Yen Staying Generally Weak, Canadian Shrugs Poor Job Data – Action Forex

Yen remains the worst performer for the day, but selloff appears to have slowed somewhat. Meanwhile, Euro and Swiss Franc are also softening, thanks to selling against Sterling. Canadian Dollar is mixed for now, with muted reaction to worse than expected job data from Canada. While the data doesn’t add to the case for another rate hike by BoC in July, the eventual outcome will still very much depend on the next around of economic projections. Meanwhile, Australian and New Zealand Dollars are the better performers today. US Dollar turned mixed digesting some of this week’s losses.

Technically, EUR/GBP is finally resuming recent decline from 0.8977. Next target is 0.8545 support and then 161.8% projection of 0.8977 to 0.8717 from 0.8874 at 0.8453. The question is whether the selloff in EUR/GBP would spread to other Euro pairs. In particular, attention would be on whether EUR/CHF could break through 0.9670 support to resume larger decline.

In Europe, at the time of writing, FTSE is down -0.51%. DAX is down -0.16%. CAC is down -0.29%. Germany 10-year yield is down -0.026 at 2.379. Earlier in Asia, Nikkei rose 1.97%. Hong Kong HSI rose 0.47%. China Shanghai SSE rose 0.55%. Singapore Strait Times rose 0.01%. Japan 10-year JGB yield dropped -0.0070 to 0.435.

Canada employment down -17.3k in May, unemployment rate rose to 5.2%

Canada employment dropped -17.3k, or -0.1% mom in May, worse than expectation of 21.2k growth. That compared to average 33k monthly growth from February to April. Employment was down -30k in the services-producing sector, and up 23k in the goods-producing sector.

Employment rate dropped -0.3% to 62.1%, reflecting strong population growth of 83k in the month.

Unemployment rate rose from 5.0% to 5.2%, above expectation of 5.1%. That’s the first monthly increase since August 2022.

BoJ to persist with monetary easing amid inflation uncertainty, says Ueda

BoJ is committed to maintaining its monetary easing policy as it seeks to sustainably achieve its 2% inflation target, stated BOJ Governor Kazuo Ueda in a parliamentary address.

He acknowledged, “There’s still some distance to sustainably and stably achieve our 2% inflation target. As such, we will patiently maintain our monetary easing policy.”

Ueda explained that the central bank’s strategy is to initiate a positive cycle in which inflation-adjusted wages will start to rise.

However, he also indicated that BOJ anticipates core consumer inflation to dip below 2% target in the latter half of the fiscal year. Despite this projection, Ueda expressed that there remains a substantial degree of uncertainty surrounding the inflation outlook.

One key factor he highlighted is corporate price-setting behaviour, which he stated was “somewhat overshooting expectations.”

China CPI ticked up to 0.2% yoy in May, but PPI down -4.6% yoy

China CPI ticked up slightly from 0.1% yoy to 0.2% yoy in May, above expectation of 0.1% yoy. Core CPI, which excludes volatile food and energy prices, slowed from 0.7% yoy to 0.6% yoy.

Food price rose 1.0% yoy, up from prior month’s 0.4% yoy. However, price for industrial consumer products dropped -1.7% yoy, worse than April’s -1.5% yoy. On a month-on-month basis CPI dropped -0.2% mom, deeper than April’s -0.1% mom.

PPI dropped from -3.60% yoy to -4.6% yoy, below expectation of -3.9% yoy. That’s also the steepest decline in seven years since May 2016.

Dong Lijuan, an NBS statistician, said the consumer inflation picked up marginally with the gradual recovery in consumer demand, while the fall in factory-gate prices was affected by declining international commodity prices, weak demand for industrial products at both home and abroad, as well as a high comparison base in the previous year.

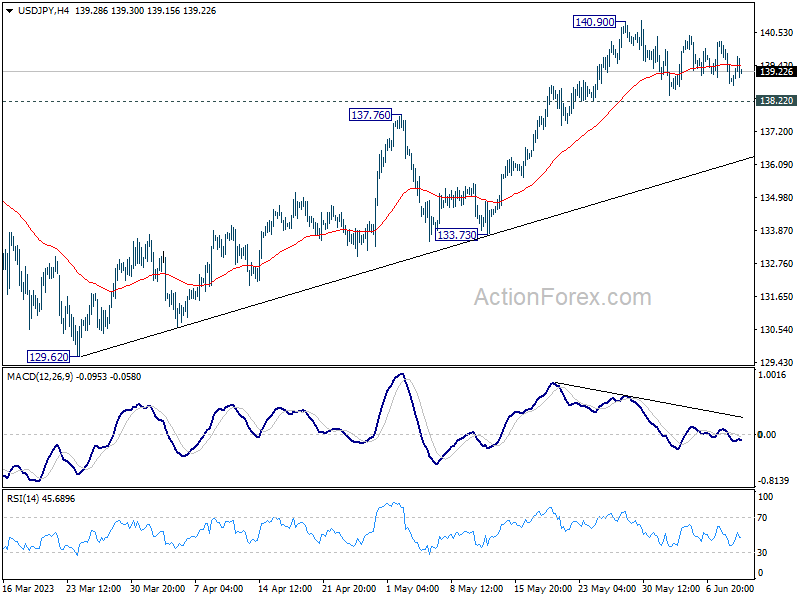

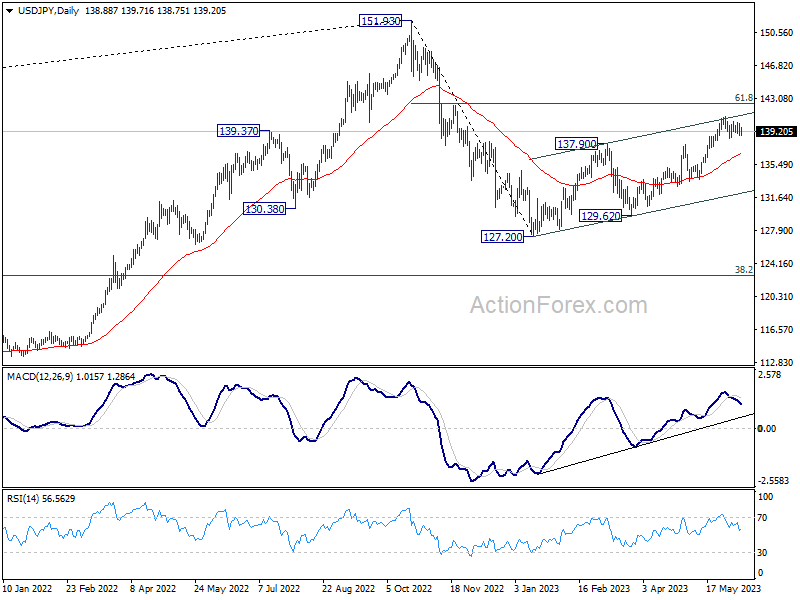

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 138.41; (P) 139.32; (R1) 139.82; More…

Sideway trading continues in USD/JPY and intraday bias remains neutral at this point. With 138.22 minor support intact, further rally is expected. On the upside, break of 140.90 will resume larger rise from 127.20 to 142.48 fibonacci level. However, considering bearish divergence condition in 4 hour MACD, break of 138.22 will confirm short term topping, and turn bias back to the downside for 55 D EMA (now at 136.70).

{kind=link}

In the bigger picture, rise from 127.20 is seen as the second leg of the corrective pattern from 151.93 high. Stronger rally would be seen to 61.8% retracement of 151.93 to 127.20 at 136.34. Sustained break there will pave the way back to retest 151.93. On the downside, however, break of 133.73 support will argue that the pattern could have started the third leg through 127.20 low.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y May | 2.70% | 2.50% | 2.50% | 2.60% |

| 01:30 | CNY | CPI Y/Y May | 0.20% | 0.10% | 0.10% | |

| 01:30 | CNY | PPI Y/Y May | -4.60% | -3.90% | -3.60% | |

| 08:00 | EUR | Italy Industrial Output M/M Apr | -1.90% | 0.10% | -0.60% | |

| 12:30 | CAD | Capacity Utilization Q1 | 81.90% | 82.20% | 81.70% | |

| 12:30 | CAD | Net Change in Employment May | -17.3K | 21.2K | 41.4K | |

| 12:30 | CAD | Unemployment Rate May | 5.20% | 5.10% | 5.00% |