Risk Sentiment Stabilized, Dollar Looks Into FOMC Minutes – Action Forex

Risk sentiment appears to have stabilized as markets enter into US session. There have been increasing speculation that Fed would revert to a 50bps rate hike in March. Traders might try to scrutinize FOMC minutes to get more hints on the chance. But overall, that’s not the majority’s opinion for now. In the currency markets, Sterling remains the strongest one for the week, followed by Dollar and Kiwi. Aussie is the worst followed by Euro and then Canadian.

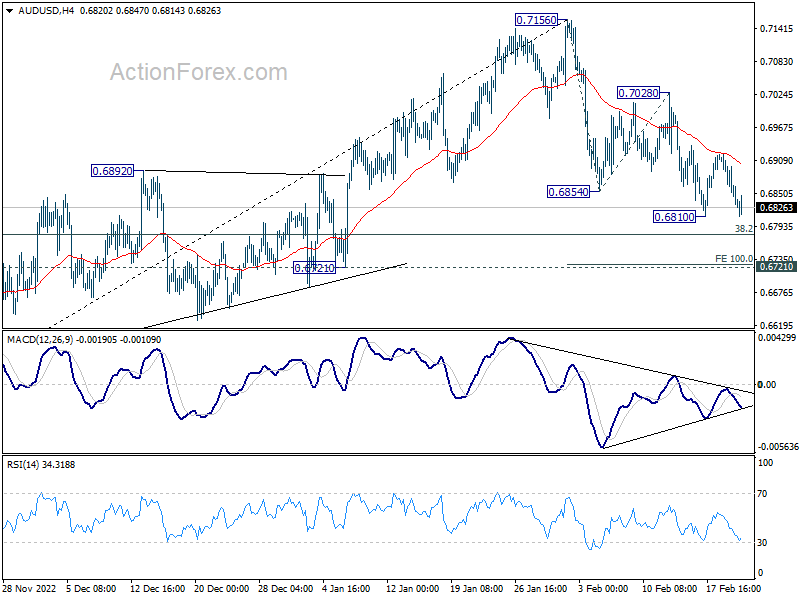

Technically, USD/CAD has resumed near term rally yesterday. It could be AUD/USD’s turn in the current session. Break of 0.6810 temporary low will resume whole corrective fall from 0.7156 to 100% projection of 0.6854 to 0.7028 from 0.6854 at 0.6736, which is close to 0.6721 key structural support. Breakout in AUD/USD could be triggered by resumed selloff in stocks after FOMC minutes.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.78%. DAX is down -0.09%. CAC is down -0.18%. Germany 10-year yield is up 0.0008 at 2.532. Earlier in Asia, Nikkei dropped -1.34%. Hong Kong HSI dropped -0.51%. China Shanghai SSE dropped -0.47%. Singapore Strait Times dropped -0.21%. Japan 10-year JGB yield dropped -0.0001 to 0.503.

Fed Bullard: Let’s be sharp and get inflation under control in 2023

St. Louis Fed President James Bullard told CNBC, “Our risk now is inflation doesn’t come down and reaccelerates and then what do we do.

“We are going to have to react, and if inflation doesn’t start to come down, you know, you risk this replay of the 1970s where you had 15 years and you’re trying to battle the drag, and you don’t want to get into that.

“Let’s be sharp now, let’s get inflation under control in 2023 and it’s a good time to fight inflation because the labor market is still strong,” He added.

Bullard reiterated his view that Federal funds rate at 5.25-5.50% rate would be adequate for the task.

Germany Ifo rose to 91.1, gradually working out of weakness

Germany Ifo Business Climate rose from 90.2 to 91.1 in February, matched expectations. Current Assessment Index dropped from 94.1 to 93.0, below expectation of 94.3. Expectations Index rose from 86.4 to 88.5, above expectation of 94.7.

By sector, manufacturing rose form -0.7 to 1.5. Services rose from 0.2 to 1.3. Trade rose from -15.4 to -10.6. Construction rose from -21.7 to -19.6.

Ifo said: “The German economy is gradually working its way out of a period of weakness.”

Villeroy: ECB in no way obliged to hike at every meeting

ECB governor François Villeroy de Galhau told French daily Les Echos that investors have “overreacted” to ECB communication since last week.

“There is an excess of volatility in the terminal rate expectations,” he said. “Put differently, markets have overreacted a little since Thursday.”

Villeroy also noted that while interest rate could peak by the end of summer, ECB is “in no way” obliged to raise borrowing costs at every meeting between now and September.

RBNZ hikes 50bps, sees OCR peaking at 5.5%

RBNZ raises the Official Cash Rate by 50bps to 4.75% as widely expected. It also maintained hawkish bias and noted, “monetary conditions need to tighten further”.

Regarding cyclone Gabrielle, it’s “too early to accurately assess the monetary policy implications”.. The committee will also “look through” the “short-term output variations and direct price effects” related to the weather event.

In the economic projections, RBNZ sees OCR peaking at 5.5% in Q4 2023, and stays above 5% until Q1 2025. GDP is projected to contract in Q2, Q3 and Q4 this year. Inflation is projected to drop gradually from 7.3% in Q1, but only falls back below 3% in Q3 2024.

In the post meeting press conference, RBNZ Governor Adrian Orr said that all options remain on the table today, “including 25, 50 and 75 bps hikes.” There was “very little discussion of a 25bp rate hike”, while “most focus was on 50bp”.

Australia Westpac leading index ticked up, growth below trend through most of 2023

Australia Westpac-MI leading index ticked up slightly in January. Growth in the three to nine months period is estimated to be -1.04% below trend, comparing to -1.09% in December.

Westpac added that growth would remain below trend through most of 2023, with global factors, monetary policy and, recently, hours worked have weighed heavily on the Index.

Regarding RBA policy, Westpac expects another 25bps hike at March meeting to 3.60%. The cash rate is expected to peak at 3.85%, but recent communications from RBA “imply upside risks to that forecast”.

BoJ Tamura: Appropriate to maintain monetary easing for now

BoJ board member Naoki Tamura said, “we’re now in a phase where we need to scrutinise whether Japan can achieve a positive wage-inflation cycle. As such, it’s appropriate to maintain monetary easing for now.”

Tamura also noted that December’s decision to double to yield cap was aimed at making monetary easing more sustainable, not at tightening. “At this stage, it’s important to follow carefully and humbly how markets would stabilise and to what extent market functions will improve,” he said.

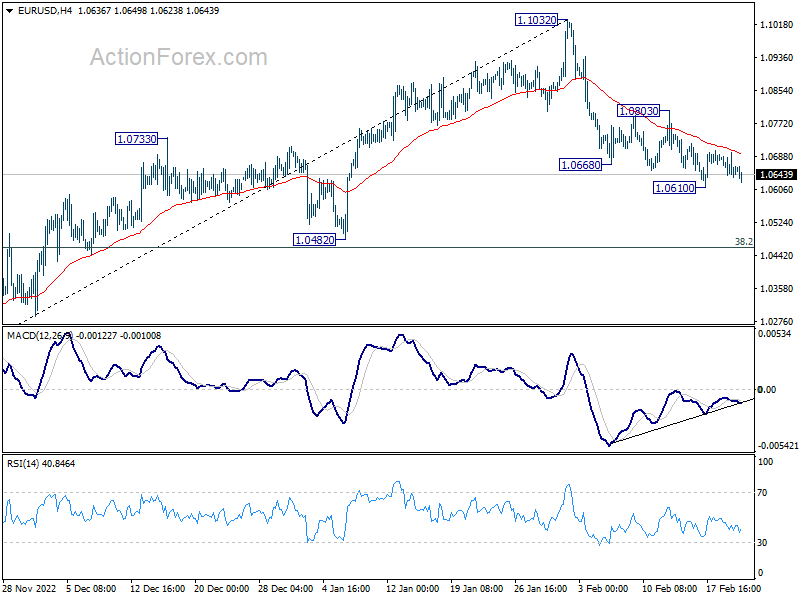

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0623; (P) 1.0661; (R1) 1.0683; More…

Range trading continues in EUR/USD and intraday bias stays neutral first. Further decline is in favor with 1.0803 resistance intact. On the downside, break of 1.0610 will resume the corrective fall from 1.1032 and 38.2% retracement of 0.9534 to 1.1032 at 1.0463. Strong support should be seen around there to bring rebound, at least on first attempt.

{kind=link}

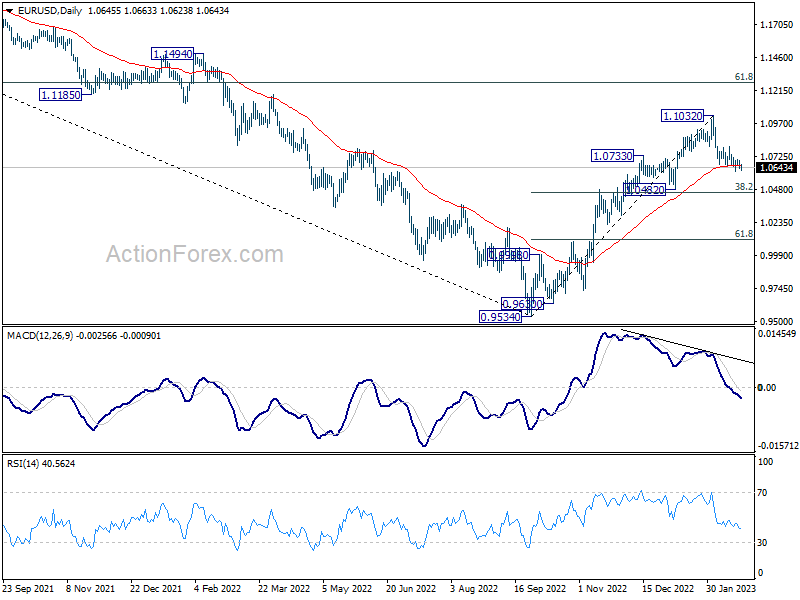

In the bigger picture, the rally from 0.9534 low (2022 low) is a medium term up trend rather than a correction. Further rise is in favor to 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 next. This will remain the favored case as long as 1.0482 support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Jan | -1954M | -475M | -636M | |

| 23:30 | AUD | Westpac Leading Index M/M Jan | -0.10% | -0.10% | -0.20% | |

| 23:50 | JPY | Corporate Service Price Index Y/Y Jan | 1.60% | 1.50% | 1.50% | |

| 00:30 | AUD | Wage Price Index Q/Q Q4 | 0.80% | 1.00% | 1.00% | 1.10% |

| 00:30 | AUD | Construction Work Done Q4 | -0.40% | 1.60% | 2.20% | |

| 01:00 | NZD | RBNZ Rate Decision | 4.75% | 4.75% | 4.25% | |

| 02:00 | NZD | RBNZ Press Conference | ||||

| 07:00 | EUR | Germany CPI M/M Jan F | 1.00% | 1.00% | 1.00% | |

| 07:00 | EUR | Germany CPI Y/Y Jan F | 8.70% | 8.70% | 8.70% | |

| 09:00 | CHF | ZEW Expectations Feb | -12.3 | -40 | ||

| 09:00 | EUR | Germany IFO Business Climate Feb | 91.1 | 91.1 | 90.2 | |

| 09:00 | EUR | Germany IFO Current Assessment Feb | 93.9 | 94.3 | 94.1 | |

| 09:00 | EUR | Germany IFO Expectations Feb | 88.5 | 84.7 | 86.4 | |

| 13:30 | CAD | New Housing Price Index M/M Jan | -0.20% | 0.10% | 0.00% | |

| 19:00 | USD | FOMC Minutes |