China’s Robust Services Data Boosts Markets; UK Joins CPTPP, Strengthening Sterling – Action Forex

As March comes to an end, strong services data from China has invigorated the markets, providing additional support to Australian and New Zealand Dollar. Sterling is further bolstered by the news that the UK has secured a deal to join the 11-country Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), while Yen continues its selloff alongside a softer Euro and Swiss Franc.

For the week, Canadian Dollar stands as the strongest performer, followed by Euro and Sterling. Yen lags as the worst performer, succeeded by Dollar and Swiss Franc. Aussie and Kiwi are mixed, but upcoming Eurozone CPI and US PCE inflation data could shift the picture.

Technically, NASDAQ’s break above last week’s high of 12013.98 suggests a resumption of the rise from 10982.80, and a larger rebound from 10088.82 could be ready to resume too, potentially breaking through the 12269.55 resistance soon. This development, if realized, will continue to suppress any rebound attempts in Dollar and Yen. However, it remains to be seen whether Euro and Sterling or Loonie and Aussie will gain more ground.

In Asia, at the time of writing, Nikkei is up 1.10%. Hong Kong HSI is up 0.84%. China Shanghai SSE is up 0.22%. Singapore Strait Times is up 0.20%. Japan 10-year JGB yield is up 0.0035 at 0.329. Overnight, DOW rose 0.43%. S&P 500 rose 0.57%. NASDAQ rose 0.73%. 10-year yield dropped -0.0015 to 3.551.

Fed Collins: Tightening lending standards may partially offset need for more rate hikes

Fed’s ongoing battle against inflation was underscored by Boston Fed President Susan Collins, who expressed concerns over the persistently high inflation rates. She stated yesterday, “Inflation remains too high, and recent indicators reinforce my view that there is more work to do, to bring inflation down to the 2% target associated with price stability.”

Collins reiterated her belief that Fed can successfully lower inflation without causing a recession, but acknowledged that a rise in unemployment would be necessary to achieve this goal. As Fed prepares for its May meeting, Collins admitted it is too early to predict the appropriate course of action.

She also noted that recent developments may lead banks to adopt a more conservative outlook and tighten lending standards, thus helping to slow the economy and reduce inflationary pressures. “These developments may partially offset the need for additional rate increases,” she added in her prepared remarks.

Fed Kashkari: More work to do to bring services back into balance

Minneapolis Fed President Neel Kashkari expressed concerns over the current state of the service economy and its potential impact on inflation. “The one area that is particularly concerning right now is that the services economy, outside of housing, has not shown any sign of slowing down,” he said yesterday.

Kashkari emphasized the need for further action, stating, “Wage growth is still growing faster than what is consistent with our 2% inflation target; that tells me we still have more work to do to bring the services side of the economy back into balance… we know we have to get inflation down, and we will.”

He also addressed the ongoing banking stresses, drawing a comparison to the 2008 financial crisis. While he doesn’t expect a repeat of that situation, he cautioned that banking panics tend to take longer to resolve than expected: “Every time in 2008, we thought we were through it, there was another shoe yet to drop. So I am prepared to think this could take a little longer than we expect until we fully get behind it.”

Although the US banking system is sound and most banks are prepared for higher rates, Kashkari raised concerns about the potential for a sustained credit crunch, which could slow down the economy. “What’s unclear right now is how much the banking stresses of the past few weeks are leading to a sustained credit crunch,” he said.

Fed Barkin: I’m comfortable with the trajectory we’re on now

Richmond Fed President Thomas Barkin expressed his comfort with Fed’s current approach to interest rate hikes, stating, “I’m comfortable with the trajectory we’re on now, meeting by meeting, whether you need a 25 basis point hike or not.” He acknowledged the challenges of finding the right balance, but emphasized that even if the decision isn’t perfect, it won’t be too far off.

Barkin also addressed the uncertainties surrounding the ongoing banking situation and its potential impact on consumer confidence, business investment, and the availability of credit. “There is a lot of uncertainty about what if anything this bank situation does to consumer confidence, business confidence, business investment, consumer spending, availability of credit,” he said, adding that it’s difficult to predict the future effects on demand and inflation.

Despite the uncertainties, Barkin highlighted the wide range of possible outcomes and Fed’s ability to respond accordingly. “If inflation persists, we can react by raising rates further,” he said. “If I am wrong about the pricing dynamics at play, or about credit conditions, then we can respond appropriately.”

Japan reported strong industrial production and retail sales growth

Japan reported strong industrial production growth of 4.5% mom in February, surpassing expectations of 2.8% mom growth. The seasonally adjusted production index for the manufacturing and mining sectors reached 94.8, with the industry ministry predicting a 2.3% mom increase in March and a 4.4% mom advance in April.

Retail sales also exceeded expectations, rising 6.6% yoy compared to the anticipated 5.9% yoy. However, the unemployment rate increased from 2.4% to 2.6%, higher than the expected 2.4%.

Inflation in Tokyo experienced a slight decline, with the March CPI dropping from 3.4% yoy to 3.3% yoy, still above the expected 2.7% yoy. The core CPI (excluding fresh food) eased from 3.3% yoy to 3.2% yoy, meeting expectations. Meanwhile, the core-core CPI (excluding fresh food and energy) rose from 3.2% yoy to 3.4% yoy, surpassing the anticipated 3.3% yoy.

Elsewhere

In March, China’s NBS PMI Manufacturing dipped from 52.6 to 51.9, aligning with expectations. Despite the slight decline, the data still indicated growth for the third consecutive month and represented the second-highest level in nearly two years. Conversely, PMI Non-Manufacturing experienced a significant jump from 56.3 to 58.2, surpassing the expected 54.3. This marked the highest level recorded since May 2011.

Looking ahead, Eurozone CPI flash is the main focus in European session while unemployment rate will also be released. . Germany will release import price, retail sales and unemployment. Swiss will release retail sales. UK will publish Q4 GDP final.

Later in the day, US personal income and spending, with PCE inflation will be the highlight. Chicago PMI will also be released.

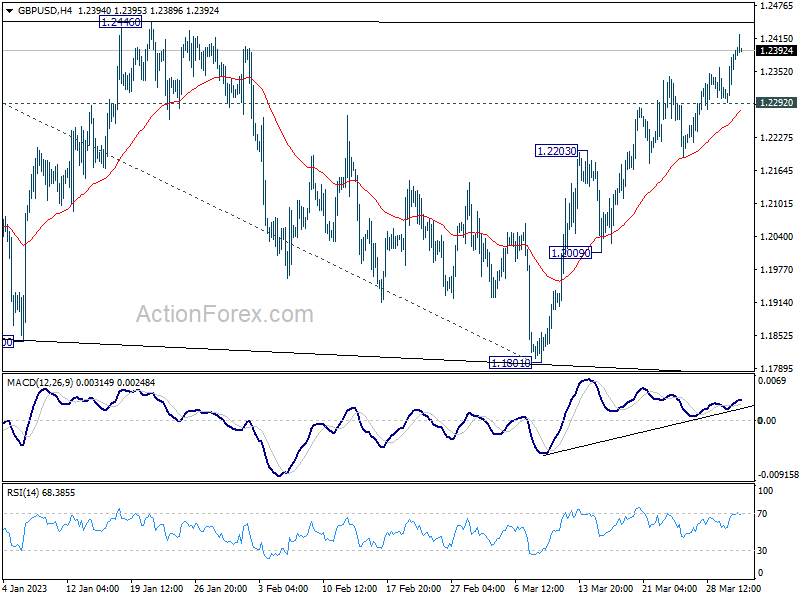

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2324; (P) 1.2359; (R1) 1.2423; More…

GBP/USD’s rally continues today and intraday bias stays on the upside for 1.2445/6 resistance zone. Decisive break there will resume larger rally from 1.0351, and target 1.2759 fibonacci level. On the upside, below 1.2292 minor support will turn intraday bias neutral first. But further rally will remain in favor as long as 1.2203 resistance turned support holds.

{kind=link}

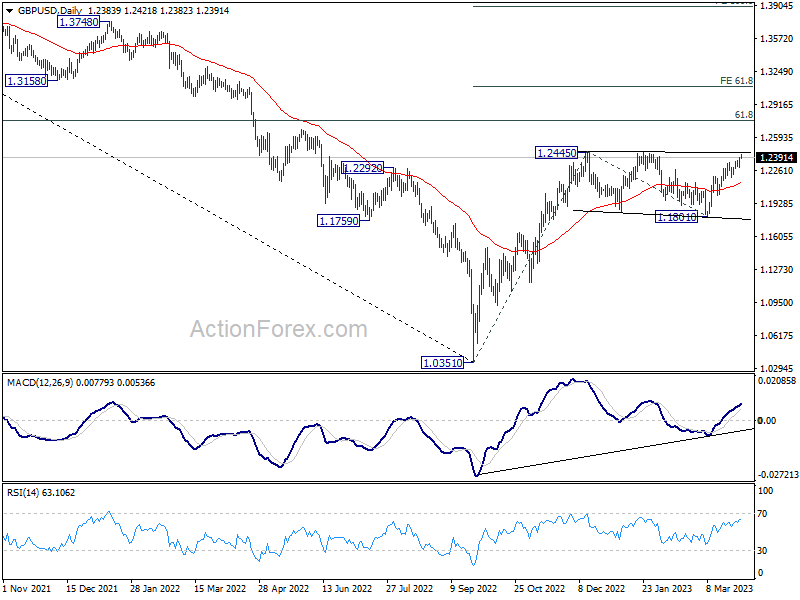

In the bigger picture, the rise from 1.0351 medium term term bottom (2022 low) is in progress for 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. Sustained break there will add to the case of long term bullish trend reversal. Further break of 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095 could prompt upside acceleration to 100% projection at 1.3895. For now, this will remain the favored case as long as 1.1801 support holds, even in case of deep pull back.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Mar | 3.20% | 3.20% | 3.30% | |

| 23:30 | JPY | Unemployment Rate Feb | 2.60% | 2.40% | 2.40% | |

| 23:50 | JPY | Industrial Production M/M Feb P | 4.50% | 2.80% | -5.30% | |

| 23:50 | JPY | Retail Trade Y/Y Feb | 6.60% | 5.90% | 6.30% | |

| 00:30 | AUD | Private Sector Credit M/M Feb | 0.30% | 0.30% | 0.40% | |

| 01:00 | CNY | NBS Manufacturing PMI Mar | 51.9 | 51.9 | 52.6 | |

| 01:00 | CNY | Non-Manufacturing PMI Mar | 58.2 | 54.3 | 56.3 | |

| 05:00 | JPY | Housing Starts Y/Y Feb | -0.3% | -0.50% | 6.60% | |

| 06:00 | GBP | GDP Q/Q Q4 F | 0.00% | 0.00% | ||

| 06:00 | GBP | Current Account (GBP) Q4 | -17.5B | -19.4B | ||

| 06:00 | EUR | Germany Import Price Index M/M Feb | -0.80% | -1.20% | ||

| 06:00 | EUR | Germany Retail Sales M/M Feb | 0.50% | -0.30% | ||

| 06:30 | CHF | Real Retail Sales Y/Y Feb | -1.00% | -2.20% | ||

| 06:45 | EUR | France Consumer Spending M/M Feb | 0.20% | 1.50% | ||

| 07:55 | EUR | Germany Unemployment Change Feb | 2K | 2K | ||

| 07:55 | EUR | Germany Unemployment Rate Feb | 5.50% | |||

| 09:00 | EUR | Eurozone Unemployment Rate Feb | 6.70% | 6.70% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Mar P | 7.20% | 8.50% | ||

| 09:00 | EUR | Eurozone Core CPI Y/Y Mar P | 5.70% | 5.60% | ||

| 12:30 | CAD | GDP M/M Jan | 0.00% | -0.10% | ||

| 12:30 | USD | Personal Income M/M Feb | 0.30% | 0.60% | ||

| 12:30 | USD | Personal Spending Feb | 0.30% | 1.80% | ||

| 12:30 | USD | PCE Price Index M/M Feb | 0.20% | 0.60% | ||

| 12:30 | USD | PCE Price Index Y/Y Feb | 5.30% | 5.40% | ||

| 12:30 | USD | Core PCE Price Index M/M Feb | 0.40% | 0.60% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Feb | 4.40% | 4.70% | ||

| 13:45 | USD | Chicago PMI Mar | 43.6 | 43.6 | ||

| 14:00 | USD | Michigan Consumer Sentiment Mar F | 63.4 | 63.4 |