Sterling and Loonie Shrug Inflation Data, Markets Tread Water – Action Forex

The financial markets are generally quiet today, with European indexes and US futures trading slightly lower into US session. In the currency markets, most major pairs and crosses are stuck inside yesterday’s range, with Yen and Dollar on the softer side, Euro and Swiss Franc on the firmer side. Sterling and Canadian Shrug respecting inflation data. Aussie and Kiwi are mixed.

Technically, while Dollar’s selloff might have lost momentum, it’s far too early to call for a reversal. Levels to note included 1.0092 support in EUR/USD, 0.6521 support in AUD/USD, 0.9680 minor resistance in USD/CHF and 1.3494 resistance in USD/CAD. As long as these level holds, near term sentiment is still against the greenback.

In Europe, at the time of writing, FTSE is down -0.16%. DAX is down -0.83%. CAC is down -0.39%. Germany 10-year yield is down -0.079 at 2.034. Earlier in Asia, Nikkei rose 0.14$. Hong Kong HSI dropped -0.47%. China Shanghai SSE dropped -0.45%. Singapore Strait Times dropped -0.28%. Japan 10-year JGB yield rose 0.0014 to 0.244.

US retail sales rose 1.3% mom in Oct, ex-auto sales up 1.3% mom

US retail sales rose 1.3% mom to USD 694.5B in October, above expectation of 0.9% mom. Ex-auto sales rose 1.3% mom, above expectation of 0.4% mom to USD 565.1B. Ex-gasoline sales rose 1.0% mom to USD 630.4B.

Comparing with October 2021, total sales were up 8.3% yoy. Total sales in the three months through October were up 8.9% yoy.

Fed George: Maybe we even have economic contraction to slow inflation

Kansas City Fed President Esther George told the WSJ, “‘I have not in my 40 years with the Fed seen a time of this kind of tightening that you didn’t get some painful outcomes”.

“I’m looking at a labor market that is so tight, I don’t know how you continue to bring this level of inflation down without having some real slowing, and maybe we even have contraction in the economy to get there.”

Canada CPI unchanged at 6.9% yoy in Oct

Canada CPI was unchanged at 6.9% yoy in October, slightly below expectation of 7.0% yoy. Excluding food and energy, prices slowed slightly from 5.4% to 5.3% yoy.

On a monthly basis, CPI rose 0.7% mom, below expectation of 0.8% mom, largely driven by the 9.2% mom rise in prices for gasoline.

Comparing to 5.6% you rise in average hourly wages, on average, prices rose faster than wages.

ECB de Guindos: Will discuss balance sheet reduction in December

ECB Vice President Luis de Guindos said, “we will discuss about the reduction of our balance sheet,” at December meeting.

“I think this is important in terms of both to reduce the excess liquidity that we see in the marketplace, and secondly as well to alleviate the situation of scarcity of collateral,” he added.

De Guindos also noted, “it’s very difficult to have financial stability without price stability,” adding that “the main risk now for financial stability, for growth, is to have inflation at very high levels.”

UK CPI accelerated further to 11.1% yoy in Oct despite energy price guarantee

UK CPI accelerated from 10.1% yoy to 11.1% yoy in October, above expectation of 10.6% yoy. That’s highest level since 1981 based on modelled data. Core CPI was unchanged at 6.5% yoy, above expectation of 6.4% yoy.

ONS said, “Despite the introduction of the government’s Energy Price Guarantee, gas and electricity prices made the largest upward contribution to the change in both the CPIH and CPI annual inflation rates between September and October 2022.”

“Rising food prices also made a large upward contribution to change with transport (principally motor fuels and second-hand car prices) making the largest, partially offsetting, downward contribution to the change in the rates.”

Also released, PPI input came in at 0.6% mom, 19.2% yoy, versus expectation of 1.0% mom, 17.7% yoy. PPI output was at 0.3% mom, 14.8% yoy, versus expectation of 0.0% mom, 14.8% yoy. PPI core output was at 0.5% mom, 13.3% yoy, versus expectation of 1.3% mom, 14.0% yoy.

Japan machine orders dropped -4.6% mom in Sep

Japan private-sector machine orders dropped sharply by -4.6% mom in September, much worse than expectation of 0.7% mom. That followed a -5.8% mom decline in August.

Nevertheless, for October-December period, manufacturers surveyed by the Cabinet Office are expecting core orders to rise 3.6%.

The government also downgraded its view on machinery orders to “recovery is stalling”, from “economy was picking up”.

Australia Westpac leading index signals sustained weak growth next year

Australia Westpac Leading Index dropped from -1.09% to -1.19% in October, a new post-pandemic low. Westpac said the is consistent with “sustained weak growth” in 2023. It expects GDP growth to slow from around 3.4% in 2022 to just 1% next year.

It added, “key drivers of the slowdown are: monetary policy tightening; falling commodity prices; and softness in jobs growth as capacity constraints bite.”

Regarding RBA policy, Westpac expects another 25bps rate hike at the December 6 meeting. And, “a mooted pause in the tightening is unlikely to occur in 2022 or the early months of 2023 as the Bank continues to underperform its inflation objectives.”

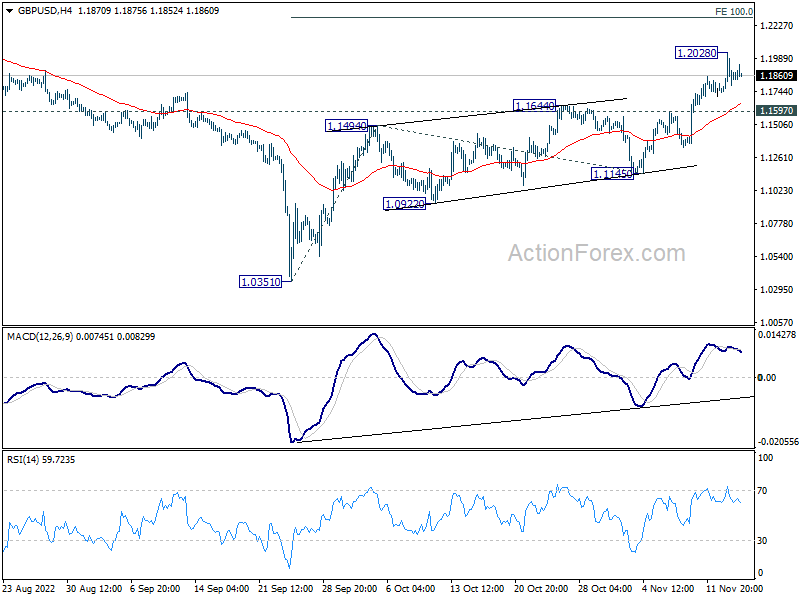

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1729; (P) 1.1878; (R1) 1.2016; More…

Intraday bias in GBP/USD is turned neutral with a temporary top formed at 1.2028, and more consolidations would be seen. Downside of retreat should be contained by 1.1597 minor support to bring another rally. On the upside, above 1.2028 will resume the rise from 1.0351 to 100% projection of 1.0351 to 1.1494 from 1.1145 at 1.2288.

{kind=link}

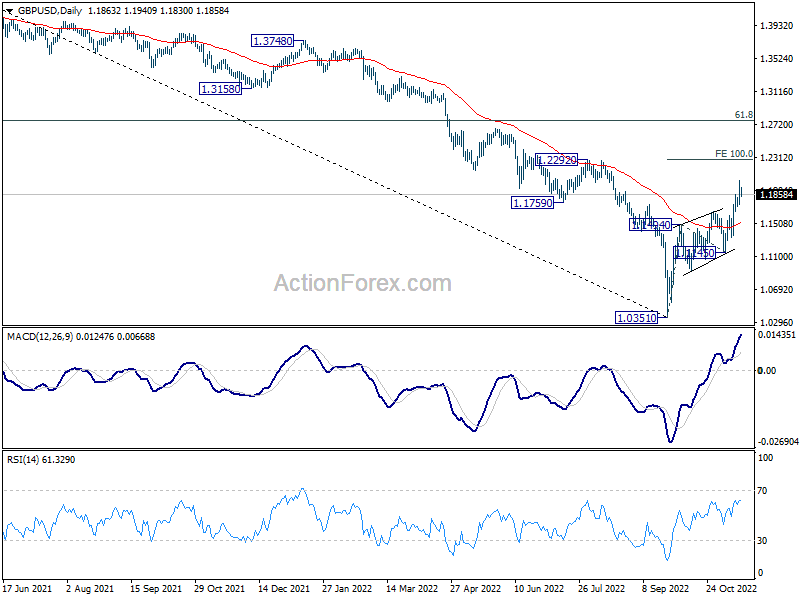

In the bigger picture, rise from 1.0351 medium term bottom is at least correcting whole down trend from 1.4248 (2021 high). Further rise is expected as long as 1.1145 support holds. Next target is 61.8% retracement of 1.4248 to 1.0351 at 1.2759

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/M Oct | -0.10% | 0.00% | ||

| 23:50 | JPY | Machinery Orders M/M Sep | -4.60% | 0.70% | -5.80% | |

| 00:30 | AUD | Wage Price Index Q/Q Q3 | 1.00% | 0.90% | 0.70% | 0.80% |

| 04:30 | JPY | Tertiary Industry Index M/M Sep | -0.40% | 0.60% | 0.70% | |

| 07:00 | GBP | CPI M/M Oct | 2.00% | 1.70% | 0.50% | |

| 07:00 | GBP | CPI Y/Y Oct | 11.10% | 10.60% | 10.10% | |

| 07:00 | GBP | Core CPI Y/Y Oct | 6.50% | 6.40% | 6.50% | |

| 07:00 | GBP | RPI M/M Oct | 2.50% | 1.80% | 0.70% | |

| 07:00 | GBP | RPI Y/Y Oct | 14.20% | 13.40% | 12.60% | |

| 07:00 | GBP | PPI Input M/M Oct | 0.60% | 1.00% | 0.40% | 0.90% |

| 07:00 | GBP | PPI Input Y/Y Oct | 19.20% | 17.70% | 20.00% | 20.80% |

| 07:00 | GBP | PPI Output M/M Oct | 0.30% | 0.00% | 0.20% | 0.30% |

| 07:00 | GBP | PPI Output Y/Y Oct | 14.80% | 14.80% | 15.90% | 16.30% |

| 07:00 | GBP | PPI Core Output M/M Oct | 0.50% | 1.30% | 0.70% | 0.80% |

| 07:00 | GBP | PPI Core Output Y/Y Oct | 13.30% | 14.00% | 14.00% | 14.40% |

| 13:15 | CAD | Housing Starts Oct | 267k | 275K | 300K | 299k |

| 13:30 | CAD | CPI M/M Oct | 0.70% | 0.80% | 0.10% | |

| 13:30 | CAD | CPI Y/Y Oct | 6.90% | 7.00% | 6.90% | |

| 13:30 | CAD | CPI Median Y/Y Oct | 4.80% | 4.80% | 4.70% | |

| 13:30 | CAD | CPI Trimmed Y/Y Oct | 5.30% | 5.30% | 5.20% | |

| 13:30 | CAD | CPI Common Y/Y Oct | 6.20% | 5.90% | 6.00% | 6.20% |

| 13:30 | USD | Retail Sales M/M Oct | 1.30% | 0.90% | 0.00% | |

| 13:30 | USD | Retail Sales ex Autos M/M Oct | 1.30% | 0.40% | 0.10% | |

| 13:30 | USD | Import Price Index M/M Oct | -0.20% | -0.50% | -1.20% | |

| 14:15 | USD | Industrial Production M/M Oct | 0.20% | 0.40% | ||

| 14:15 | USD | Capacity Utilization Oct | 80.40% | 80.30% | ||

| 15:00 | USD | Business Inventories Sep | 0.50% | 0.80% | ||

| 15:00 | USD | NAHB Housing Market Index Nov | 36 | 38 | ||

| 15:30 | USD | Crude Oil Inventories | -2.0M | 3.9M |