Little Reaction to US ADP and Eurozone CPI Miss, Consolidations Continue – Action Forex

Overall markets remain steady in consolidative trading today. There is little reaction to lower than expected Eurozone CPI and US ADP job data. Fed Chair Jerome Powell’s speech might trigger some volatility, or traders will have to wait for non-farm payrolls on Friday. For now, Dollar is the strongest for the week, followed by Yen and Euro. Canadian remains the weakest followed by Sterling and Swiss Franc. Aussie and Kiwi are mixed.

Technically, WTI crude oil staged a notably rebound this week after dipping to 71.40 initially. But it has yet to break through 83.07 minor resistance. Thus, another fall is in favor to resume the larger down trend. However, firm break of 83.07 will firstly confirm short term bottoming, and secondly open up further rise towards 94.25 resistance. Canadian Dollar could be give a lift if that happens.

In Europe, at the time of writing, FTSE is up 1.02%. DAX is up 0.26%. CAC is up 0.79%. Germany 10-year yield is up 0.030 at 1.954. Earlier in Asia, Nikkei dropped -0.21%. Hong Kong HSI rose 2.16%. China Shanghai SSE rose 0.05%. Singapore Strait Times rose 0.43%. Japan 10-year JGB yield dropped -0.0033 to 0.251.

US ADP employment grew 127k, Fed tightening having impact

US ADP private employment grew 127k in November, below expectation of 195k. By sector, goods- producing jobs dropped -86k. Service-providing jobs rose 213k. By establishment size, small companies lost -51k jobs. Medium companies added 246k. Large companies lost -68k.

Turning points can be hard to capture in the labor market, but our data suggest that Federal Reserve tightening is having an impact on job creation and pay gains. In addition, companies are no longer in hyper-replacement mode. Fewer people are quitting and the post-pandemic recovery is stabilizing.

Also released, US Q3 GDP growth was revised up to 2.9% annualized, price index revised up to 4.3%. Goods trade deficit widened to USD -99.0B.

BoE Pill expects headline inflation to tail off in 2nd half of next year quite rapidly

BoE Chief Economist Huw Pill said at a conference, “we are expecting to see headline inflation tail off in the second half of next year, in fact quite rapidly, on account of those base effects.” But, “there’s a lot of uncertainty around the outlook for gas price developments,” he added.

“Very low levels of unemployment and the association with the mid-1970s is not entirely reassuring from an inflection point of view,” Pill said. “People in the 50 to 65 age group, relative to pre-COVID levels, are having a higher level of inactivity not being in a job and not looking for work.”

Eurozone CPI slowed to 10% yoy in Nov

Eurozone CPI slowed from 10.6% yoy to 10.0% yoy in November, below expectation of 10.4% yoy. CPI ex-energy rose from 6.9% yoy to 7.0% yoy. CPI ex-energy, food, alcohol and tobacco was unchanged at 5.0% yoy.

Looking at the main components, energy is expected to have the highest annual rate in November (34.9%, compared with 41.5% in October), followed by food, alcohol & tobacco (13.6%, compared with 13.1% in October), non-energy industrial goods (6.1%, stable compared with October) and services (4.2%, compared with 4.3% in October).

Swiss KOF dropped to 89.5, economic outlook remains subdued

Swiss KOF Economic Barometer dropped from 90.9 to 89.5 in November, matched expectations. KOF said, “This is the fifth time in a row that the barometer has fallen. The outlook for the Swiss economy therefore remains subdued in the coming months.”

KOF added: “The negative development of the barometer is primarily driven by indicator bundles for the sector other services. Indicators for the accommodation and food service activities sector and private consumption are also weakening. In contrast, indicator bundles covering foreign demand record a slight positive development.”

France household consumption dropped sharply by -2.8% yoy in Oct

France household consumption dropped sharply by -2.8% mom in October, much worse than expectation of -0.9% mom. That’s also the largest decline since April 2021, primarily due to the sharp drop in energy consumption (-7.9%), but also stems from the decline in purchases of manufactured goods (-1.7%) and in food consumption (-1.4%).

All item CPI was unchanged at 6.2% yoy in November. Food price accelerated from1 2.0% yoy to 12.2% yoy. Energy prices slowed from 19.1% yoy to 18.5% yoy. Manufacturing products rose from 4.2 yoy to 4.4% yoy while services dropped from 3.1% yoy to 3.0% yoy.

Q3 GDP grew 0.2% qoq, unrevised.

China PMI manufacturing dropped to 48.0, non-manufacturing down to 46.7

China NBS PMI Manufacturing dropped from 49.2 to 48.0 in November, below expectation of 49.2. PMI Non-Manufacturing dropped from 48.7 to 46.7, below expectation of 48.0. Both readings were the lowest in seven months.

“In November, impacted by multiple factors including the wide and frequent spread of domestic outbreaks, and the international environment becoming more complex and severe, China’s purchasing managers’ index fell,” NBS senior statistician Zhao Qinghe said in a statement.

Zhao said domestic outbreaks in November caused “production activity to slow down and product orders to fall”, noting “increased fluctuation in market expectations”.

Japan industrial production dropped -2.6% mom in Oct, but bounce back expected

Japan industrial production dropped -2.6% mom in October, worse than expectation of -1.8% mom.

The seasonally adjusted production index for the manufacturing and mining sectors stood at 95.9 against 100 for the base year of 2015. The shipment index stood at 94.1, down -1.1%, and the inventory index at 103.0, down -0.8%.

The Ministry of Trade, Economy and Industry expects production to rise 3.3% in November and then 2.4% in December.

METI cut its assessment of industrial output for the first time in five months, saying “production is gradually picking up, but some weaknesses are observed.”

Australia monthly CPI slowed to 6.9% yoy in Oct, food inflation eased

Australia monthly CPI slowed from 7.3% yoy to 6.9% yoy in October. The most significant contributors to the annual rise were new dwellings (+20.4%), automotive fuel (+11.8%) and fruit and vegetables (+9.4%).

“High levels of building construction activity and ongoing shortages of labour and materials contributed to the rise in new dwellings” Michelle Marquardt, ABS Head of Prices Statistics said.

Automotive fuel prices accelerated from 10.1% to 11.8% as the government’s temporary cut to the fuel excise ended on September 29. Annually, prices for fruit and vegetables rose by 9.4%, down from 17.4% in September.

NZ ANZ business confidence dropped to -57.1, strain showing for businesses

New Zealand ANZ Business Confidence dropped from -42.7 to -57.1 in November. Looking at some details, own activity outlook dropped from -2.5 to -13.7, just 8 pts shy of 2009 lows. Export intentions dropped from -4.3 to -5.4. Investment intentions dropped from 1.1 to -8.1. Employment intentions dropped from 5.0 to -4.0. Pricing intentions dropped from 64.5 to 58.5. Cost expectations ticked up from 88.6 to 88.7. Inflation expectations rose from 6.13 to 6.39.

ANZ said, “The strain is showing for kiwi businesses. Cost increases remain relentless and margins are squeezed, firms are chronically understaffed, and they’re waiting for the hammer to fall as the impact of relentless monetary policy tightening eventually kicks in. There are a lot of dark clouds on the horizon, and this month’s survey reflects that.”

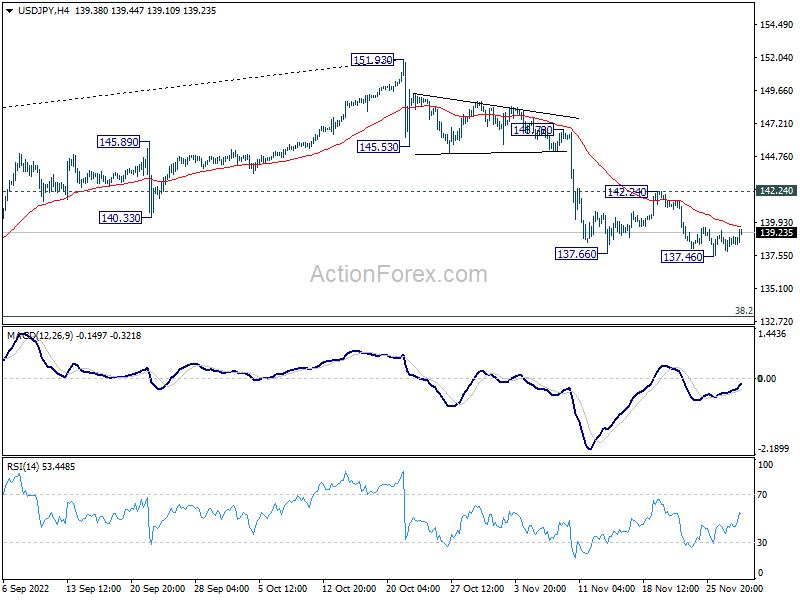

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 137.93; (P) 138.64; (R1) 139.42; More…

Intraday bias in USD/JPY is turned neutral first with today’s recovery. Further decline will remain in favor as long as 142.24 resistance holds. Break of 137.36 will resume the fall from 151.93 to 133.07 medium term fibonacci level. However, firm break of 142.24 will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

{kind=link}

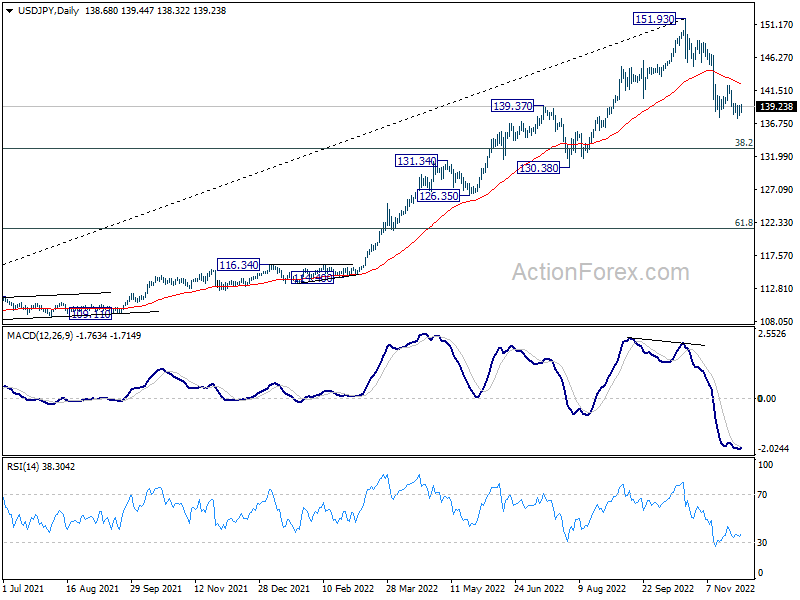

In the bigger picture, a medium term top should be formed at 151.93. Fall from there is correcting larger up trend from 102.58. It’s too early to call for bearish trend reversal. But even as a corrective move, such decline should target 38.2% retracement of 102.58 to 151.93 at 133.07, or further to 55 week EMA (now at 131.51).

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Oct | -10.70% | 3.80% | 3.60% | |

| 23:50 | JPY | Industrial Production M/M Oct P | -2.60% | -1.80% | -1.70% | |

| 00:00 | NZD | ANZ Business Confidence Nov | -57.1 | -42.7 | ||

| 00:01 | GBP | BRC Shop Price Index Y/Y Oct | 7.40% | 6.60% | ||

| 00:30 | AUD | Private Sector Credit M/M Oct | 0.60% | 0.60% | 0.70% | |

| 00:30 | AUD | Building Permits M/M Oct | -6.00% | -2.00% | -5.80% | -8.10% |

| 00:30 | AUD | Construction Work Done Q3 | 2.20% | 2.00% | -3.80% | -2.00% |

| 01:00 | CNY | Manufacturing PMI Nov | 48 | 49.2 | 49.2 | |

| 01:00 | CNY | Non-Manufacturing PMI Nov | 46.7 | 48 | 48.7 | |

| 05:00 | JPY | Housing Starts Y/Y Oct | -1.80% | -0.50% | 1.00% | |

| 07:45 | EUR | France Consumer Spending M/M Oct | -2.80% | -0.90% | 1.20% | |

| 07:45 | EUR | France GDP Q/Q Q3 | 0.20% | 0.20% | 0.20% | |

| 08:00 | CHF | KOF Leading Indicator Nov | 89.5 | 89.5 | 90.9 | |

| 08:55 | EUR | Germany Unemployment Change Nov | 17K | 10K | 8K | |

| 08:55 | EUR | Germany Unemployment Rate Nov | 5.60% | 5.50% | 5.50% | |

| 09:00 | CHF | Credit Suisse Economic Expectations Nov | -57.5 | -53.1 | ||

| 10:00 | EUR | Eurozone CPI Y/Y Nov P | 10.00% | 10.40% | 10.60% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Nov P | 5.00% | 4.90% | 5.00% | |

| 13:15 | USD | ADP Employment Change Nov | 127K | 195K | 239K | |

| 13:30 | USD | GDP Annualized Q3 P | 2.90% | 2.60% | 2.60% | |

| 13:30 | USD | GDP Price Index Q3 P | 4.30% | 4.10% | 4.10% | |

| 13:30 | USD | Wholesale Inventories Oct P | 0.80% | 0.50% | 0.60% | |

| 13:30 | USD | Goods Trade Balance (USD) Oct P | -99.0B | -90.2B | -92.2B | -91.9B |

| 14:45 | USD | Chicago PMI Nov | 45.4 | 45.2 | ||

| 15:00 | USD | Pending Home Sales M/M Oct | -5.80% | -10.20% | ||

| 15:30 | USD | Crude Oil Inventories | -3.2M | -3.7M |