Markets Tread Water ahead of Fed Hike and Guidance – Action Forex

The financial markets are all very steady today, awaiting FOMC rate decision. A 75bps hike a done deal, and the key is whether Fed Chair Jerome Powell would signal slower tightening pace ahead. For now, Dollar is the weaker one for today, followed by Euro and Sterling. On the other hand, Yen is the stronger one together with Aussie and Kiwi. But of course, such picture could change drastically after FOMC.

Post FOMC press conference market movements, in stocks, bonds and FX, should largely be driven by risk sentiment. AUD/USD has the potential to have larger moves than other Dollar pairs. Technically, break of 0.6355 minor support will signal that corrective rebound from 0.6169 has completed, and selloff could intensify through this low quickly. On the other hand, firm break of 0.6530 will add to the case of larger reversal, and bring stronger rise to 0.6698/6915 resistance zone.

In Europe, at the time of writing, FTSE is down -0.08%. DAX is flat. CAC is down -0.10%. Germany 10-year yield is up 0.016 at 2.147. Earlier in Asia, Nikkei dropped -0.06%. Hong Kong HSI rose 2.41%. China Shanghai SSE rose 1.15%. Singapore Strait Times rose 0.34%. Japan 10-year JGB yield dropped -0.0052 to 0.247.

US ADP employment grew 239k, strong but not broad-based

US ADP private employment grew 239k in October, above expectation of 198k. Goods-producing jobs decreased -8k but service-providing jobs increased 247k. By company size, small establishments added 25k jobs, medium added 218k, large lost -4k.

“This is a really strong number given the maturity of the economic recovery but the hiring was not broad-based,” said Nela Richardson, chief economist, ADP. “Goods producers, which are sensitive to interest rates, are pulling back, and job changers are commanding smaller pay gains. While we’re seeing early signs of Fed-driven demand destruction, it’s affecting only certain sectors of the labor market.”

Eurozone PMI manufacturing finalized at 46.4, moved into a deeper decline

Eurozone PMI Manufacturing was finalized at 46.4 in October, down from September’s 48.4. Manufacturing Output Index was finalized at 43.8, down from prior month’s 46.3. Both were the lowest reading in 29 months.

Looking at member countries, Ireland PMI manufacturing dropped to 51.4 (2-month low) but stayed in expansion. Greece (48.1, 22-month low), the Netherlands (47.9, 27-month low), France (47.2, 29-month low), Austria (46.6, 28-month low), Italy (46.5, 29-month low), Germany (45.1, 28-month low), and Spain (44.7, 29-month low) were all in contraction.

Joe Hayes, Senior Economist at S&P Global Market Intelligence said: “The eurozone goods-producing sector moved into a deeper decline at the start of the fourth quarter. The PMI surveys are now clearly signalling that the manufacturing economy is in a recession. In October, new orders fell at a rate we’ve rarely seen during 25 years of data collection – only during the worst months of the pandemic and in the height of the global financial crisis between 2008 and 2009 have decreases been stronger.”

Japan Suzuki concerned about gradual weakening of Yen

Japan Finance Minister Shunichi Suzuki told the parliament, “I am very concerned about the gradual weakening of the yen”, which could accelerate inflation by increasing import costs.

BoJ Governor Haruhiko Kuroda also said, recent Yen weakness raises uncertainty on the outlook, and is negative for the economy.

Regarding monetary policy, Kuroda said, “If the achievement of our 2% inflation target comes into sight, making yield curve control more flexible could become an option.” But for now, he added that the central bank must maintain ultra-low loose monetary policy to support the economy.

Australia AiG manufacturing fell to 49.6, longstanding supply-side problems continue

Australia AiG Performance of Manufacturing Index dropped -0.6 to 49.6 in October. Looking at some details, production dropped -0.1 to 47.6. Employment rose 7.1 to 46.9. New orders dropped -4.0 to 53.8. sales dropped -3.0 to 48.4. Input prices dropped -6.8 to 78.0. Selling prices dropped -2.7 to 67.5. Average wages dropped -5.1 to 71.0.

Innes Willox, Chief Executive of Ai Group said: “Australian manufacturing is in a holding pattern, with three straight months of flat results. Demand conditions in the market remain stable, but longstanding supply-side problems, such as labour and supply chain shortages, continue to drag on the industry.”

NZ unemployment rate unchanged at 3.3%, record hourly earning growth

New Zealand employment grew 1.3% in Q3, above expectation of 0.5%. Unemployment rate was unchanged at 3.3%, above expectation of 3.2%. Labor force participation rate rose 0.8% to 71.7%. Underutilization rate dropped -0.2 to 9.0%.

Average ordinary time hourly earnings rose 2.4% qoq, 7.4% yoy. The annual rise was the highest since the series began in 1989. All salary and wage rates (including overtime) index rose 3.7% yoy, second highest annual rate since record began in 1993.

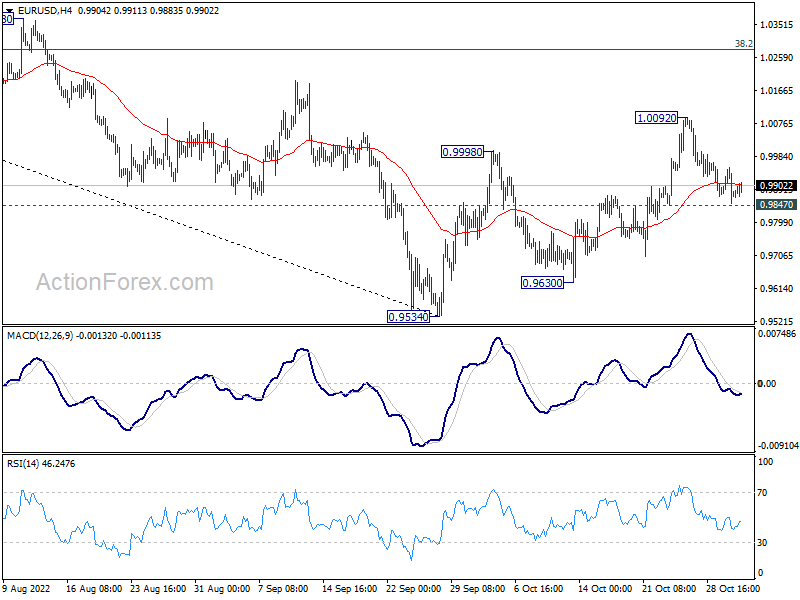

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 0.9833; (P) 0.9894; (R1) 0.9934; More…

EUR/USD is staying in range of 0.9847/1.0092 and intraday bias remains neutral. Further rise is in favor as long as 0.9847 minor support holds. Break of 1.0092 will target 38.2% retracement of 1.1494 to 0.9534 at 1.0283. However, break of 0.9847 will turn bias back to the downside for 0.9534/9630 support zone instead.

{kind=link}

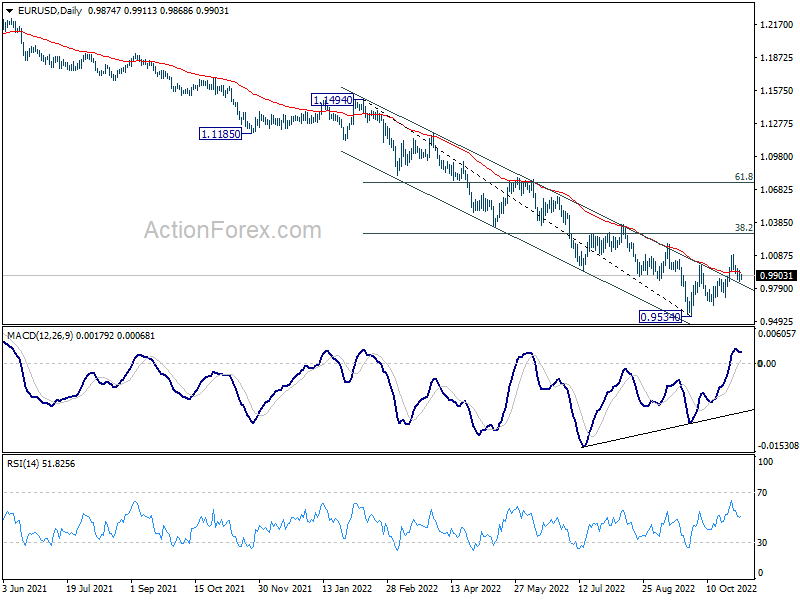

In the bigger picture, the case of medium term bottoming at 0.9534 building up, with bullish convergence condition in daily MACD. While it is too early to call for trend reversal, firm break of 0.9998 opens up stronger rebound back to 55 week EMA (now at 1.0630) even as a corrective rise. However, sustained trading back below 55 day EMA (now at 0.9938) will revive medium term bearishness for another fall through 0.9534 low.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Mfg Index Oct | 49.6 | 50.2 | ||

| 21:45 | NZD | Employment Change Q3 | 1.30% | 0.50% | 0.00% | |

| 21:45 | NZD | Unemployment Rate Q3 | 3.30% | 3.20% | 3.30% | |

| 21:45 | NZD | Labour Cost Index Q/Q Q3 | 1.10% | 1.00% | 1.30% | |

| 23:50 | JPY | Monetary Base Y/Y Oct | -6.90% | -2.00% | -3.30% | |

| 23:50 | JPY | BoJ Minutes | ||||

| 00:01 | GBP | BRC Shop Price Index Y/Y Sep | 6.60% | 5.50% | 5.70% | |

| 00:30 | AUD | Building Permits M/M Sep | -5.80% | -9.00% | 28.10% | 23.10% |

| 07:00 | EUR | Germany Trade Balance (EUR) Sep | 3.7B | 0.5B | 1.2B | |

| 08:45 | EUR | Italy Manufacturing PMI Oct | 46.5 | 46.9 | 48.3 | |

| 08:50 | EUR | France Manufacturing PMI Oct F | 47.2 | 47.4 | 47.4 | |

| 08:55 | EUR | Germany Unemployment Change Oct | 8K | 15K | 14K | |

| 08:55 | EUR | Germany Unemployment Rate Oct | 5.50% | 5.50% | 5.50% | |

| 08:55 | EUR | Germany Manufacturing PMI Oct F | 45.1 | 45.7 | 45.7 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Oct | 46.4 | 46.6 | 46.6 | |

| 12:15 | USD | ADP Employment Change Oct | 239K | 198K | 208K | 192K |

| 14:30 | USD | Crude Oil Inventories | -0.2M | 2.6M | ||

| 18:00 | USD | Fed Interest Rate Decision | 4.00% | 3.25% | ||

| 18:30 | USD | FOMC Press Conference |