Sterling Hit by BoE Bailey; Aussie Suffers Amid Copper Price Decline – Action Forex

In the wake of comments from BoE Governor Andrew Bailey suggesting a potential pause in rate hikes, Sterling has taken a sharp downward turn overnight. Despite the expected 25bps hike yesterday, Bailey’s interview with Bloomberg TV sent ripples through the market, causing a broad sell-off of the Pound. With UK GDP data on the horizon, Sterling’s performance remains under scrutiny. However, unless GDP figures significantly exceed expectations, it’s more probable than not that Sterling will conclude the week as one of the weakest performers.

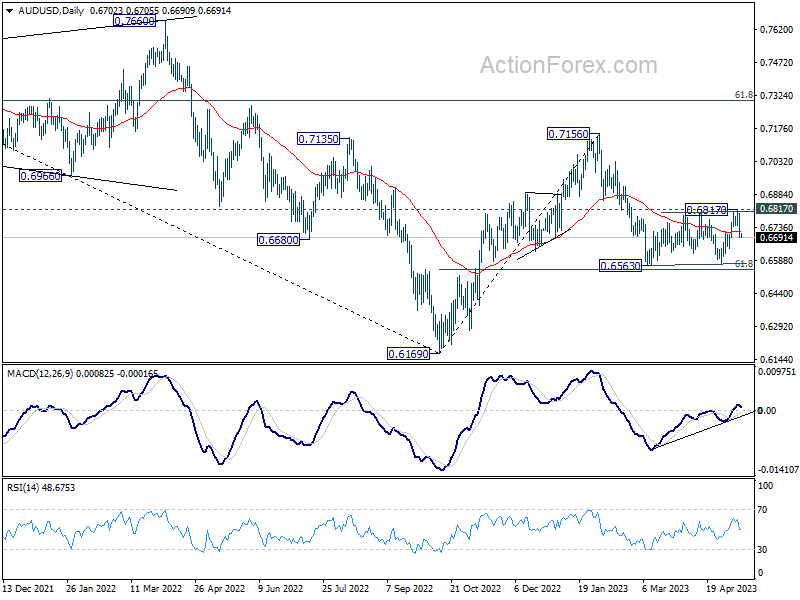

Meanwhile, Australian Dollar the worst performer for the week so far, taking a hit from the drastic fall in Copper prices and growing concerns over China’s economy. Euro is trailing closely behind Sterling as the third weakest currency. New Zealand Dollar is also losing ground following RBNZ’s inflation expectations survey. As risk aversion grows in the commodity sector, Yen, Dollar, and Swiss Franc are gaining traction.

From a technical perspective, the unfolding scenarios in both EUR/USD and USD/CHF markets will be key areas of focus in the coming days. Should EUR/USD see a firm break of 1.0908 support, it would confirm a short-term top and suggest that the pair is already in correction to its entire uptrend from 2022 low of 0.9534. Concurrently, if USD/CHF can decisively break 0.8993 resistance, it would confirm short-term bottom at 0.8818, indicating a potential correction of its entire downtrend from 2022 high at 1.0146. If these scenarios materialize, we could see more upbeat Dollar outlook for the remainder of Q2.

In Asia, at the time of writing, Nikkei is up 0.87%. Hong Kong HSI is down -0.13%. China Shanghai SSE is down -0.40%. Singapore Strait Times is down -0.83%. Japan 10-year JGB yield is down -0.0187 at 0.373. Overnight, DOW dropped -0.66%. S&P 500 dropped -0.17%. NASDAQ rose 0.18%. 10-year yield dropped -0.042 to 3.397.

ECB de Guindos: What worries me is trend in service prices

ECB Vice President Luis de Guindos assured yesterday that “There is no doubt headline inflation will continue to ease”. However, he added a note of caution, “But there are more doubts about underlying inflation.”

De Guindos expressed particular concern about the inflation trend in service prices, a sector showing increased momentum due to rising demand and accelerating salary increases. “What worries me the most in the underlying inflation trend is the trend in service prices,” he revealed. “Momentum in services… is rising. There’s demand and that’s because salary increases are accelerating.”

When discussing future interest rate hikes, de Guindos stated, “There could be more interest rate hikes, but their size will depend on upcoming data and the effect tighter credit will have on economic activity.”

Market expectations lean towards a 25bps increase at the June meeting, with a potential additional hike by summer’s end, followed by rate cuts in early next year. However, de Guindos urged caution in predicting these outcomes. “Don’t believe anybody who tells you what the terminal rate is going to be,” he said. “I don’t feel comfortable or uncomfortable but markets can be wrong about this.”

New Zealand BNZ PMI rose to 49.1, but struggles continue

New Zealand’s manufacturing sector is continuing to grapple with challenges as BusinessNZ Performance of Manufacturing Index edged up to 49.1 in April, from 48.1 in March, remaining below neutral 50.0 mark that separates expansion from contraction.

While the index ticked higher, five of the last seven months have seen contraction, indicating ongoing stress in the sector. In fact, the proportion of negative comments rose to 70.3% in April, compared with 63.2% in March and 60.2% in February. Manufacturers expressed concerns over price pressures, staffing issues, and lower demand, mirroring the broader economic challenges faced by the country.

Digging deeper into the data, we see that production rose from 43.4 to 47.0 and employment edged up from 47.3 to 47.8. New orders also improved, rising from 46.9 to 49.8, but these sub-indexes remained in contraction territory. Finished stocks increased from 48.5 to 52.5, while deliveries dropped from 53.9 to 51.5.

Catherine Beard, BusinessNZ’s Director of Advocacy, commented on the tough conditions, noting the stresses and strains of the wider economy appear to be playing out in the manufacturing sector. She further added that despite the overall activity not straying too far into contraction, the sector seems unable to regain expansion mode, with key indicators of production and new orders failing to return positive results in April.

RBNZ survey sees notable decline in inflation expectations, NZD/USD tumbles

According to RBNZ Q2 Survey of Expectations (Business), inflation expectations for the year ahead took a notable dip, marking the largest drop since June 2020. The one-year-ahead inflation expectation declined by -83 basis points, moving from 5.11% down to 4.28%.

Further into the future, expectations for inflation over a two-year period also demonstrated a decrease. The mean two-year-ahead inflation expectation fell by -51 basis points from 3.30% to 2.79%, placing it back within RBNZ’s target band of 1-3% for the first time since December 2021. The survey also found that the spread of responses has narrowed compared to the previous quarter, with a lower quartile of 2.00% and an upper quartile of 3.00%.

The survey’s respondents also projected changes in the Official Cash Rate. By the end of June 2023, the OCR is expected to rise to 5.47%, an increase of 58 basis points from the last quarter’s mean estimate of 4.89%. However, expectations suggest the OCR will fall back to 4.84% by March 2024, down from the previous quarter’s estimate of 5.00%.

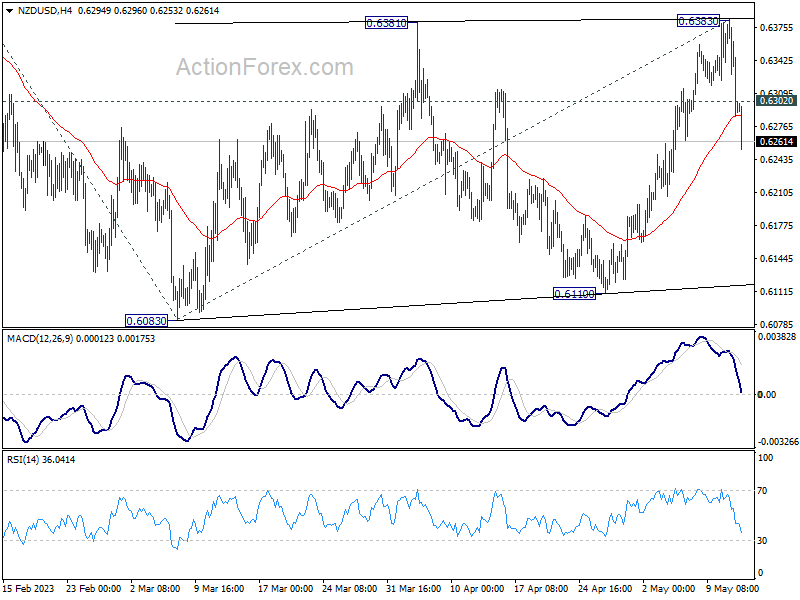

NZD/USD falls notably after the release and broke through 55 4H EMA decisively. The development suggests that rebound from 0.6110 has completed at 0.6383. More importantly, whole corrective pattern from 0.6083 might finished in a three-wave structure too. Deeper decline is now in favor back to retest 0.6083/6110 support zone. Decisive break there will resume whole fall from 0.6537. Meanwhile, break above 0.6302 minor resistance will mix up the near term outlook first.

{kind=link}

{kind=link}

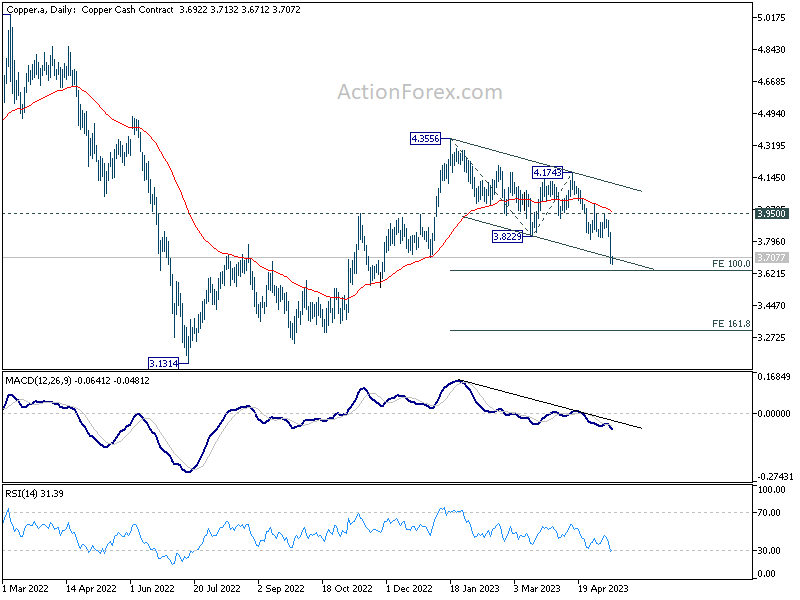

Copper plummets on China outlook, may drag down AUD/USD

Copper prices experienced a precipitous drop this week, puncturing 3.8229 support level and reaching a nadir last seen in November. This sell-off was largely catalyzed by a stark contraction in Chinese import data, which plummeted by -7.9% yoy in April. Specifically, copper imports in the first four months lagged -13% behind 2022’s pace.

This downward trend was exacerbated by release of China’s CPI data, which showed a meager 0.1% yoy rise in April – the lowest since February 2021. Additionally, China’s PPI took a nosedive by -3.6%, marking the steepest descent since May 2020.

These data, combined with recent PMI figures indicating a contraction in manufacturing in April, paint a picture of a modest post-lockdown rebound at best, with risks skewed to the downside.

From a technical perspective, resumption of fall from 4.3556 puts immediate focus on 100% projection of 4.3556 to 3.8229 from 4.1743 at 3.6416. Should this level provide strong support and instigate a rebound through 3.950 resistance level, there’s potential for a bullish resurgence leading to another rise above 4.3556. This would likely resume the whole rebound from 3.1314.

However, sustained break of 3.6416 could prompt downside acceleration towards 161.8% projection at 1.3124. It’s premature to anticipate resumption of the whole fall from 5.0332. Decline from 4.3556 might just be the second leg of the pattern from 3.1314, even in a bearish scenario. But that would depend on the downside momentum of the move.

{kind=link}

Furthermore, should the bearish Copper scenario materialize with a firm break of 3.6416 Fibonacci projection, AUD/USD could be dragged down through 0.6563 support level, thereby resuming the overall decline from 0.7156.

{kind=link}

Looking ahead

UK GDP is a major focus is European session, while production and trade balance will be released. Later in the day, US will publish import price index and U of Michigan consumer sentiment final.

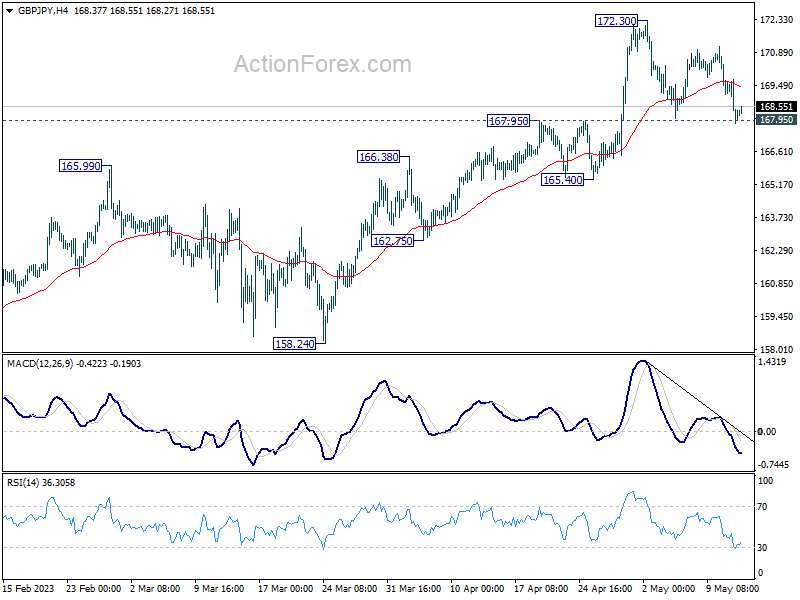

GBP/JPY Daily Outlook

Daily Pivots: (S1) 167.55; (P) 168.66; (R1) 169.47; More…

GBP/JPY dropped notably overnight but recovering after hitting 167.95 resistance turned support. Intraday bias stays neutral first. Further rally could still be seen with 167.95 intact. On the upside, break of 172.30 will resume larger up trend to 100% projection of 148.93 to 172.11 from 155.33 at 178.51. Nevertheless, firm break of 167.95 should confirm short term topping, and turn bias back to the downside for deeper pull back to 165.40 support and possible below instead.

{kind=link}

In the bigger picture, based on current momentum, up trend from 123.94 (2020 low) is likely ready to resume. Next target is 161.8% projection of 122.75 (2016 low) to 156.59 (2018 high) from 123.94 at 178.69. This will now remain the favored case as long as 165.40 support holds, in case of retreat.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI Apr | 49.1 | 48.1 | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Apr | 2.50% | 2.70% | 2.60% | 2.50% |

| 03:00 | NZD | RBNZ Inflation Expectations Q2 | 2.79% | 3.30% | ||

| 06:00 | GBP | GDP Q/Q Q1 P | 0.10% | 0.10% | ||

| 06:00 | GBP | GDP M/M Mar | 0.00% | 0.00% | ||

| 06:00 | GBP | Industrial Production M/M Mar | -0.10% | -0.20% | ||

| 06:00 | GBP | Industrial Production Y/Y Mar | -3.70% | -3.10% | ||

| 06:00 | GBP | Manufacturing Production M/M Mar | -0.10% | 0.00% | ||

| 06:00 | GBP | Manufacturing Production Y/Y Mar | -3.80% | -2.40% | ||

| 06:00 | GBP | Goods Trade Balance (GBP) Mar | -17.5B | -17.5B | ||

| 12:30 | USD | Import Price Index M/M Apr | 0.30% | -0.60% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index May P | 63 | 63.5 |