it. Debt is higher, but nowhere near the worrying levels other economies are struggling under. We’re relatively insulated from the energy cost implications of Russia’s invasion of Ukraine. Our primary export base is food, and when it comes down to it, people gotta eat. Housing affordability has improved in a meaningful but so far remarkably painless fashion. Indeed, overall the economy is still surprising economists with its resilience. It’s a rougher path ahead, but the country is still moving forward.”

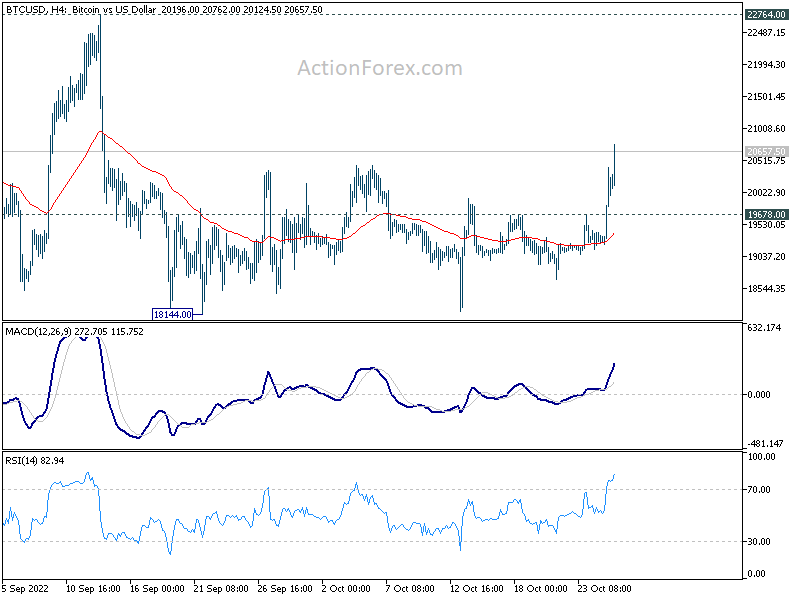

Bitcoin rises with Dollar selloff, heading to 22-23k?

Bitcoin rises notably today, following intensified selloff in Dollar in general. The break of 55 day EMA is a positive development for the near term. For now further rise expected as long as 19678 resistance turned support holds. Next target is 22764 resistance.

{kind=link}

As for the larger outlook, current rise from 18144 could either be the third leg of the consolidation pattern from 17575, or the start of an up trend. It’s too early to tell. Yet, a take on 25198 resistance is possible on break of 22764. The key resistance level is in 38.2% retracement of 48226 to 17575 at 29283. As long as this fibonacci level holds, medium term outlook will be neutral at best.

{kind=link}

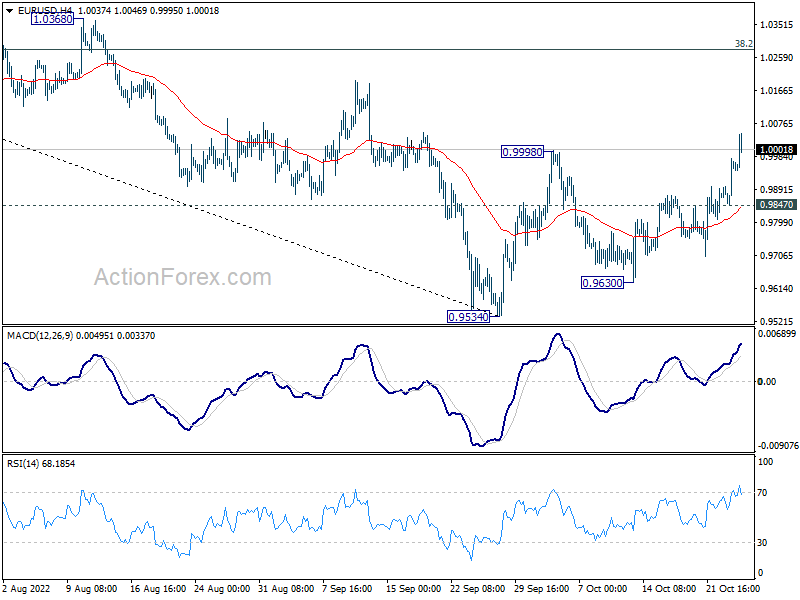

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 0.9886; (P) 0.9932; (R1) 1.0013; More…

EUR/USD’s rebound from 0.9534 resumed by breaking through 0.9988 resistance. The development also came with strong break of the medium term falling channel resistance, as well ass 55 day EMA. A medium term bottom could be in place already, on bullish convergence condition in daily MACD. Intraday bias is now on the upside for 38.2% retracement of 1.1494 to 0.9534 at 1.0283. On the downside, break of 0.9847 minor support will turn intraday bias neutral first.

{kind=link}

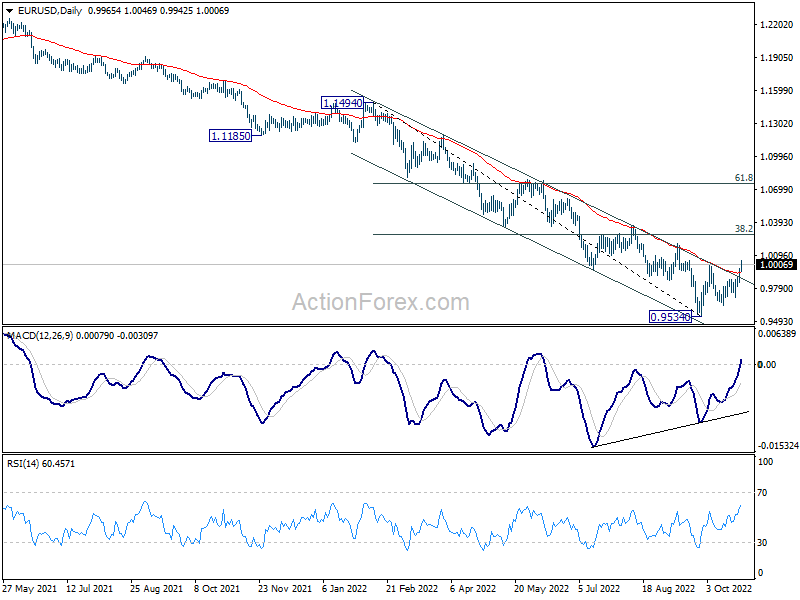

In the bigger picture, the case of medium term bottoming at 0.9534 building up. While it is too early to call for trend reversal, firm break of 0.9998 will open up stronger rebound back to 55 week EMA (now at 1.0630) even as a corrective rise. Meanwhile, firm break of 0.9534 will resume larger down trend to 100% projection of 1.3993 to 1.0339 from 1.2348 at 0.8694.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Sep | 2.10% | 1.80% | 1.90% | 2.00% |

| 00:00 | NZD | ANZ Business Confidence Oct | -42.7 | -36.7 | ||

| 00:30 | AUD | CPI Q/Q Q3 | 1.80% | 1.50% | 1.80% | |

| 00:30 | AUD | CPI Y/Y Q3 | 7.30% | 6.90% | 6.10% | |

| 00:30 | AUD | RBA Trimmed Mean CPI Q/Q Q3 | 1.80% | 1.50% | 1.50% | 1.60% |

| 00:30 | AUD | RBA Trimmed Mean CPI Y/Y Q3 | 6.10% | 5.60% | 4.90% | |

| 08:00 | CHF | Credit Suisse Economic Expectations Oct | -53.1 | -69.2 | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Sep | 6.30% | 6.10% | 6.10% | |

| 12:30 | USD | Goods Trade Balance (USD) Sep P | -92.2B | -87.8B | -87.3B | |

| 12:30 | USD | Wholesale Inventories Sep P | 0.80% | 1.30% | 1.30% | |

| 14:00 | USD | New Home Sales Sep | 590K | 685K | ||

| 14:00 | CAD | BoC Interest Rate Decision | 4.00% | 3.25% | ||

| 14:30 | USD | Crude Oil Inventories | -0.3M | -1.7M | ||

| 15:00 | CAD | BoC Press Conference |