Sterling Down after Weak Data, Euro and Swiss Franc Strong – Action Forex

Sterling is staying as one of the weakest for the week, after being sold off on weak economic data. The pressure is particularly apparent against Euro and Swiss Franc, which are the strongest ones for the week. While the financial markets are clearly in risk-off mode, Dollar is struggling to find renewed buying for now. Meanwhile, Aussie and Kiwi are still clearly pressured.

Technically, GBP/CHF’s break of 1.1326 minor support indicates that corrective pattern from 1.1574 has started the third leg already. Deeper decline is now in favor for the near term. But downside should be contained by 1.1047 cluster support (38.2% retracement of 1.1083 to 1.1574 at 1.1043 to bring rebound. An upside breakout through 1.1574 is still expected at a later stage, together with EUR/CHF breaking through 0.9953.

In Europe, at the time of writing, FTSE is down -1.45%. DAX is down -0.71%. CAC is down -1.43%. Germany 10-year yield is up 0.0964 at 2.177. Earlier in Asia, Nikkei dropped -1.87%. Hong Kong HSI rose 0.42%. China Shanghai SSE dropped -0.02%. Singapore Strait Times dropped -1.01%. Japan 10-year JGB yield dropped -0.0020 to 0.256.

ECB Villeroy: The match is over in fighting inflation

ECB Governing Council member Francois Villeroy de Galhau told BFM Business radio that “the match is not over” in fighting inflation, adding that rate hikes remain the main tool.

Regarding the quantitative tightening on the APP by EUR 15B per month from March, he said, “we will re-examine it in June and we will probably increase the reduction starting in July,”

“The European economy is more resilient than we feared even a few weeks ago,” he said. “There will be a strong slowdown in 2023. We will escape what certain people call a hard landing. We will have a rather significant rebound in 2024 and 2025.”

ECB Rehn: More 50bps hike at least as far as I see in Feb and Mar

ECB Governing Council member Olli Rehn said, “we will stay the course as President (Christine) Lagarde yesterday indicated and this will likely mean 50 basis point rate hikes in the coming meetings, at least as far as I see in February, and March.”

Another Governing Council member Robert Holzmann said the signal that more 50bps rate hikes are coming was “a toughly hawkish statement that for me is equivalent to the 75”. He added that ECB could “go deep into restrictive territory if needed”.

Bundesbank expects no severe economic slump in Germany

Bundesbank projects that the German economy will contract -0.5% in 2023, then grow by 1.7% in 2024 and 1.4% in 2025. President Joachim Nagel said, “Economic output is likely to shrink initially, but we expect a gradual recovery from the second half of 2023… Compared to the June projection, the rate of change of GDP for 2023 has been revised significantly downwards.”

HICP inflation is projected to decline to 7.2% in 2023, then to 4.1% in 2024, and 2.8% in 2025. HICP excluding energy and food is expected to increase slightly to 4.3% in 2023, then gradually decline to 2.9% in 2024 and 2.6% in 2025.

Eurozone PMI composite rose to 48.8, consistent with -0.2% GDP contraction in Q4

Eurozone PMI Manufacturing rose from 47.1 to 47.8 in December. PMI Services rose from 48.5 to 49.1. PMI Composite rose from 47.8 to 48.8. Still, the downside extended into its sixth successive month, even though rate of decline moderated.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said: “While the further fall in business activity in December signals a strong possibility of recession, the survey also hints that any downturn will be milder than thought likely a few months ago. The data for the fourth quarter are consistent with GDP contracting at a quarterly rate of just less than 0.2%, and forward-looking indicators are currently boding well for the rate of decline to ease further in the first quarter.”

Eurozone CPI finalized at 10.1% yoy in Nov, core CPI at 5.0% yoy

Eurozone CPI was finalized at 10.1% yoy in November, down from October’s 10.6% yoy. CPI core was finalized at 5.0%, unchanged from prior month’s reading. The highest contribution came from energy (+3.82%), followed by food, alcohol & tobacco (+2.84%), services (+1.76%) and non-energy industrial goods (+1.63%).

EU CPI was finalized at 11.1% mom, down from October’s 11.5% yoy. The lowest annual rates were registered in Spain (6.7%), France (7.1%) and Malta (7.2%). The highest annual rates were recorded in Hungary (23.1%), Latvia (21.7%), Estonia and Lithuania (both 21.4%). Compared with October, annual inflation fell in sixteen Member States, remained stable in three and rose in eight.

UK PMI manufacturing fell to 44.7, services recovery to 50.0

UK PMI Manufacturing dropped from 46.5 to 44.7 in December, a 31-month low. PMI Services rose from 48.8 to 50.0. PMI Composite rose from 48.2 to 49.0.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said: “The December data add to the likelihood that the UK is in recession, with the PMI indicating a 0.3% GDP contraction in the fourth quarter after the 0.2% decline seen in the three months to September.

“For now, the downturn looks to be relatively mild, and the easing in the rate of decline in December is encouraging news, as is the further marked cooling of inflationary pressures. However, the fact that the downturn has moderated compared to the turmoil created in the immediate aftermath of the botched “mini budget”, most notably in financial services, is no real cause for cheer. It is especially worrying to see business confidence and order book indicators remain so low by historical standards, with both of these key gauges signalling heightened degrees of economic stress.

“Hence it’s no surprise to see that businesses are battening down the hatches, most notably by reducing headcounts, in a sign that the downturn not only has further to run but could yet accelerate again, especially given December’s further hike to interest rates.”

UK retail sales volumes down -0.4% mom in Nov, values up 0.5% mom

In November, UK retail sales volumes declined -0.4% mom, much worse than expectation of 0.3% mom rise. Ex-fuel sales dropped -0.3% mom, worse than expectation of 0.3% mom. Fuel sales volumes declined -1.7% mom.

In value term, retail sales rose 0.5% mom while ex-fuel sales rose 0.1% mom.

Japan PMI manufacturing fell to 48.8, but services improved to 51.7

Japan PMI Manufacturing fell slightly from 49.0 to 48.8 in December, above expectation of 48.0. That’s the worst contractionary reading since October 2020. PMI Services, however, improved from 50.3 to 51.7. PMI Composite also rose back from 48.9 to 50.0.

Laura Denman, Economist at S&P Global Market Intelligence, said:

“The Japanese private sector economy saw a stabilisation in business activity in the final month of the year, with flash data indicating that the divergence between the manufacturing and services sectors has grown further. As has been the case since the launching of the National Travel Discount Programme in October, service providers have reportedly continued to profit from a boost in tourism volumes. Notably, firms have seemingly gained some pricing power as a result of improving demand within the sector and raised their selling prices at the sharpest rate since October 2019.

“Conversely, manufacturing firms continued to struggle in the face of subdued demand conditions and severe inflationary pressures with the latest flash PMI reading the lowest since October 2020. December data saw production and order books at Japanese manufacturers contract further, but at paces that were slower than in November. At the same time, though historically sharp, inflationary pressures cooled with the rate of input price inflation at the lowest level since September 2021.”

NZ BusinessNZ manufacturing dropped to 47.4, negative dynamic at play

New Zealand BusinessNZ Performance of Manufacturing Index dropped from 49.3 to 47.4 in November. That is the first time the PMI has shown consecutive months of contraction since the first nationwide lockdown in 2020.

Looking at some details, production fell slightly from 49.9 to 49.6. Employment fell from 48.7 to 46.7. New orders dropped further from 44.4 to 41.8. Finished stocks rose from 55.0 to 56.1. Deliveries dropped from 55.4 to 50.7.

BNZ Senior Economist, Craig Ebert stated “it’s been quite the sag in the PMI, compared to just three months ago when everything appeared positive. Of course, the PMI can dive down to the 40-zone when things get recessionary. And November’s result wasn’t that awful. That said, it also had componentry showing a negative dynamic at play”.

Australia PMI composite dropped to 47.3, first signs of desired soft landing

Australia PMI Manufacturing dropped from 51.3 to 50.4 in December, a 31-month low. PMI Services dropped from 47.6 to 46.9, an 11-month low. PMI Composite dropped from 48.0 to 47.3, also an 11-month low.

Warren Hogan, Chief Economic Advisor at Judo Bank said:

“The December results are one of the most up to date readings on the Australian economy and show that higher interest rates are starting to have the desired impact on activity. The Flash PMI readings for December are still well above levels that would normally be associated with recession. What we are seeing could be the first signs of a desired soft landing for the Australian economy in 2023…

“The slowing in this leading indicator of Australian economic activity will be welcomed by the RBA. Tighter monetary policy is having the desired effect, that is, a gradual slowing in domestic demand that should eventually filter through to lower inflation…

“This important leading indicator of Australian economic activity raises the prospect of an extended pause in the rate hiking cycle. As the rate hikes of 2022 continue to work through the economy over the first half of 2023, the RBA appears to have some scope to sit back and watch for a while.”

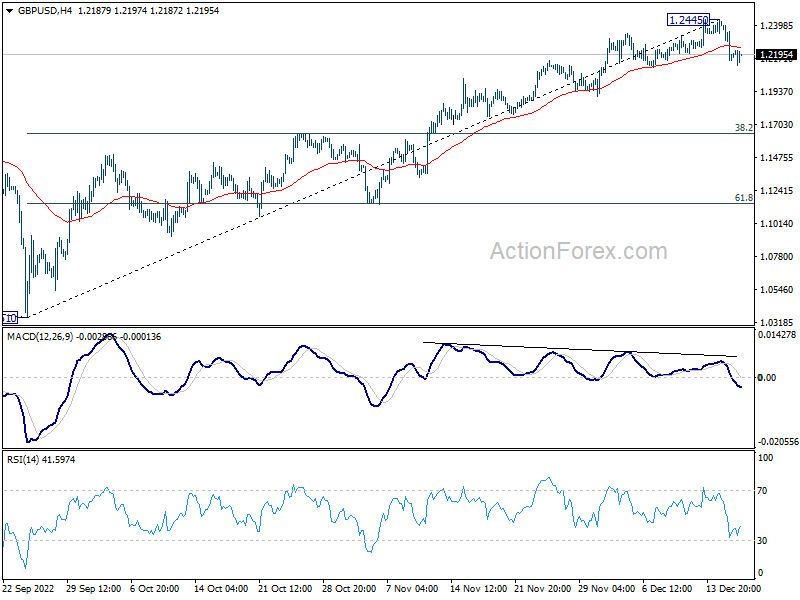

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2079; (P) 1.2256; (R1) 1.2355; More…

Intraday bias in GBP/USD remains on the downside for the moment. Fall from 1.2445 short term top should target 55 day EMA (now at 1.1865). Firm break there will target 38.2% retracement of 1.0351 to 1.2445 at 1.1645. For now, risk will stay on the downside as long as 1.2445 resistance holds, in case of recovery.

{kind=link}

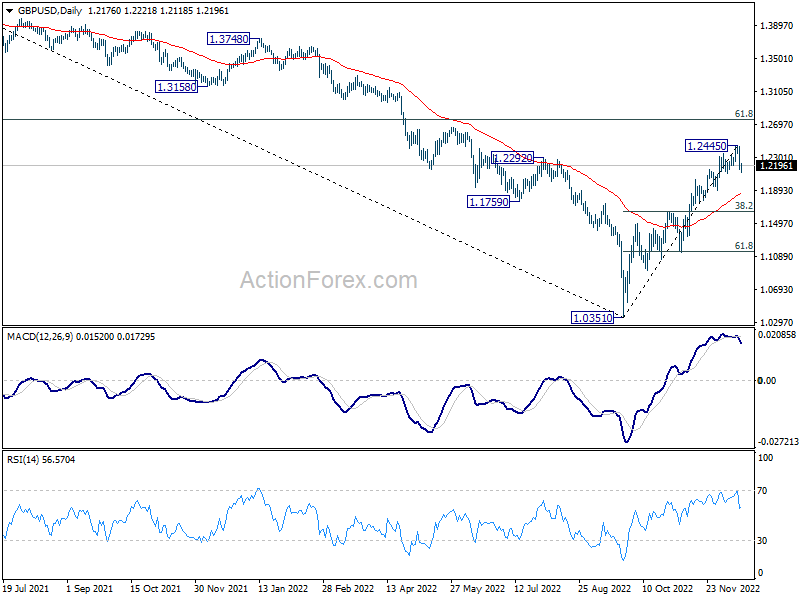

In the bigger picture, rise from 1.0351 medium term bottom is at least correcting whole down trend from 1.4248 (2021 high). Further rise is expected as long as 1.1644 resistance turned support holds. Next target is 61.8% retracement of 1.4248 to 1.0351 at 1.2759. Sustained break there will pave the way back to 1.4248. This will remain the favored case as long as 55 day EMA (now at 1.1860) holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Nov | 47.4 | 49.3 | ||

| 22:00 | AUD | Manufacturing PMI Dec P | 50.4 | 51.3 | ||

| 22:00 | AUD | Services PMI Dec P | 46.9 | 47.6 | ||

| 00:01 | GBP | GfK Consumer Confidence Dec | -42 | -43 | -44 | |

| 00:30 | JPY | Manufacturing PMI Dec P | 48.8 | 48 | 49 | |

| 07:00 | GBP | Retail Sales M/M Nov | -0.40% | 0.30% | 0.60% | 0.90% |

| 07:00 | GBP | Retail Sales Y/Y Nov | -5.90% | -5.60% | -6.10% | -5.90% |

| 07:00 | GBP | Retail Sales ex-Fuel M/M Nov | -0.30% | 0.30% | 0.30% | 0.70% |

| 07:00 | GBP | Retail Sales ex-Fuel Y/Y Nov | -5.90% | -5.80% | -6.70% | -6.40% |

| 08:15 | EUR | France Manufacturing PMI Dec P | 48.9 | 48.1 | 48.3 | |

| 08:15 | EUR | France Services PMI Dec P | 48.1 | 49.1 | 49.3 | |

| 08:30 | EUR | Germany Manufacturing PMI Dec P | 47.4 | 46.7 | 46.2 | |

| 08:30 | EUR | Germany Services PMI Dec P | 49 | 46.4 | 46.1 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Dec P | 47.8 | 46.8 | 47.1 | |

| 09:00 | EUR | Eurozone Services PMI Dec P | 49.1 | 48.5 | 48.5 | |

| 09:30 | GBP | Manufacturing PMI Dec P | 44.7 | 46.5 | 46.5 | |

| 09:30 | GBP | Services PMI Dec P | 50 | 48.5 | 48.8 | |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Oct | -28.3B | -32.5B | -37.7B | -36.4B |

| 10:00 | EUR | CPI Y/Y Nov F | 10.10% | 10.00% | 10.00% | |

| 10:00 | EUR | CPI Core Y/Y Nov F | 5.00% | 5.00% | 5.00% | |

| 13:30 | CAD | Wholesale Sales M/M Oct | 2.10% | 1.40% | 0.10% | |

| 14:45 | USD | Manufacturing PMI Dec P | 47.7 | 47.7 | ||

| 14:45 | USD | Services PMI Dec P | 46.5 | 46.2 |