NZD Higher after RBNZ Hike, Other Commodity Currencies Soft – Action Forex

New Zealand Dollar rises broadly today after hawkish RBNZ hike. But other commodity currencies are lagging behind on risk-off sentiment. As for the week so far, Sterling remains the strongest, as supported by optimism on avoiding recession. Dollar followed as second as supported by rising treasury yields, and then Swiss Franc. Aussie is the worst, followed by Yen and then Loonie.

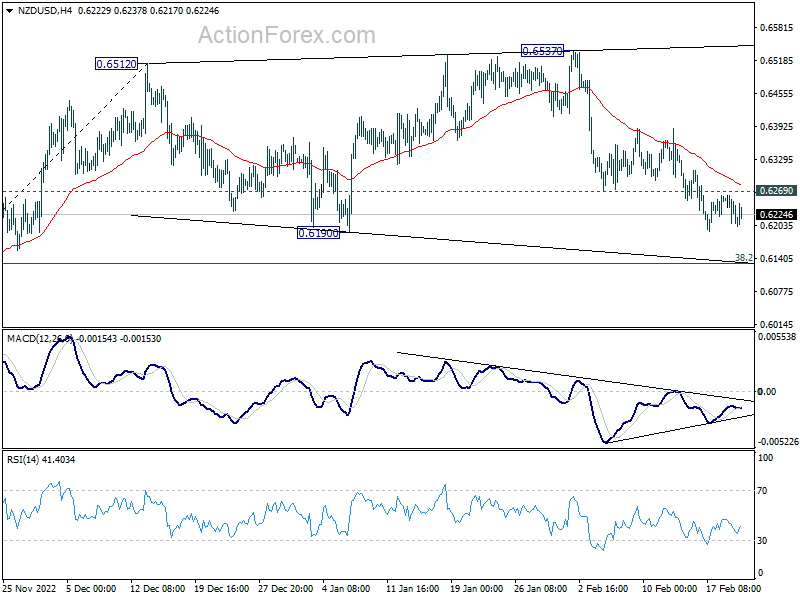

Technically, NZD/USD’s recovery today is rather weak, and doesn’t warrant a reversal. Fall from 0.6537 is still in favor to continue as long as 0.6269 support turned resistance holds. Yet, the three-wave consolidation from 0.6512 should be about to complete. Downside momentum should continue to slow while support will come in below 0.6190. Break of 0.6269 will suggest short term bottoming and bring stronger rebound.

{kind=link}

In Asia, at the time of writing, Nikkei is down -1.30%. Hong Kong HSI is up 0.03%. China Shanghai SSE is down -0.25%. Singapore Strait Times is down -0.18%. Japan 10-year JGB yield is up 0.009 at 0.512. Overnight, DOW dropped -2.06%. S&P 500 dropped -2.00%. NASDAQ dropped -2.50%. 10-year yield rose 0.127 to 3.955.

RBNZ hikes 50bps, sees OCR peaking at 5.5%

RBNZ raises the Official Cash Rate by 50bps to 4.75% as widely expected. It also maintained hawkish bias and noted, “monetary conditions need to tighten further”.

Regarding cyclone Gabrielle, it’s “too early to accurately assess the monetary policy implications”.. The committee will also “look through” the “short-term output variations and direct price effects” related to the weather event.

In the economic projections, RBNZ sees OCR peaking at 5.5% in Q4 2023, and stays above 5% until Q1 2025. GDP is projected to contract in Q2, Q3 and Q4 this year. Inflation is projected to drop gradually from 7.3% in Q1, but only falls back below 3% in Q3 2024.

In the post meeting press conference, RBNZ Governor Adrian Orr said that all options remain on the table today, “including 25, 50 and 75 bps hikes.” There was “very little discussion of a 25bp rate hike”, while “most focus was on 50bp”.

Australia Westpac leading index ticked up, growth below trend through most of 2023

Australia Westpac-MI leading index ticked up slightly in January. Growth in the three to nine months period is estimated to be -1.04% below trend, comparing to -1.09% in December.

Westpac added that growth would remain below trend through most of 2023, with global factors, monetary policy and, recently, hours worked have weighed heavily on the Index.

Regarding RBA policy, Westpac expects another 25bps hike at March meeting to 3.60%. The cash rate is expected to peak at 3.85%, but recent communications from RBA “imply upside risks to that forecast”.

BoJ Tamura: Appropriate to maintain monetary easing for now

BoJ board member Naoki Tamura said, “we’re now in a phase where we need to scrutinise whether Japan can achieve a positive wage-inflation cycle. As such, it’s appropriate to maintain monetary easing for now.”

Tamura also noted that December’s decision to double to yield cap was aimed at making monetary easing more sustainable, not at tightening. “At this stage, it’s important to follow carefully and humbly how markets would stabilise and to what extent market functions will improve,” he said.

Looking ahead

Germany Ifo business climate is the main focus in European session while CPI final will also be released. Swiss will release ZEW expectations. Later in the day, FOMC minutes will take center stage. Canada new housing price index will also be featured.

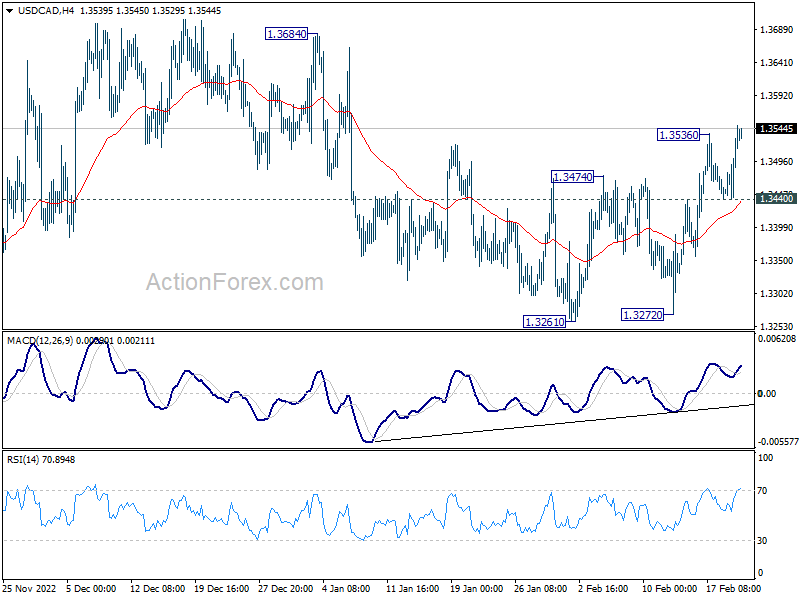

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3470; (P) 1.3509; (R1) 1.3577; More….

USD/CAD’s rally resumed after brief retreat and intraday bias is back on the upside. Outlook is unchanged that corrective pattern from 1.3967 should have completed at 1.3261. Further rally should now be seen to 1.3684 resistance first. Break there will pave the way back to retest 1.3976 high. On the downside, however, break of 1.3440 support will dampen this bullish cas and turn intraday bias neutral first.

{kind=link}

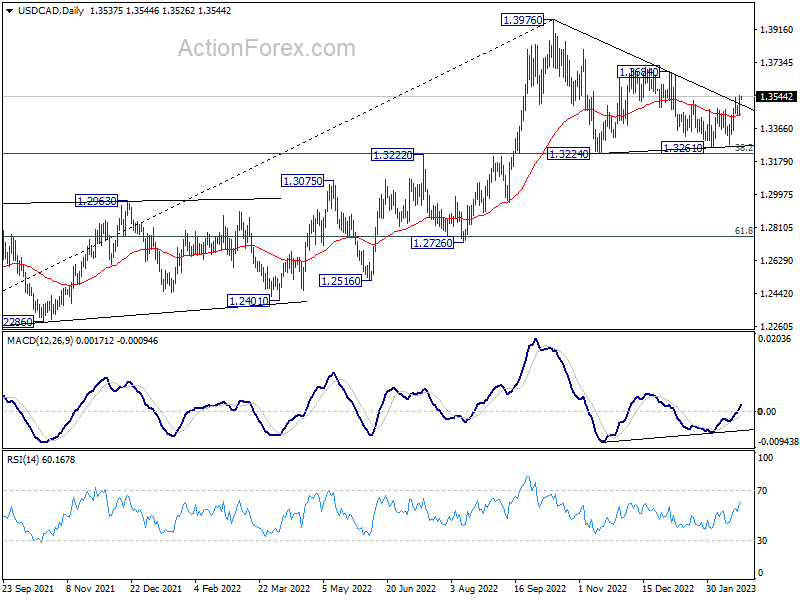

In the bigger picture, as long as 1.3222 cluster support (38.2% retracement of 1.2005 to 1.3976 at 1.3223) holds, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 high at a later stage. However, firm break of 1.3222/3 will indicate that the trend might have reversed. Deeper fall would be seen to next cluster support at 1.2726 (61.8% retracement at 1.2758).

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Jan | -1954M | -475M | -636M | |

| 23:30 | AUD | Westpac Leading Index M/M Jan | -0.10% | -0.10% | -0.20% | |

| 23:50 | JPY | Corporate Service Price Index Y/Y Jan | 1.60% | 1.50% | 1.50% | |

| 00:30 | AUD | Wage Price Index Q/Q Q4 | 0.80% | 1.00% | 1.00% | 1.10% |

| 00:30 | AUD | Construction Work Done Q4 | -0.40% | 1.60% | 2.20% | |

| 01:00 | NZD | RBNZ Rate Decision | 4.75% | 4.75% | 4.25% | |

| 02:00 | NZD | RBNZ Press Conference | ||||

| 07:00 | EUR | Germany CPI M/M Jan F | 1.00% | 1.00% | ||

| 07:00 | EUR | Germany CPI Y/Y Jan F | 8.70% | 8.70% | ||

| 09:00 | CHF | ZEW Expectations Feb | -40 | |||

| 09:00 | EUR | Germany IFO Business Climate Feb | 91.1 | 90.2 | ||

| 09:00 | EUR | Germany IFO Current Assessment Feb | 94.3 | 94.1 | ||

| 09:00 | EUR | Germany IFO Expectations Feb | 84.7 | 86.4 | ||

| 13:30 | CAD | New Housing Price Index M/M Jan | 0.10% | 0.00% | ||

| 19:00 | USD | FOMC Minutes |