RBA and BoC Bombshells Stir Market Waters; Dollar, Euro and Yen Suffered – Action Forex

Last week marked the beginning of an avalanche of central bank surprises, with both RBA and BoC springing unexpected rate hikes on markets. However, the market reactions diverged substantially. Despite a weaker-than-anticipated Australian GDP report and terrible Chinese trade data, Aussie’s underlying strength was striking. In contrast, the Loonie’s ascent was curtailed by worse-than-expected employment figures.

When the dust settled, Aussie emerged as the top performer, followed by Kiwi and then Sterling. Loonie’s rally left it in fourth place. Pound gained significant ground in the latter part of the week, largely buoyed by purchases against the Euro as markets recalibrated expectations for BoE’s terminal rate. Dollar languished at the bottom of the pile, but its performance was not dramatically dissimilar from Euro and Yen.

Markets brace themselves for more potential surprises and volatility in the coming days with Fed, ECB, and BoJ due to announce their policy decisions this week. BoE and SNB will follow suit the next week, adding to the mix of market excitement.

Aussie as top performer following RBA’s surprise rate hike

Australian Dollar secured its position as the strongest currency of the week, spurred by RBA’s unexpected 25bps rate hike to 4.10%. The central bank’s communication, underscored by Governor Philip Lowe’s speech, has marked a distinct pivot back to tackling inflation. Opinions are divided on whether another rate hike will be announced at the next meeting, but there is a broad consensus that further tightening will occur within the third quarter. The bank’s hawkish inclination is clearly discernible.

Australian Dollar ended as the strongest currency after RBA’s surprised 25bps rate hike to 4.10%. The focus of the statement, as well as speech of Governor Philip Lowe a day after, seemed to have emphasis shifted back to fighting inflation. Opinions on whether RBA would hike again at next meeting is divided, but there seems to be a consensus of more tightening within Q3. Either way, hawkish bias is clear.

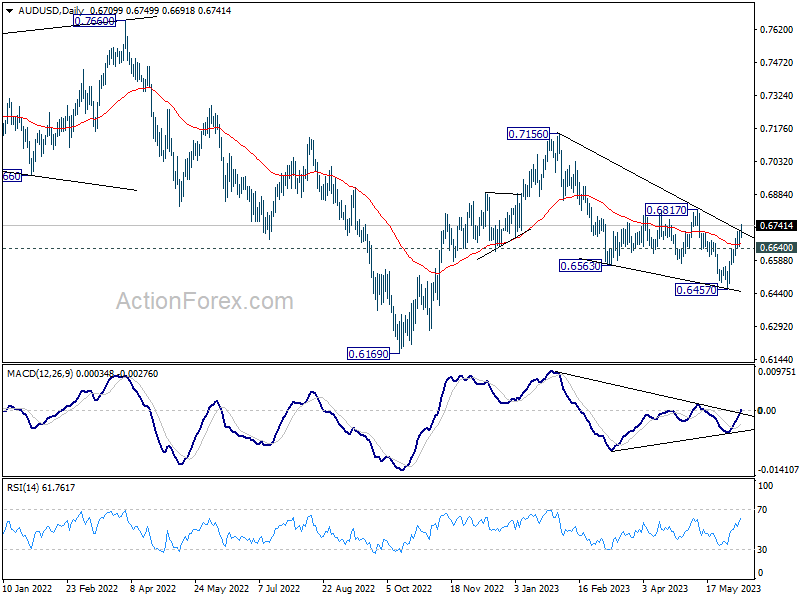

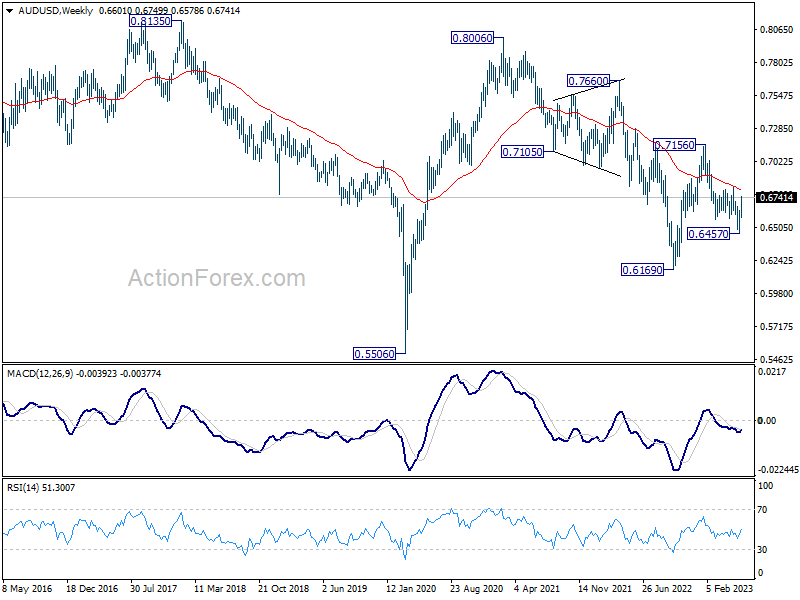

AUD/USD was the top mover last week, ended up more than 2%. The break of trend line resistance, together with bullish convergence condition in D MACD raises the chance that fall from 0.7156 has completed at 0.6457.

{kind=link}

More importantly, the three-wave corrective structure of the decline argues that rise from 0.6457 is possibly resuming whole rebound from 0.6169 (2022 low). Further rally is now in favor as long as 0.6640 support holds, with 0.6817 resistance as next target. Decisive break there will solidify the bullish case and extend the rise towards 0.7156 in H2.

{kind=link}

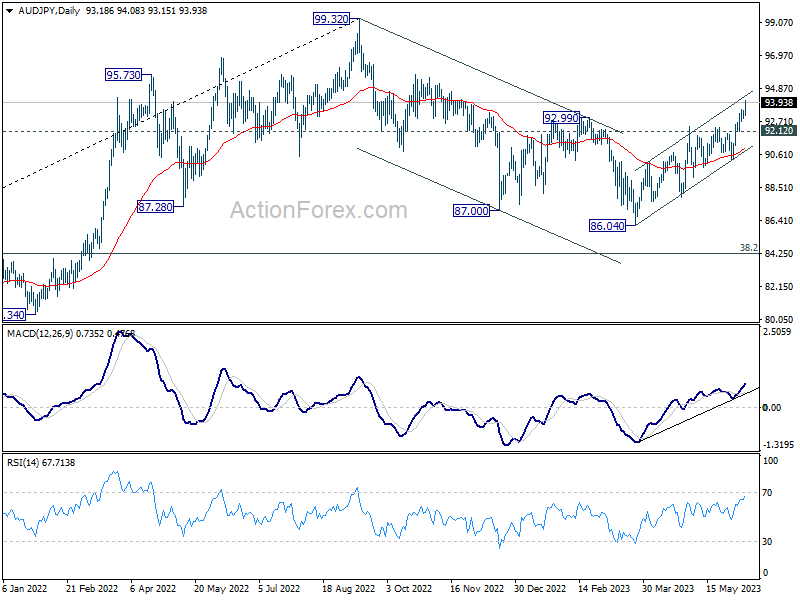

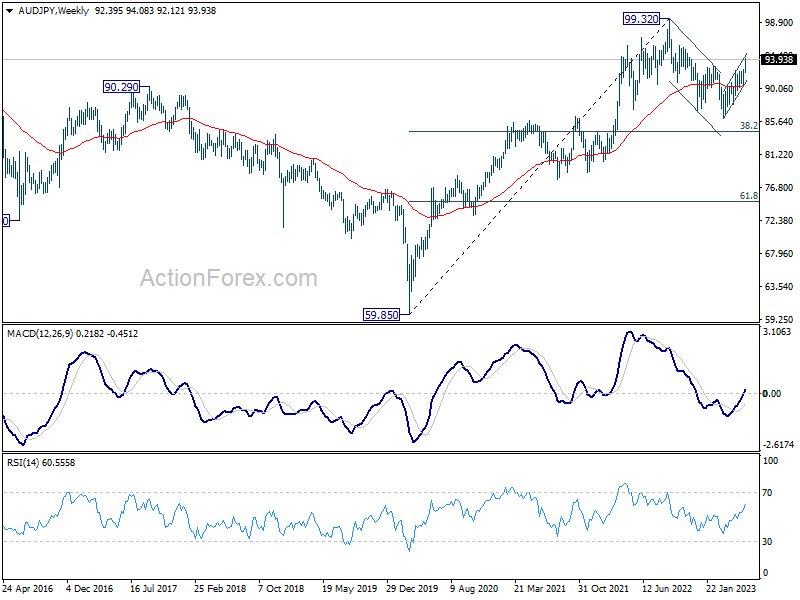

AUD/JPY was the third top mover last week, next to EUR/AUD. The firm break of 0.9299 should confirm that corrective fall from 99.32 has completed with three waves down to 86.04. Further rise is expected as long as 92.12 support holds, to retest 99.32 high.

{kind=link}

However, AUD/JPY presents a different overall outlook compared to AUD/USD. Price actions from 99.32 are seen as correcting the whole uptrend from 59.85 (2020 low). Consequently, the pattern from 99.32 could potentially stretch further with another falling leg. Thus, attention will be paid to sign of loss of momentum and reversal as AUD/JPY approaches 99.32 high.

{kind=link}

Loonie’s BoC inspired rally capped by weak job data

Despite BoC surprising 25bps rate hike to 4.75%, Canadian Dollar struggled to extend gain towards the end of the week. This hesitation in performance was largely due to disappointing job data. Market expectations, however, underwent a dramatic shift over the week, transitioning from anticipation of a 25bps rate cut by year’s end to now foreseeing an additional rate hike of the same magnitude or potentially more. The consensus now predicts another 25 basis point hike to 5.00% in July, though what lies beyond remains uncertain.

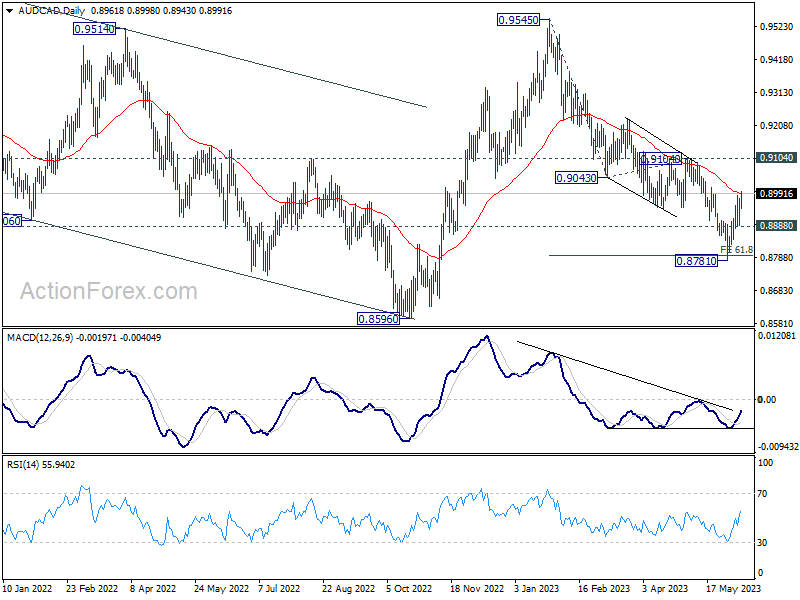

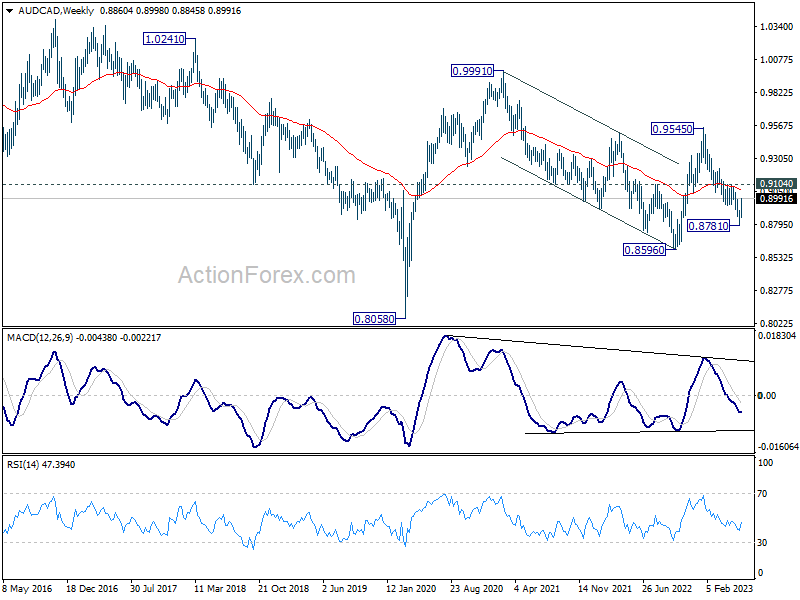

AUD/CAD’s strong rebound last week suggests clearly indicate the relative performance. The development now raises the chance that whole corrective fall from 0.9545 has completed with three waves down to 0.8781, after hitting 61.8% projection of 0.9545 to 0.9043 from 0.9104 at 0.8794.

{kind=link}

Further rally is expected as long as 0.8888 resistance holds. Firm break of 0.9104 will solidify this bullish case, and pave the way to retest 0.9454 high next.

{kind=link}

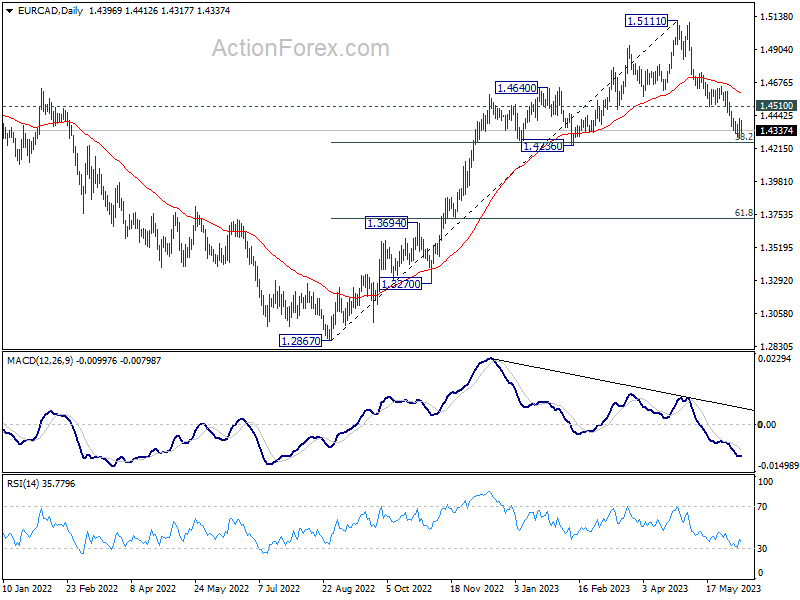

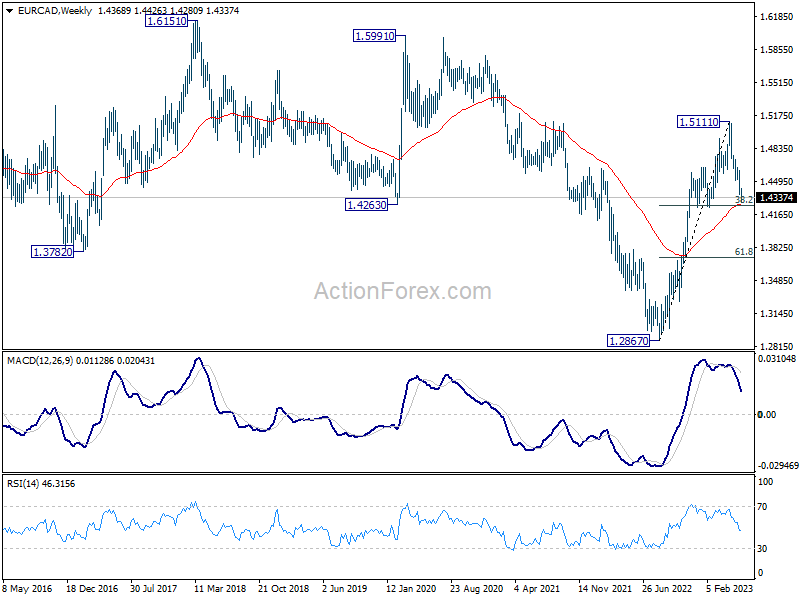

EUR/CAD’s fall from 1.5111 appeared to have slowed at it approached 1.4236 cluster support (38.2% retracement of 1.2867 to 1.5111 at 1.4254), which is also close to 55 W EMA (now at 1.4261).

{kind=link}

A strong bounce from current level, followed by break of 1.4510 support turned resistance, will argue that the corrective decline from 1.5111 has completed. Further break of 55 D EMA (now at 1.4595) will pave the way to retest 1.5111 high. However, sustained decisive break of 1.4236 could trigger further downside acceleration to 61.8% retracement at 1.3724, even just as a deep corrective move.

Meanwhile, it should be emphasized that performance of EUR/CAD will also depend on the overall strength of Euro, which will be affected by its actions against Dollar and other European majors.

{kind=link}

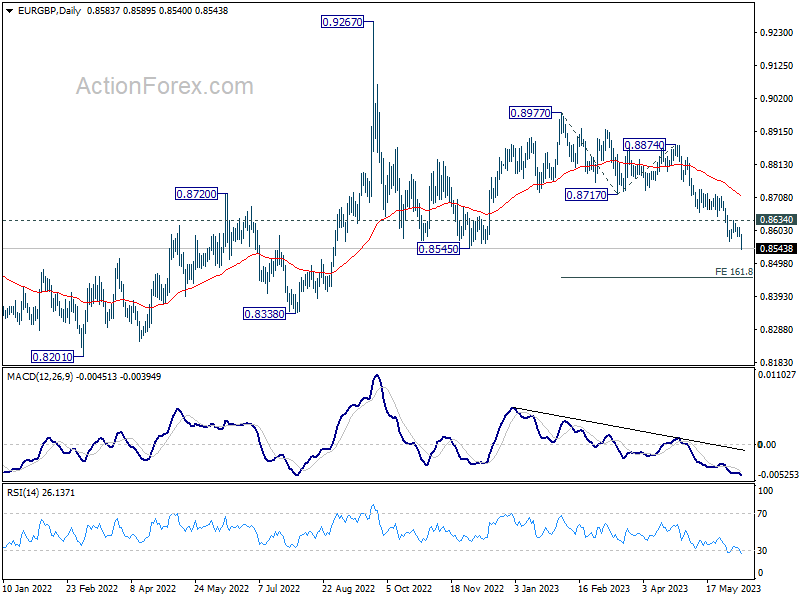

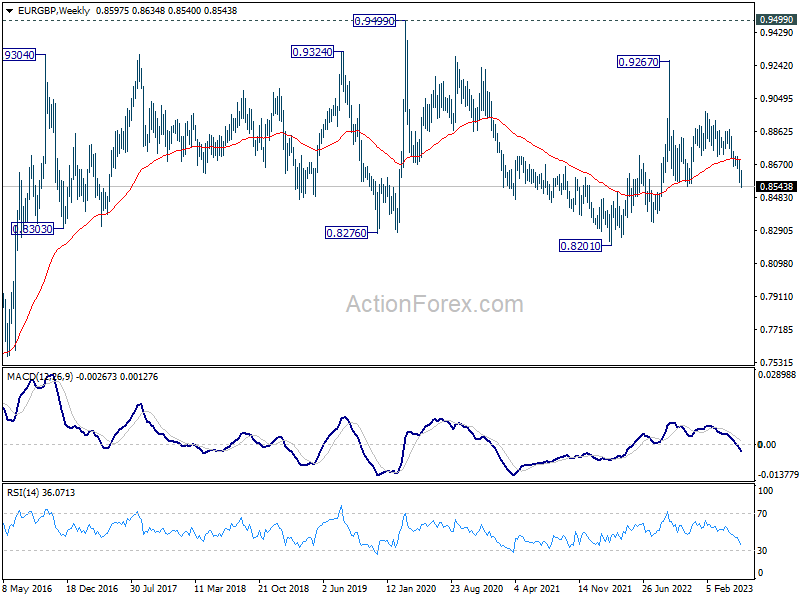

EUR/GBP extended down trend on BoE rate expectations

Talking about Euro, the decline in EUR/GBP is worth a mention. This depreciation can be attributed, in part, to the Euro’s general weakness following the latest inflation reports. While ECB is widely expected to continue tightening on June 15, a peak seems more likely during the summer.

Contrarily, market predictions for BoE terminal rate are being adjusted upwards to 5.50% from the previous 4.50% prediction. This alteration comes as UK inflation struggles to decelerate at the anticipated pace, prompting a re-evaluation of BoE’s potential response.

EUR/GBP extended the fall from 0.8977 and has indeed closed below 0.8545 medium term support (2022 low). Near term outlook will stay bearish as long as 0.8634 resistance holds. Next target is 161.8% projection of 0.8977 to 0.8717 from 0.8874 at 0.8453.

Extended selloff in EUR/GBP could be accompanied by even deeper decline in Euro-commodity crosses.

{kind=link}

{kind=link}

Dollar’s uncertain trajectory: Weakness offset by soft Euro and Yen

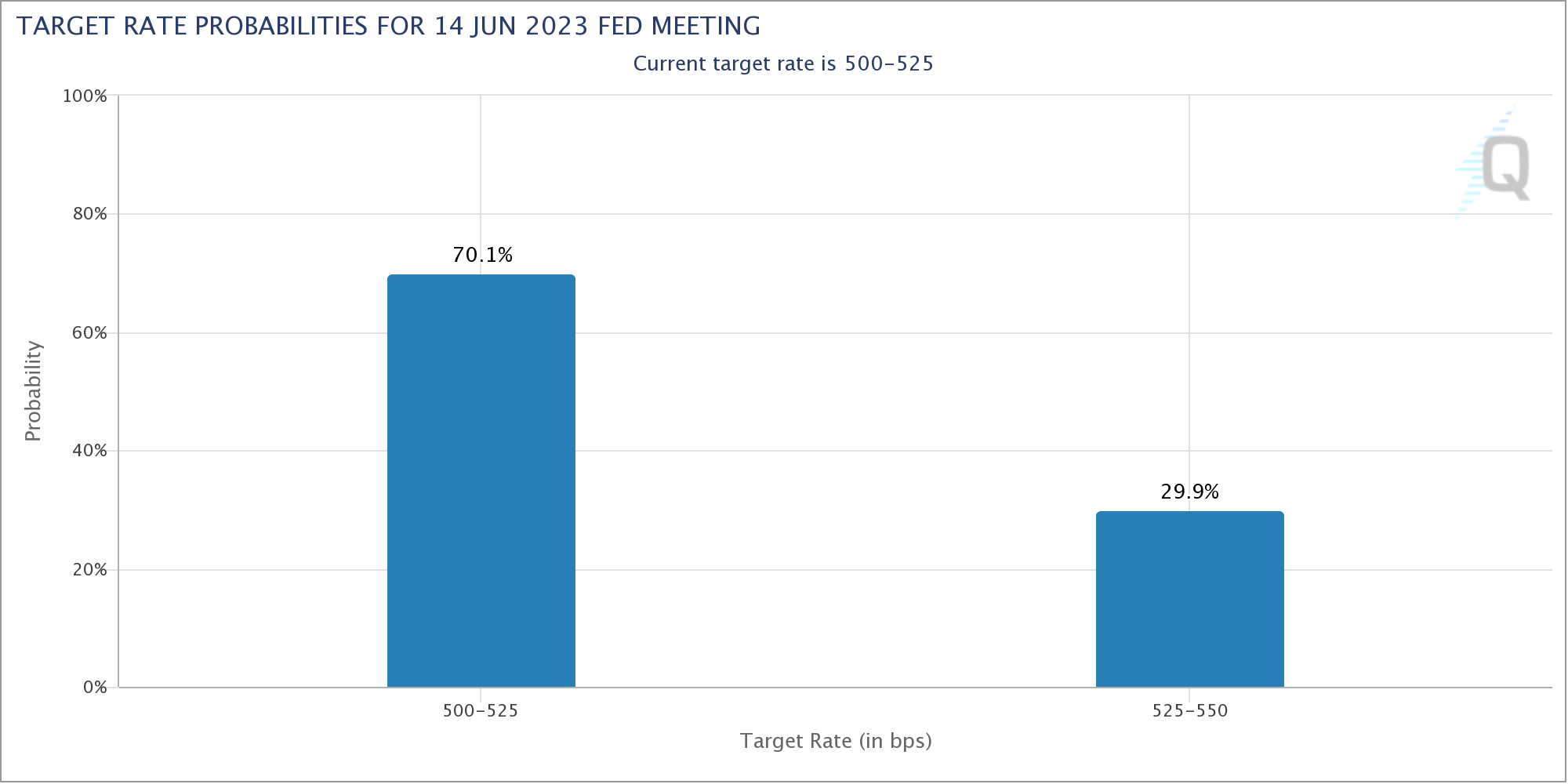

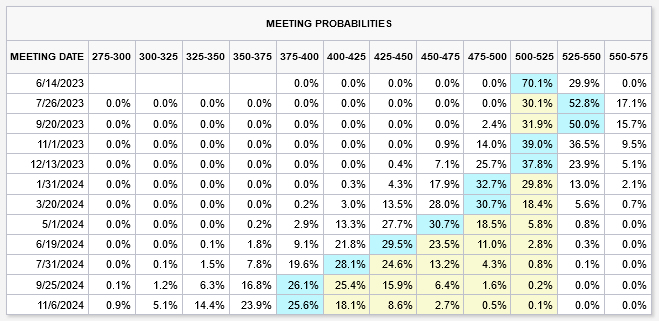

Dollar’s broad based weakness was clear last week, but that wasn’t much reflected in Dollar index. A “skip” is probably a done deal for FOMC rate decision on June 14. There is 70% chance of a hold at 5.00-5.25% as indicated by fed fund futures. Meanwhile, there is near 70% chance a final 25bps hike in July to 5.25-5.50%. But there are much uncertainty beyond June, subject to this week’s CPI release, as well as new Fed economic projections.

{kind=link}

{kind=link}

The softness in Euro and Yen kept Dollar Index’s loss limited last week. With 55 D EMA (now at 103.09) intact, it’s technically uncertain whether rise from 100.78 has completed at 104.69. That is, another rally through this resistance is possible. But even in this case, strong resistance is anticipated at 38.2% retracement of 114.77 to 100.82 at 106.14 to complete the corrective pattern from 100.82.

Meanwhile, sustained break of 103.09 will turn near term outlook bearish for a retest of 100.82. But that would come in the unlikely event of simultaneous strength in both Euro and Yen.

{kind=link}

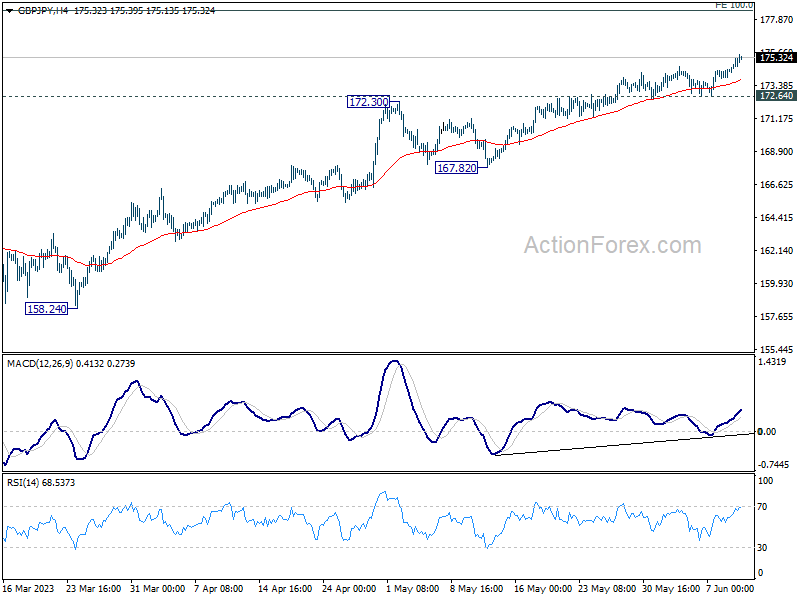

GBP/JPY Weekly Outlook

GBP/JPY’s up trend continued last week and hit as high as 175.52. Initial bias remains on the upside for this week for 100% projection of 148.93 to 172.11 from 155.33 at 178.51 next. Strong resistance could be seen from there to bring pull back, at least on first attempt. But break of 172.64 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

{kind=link}

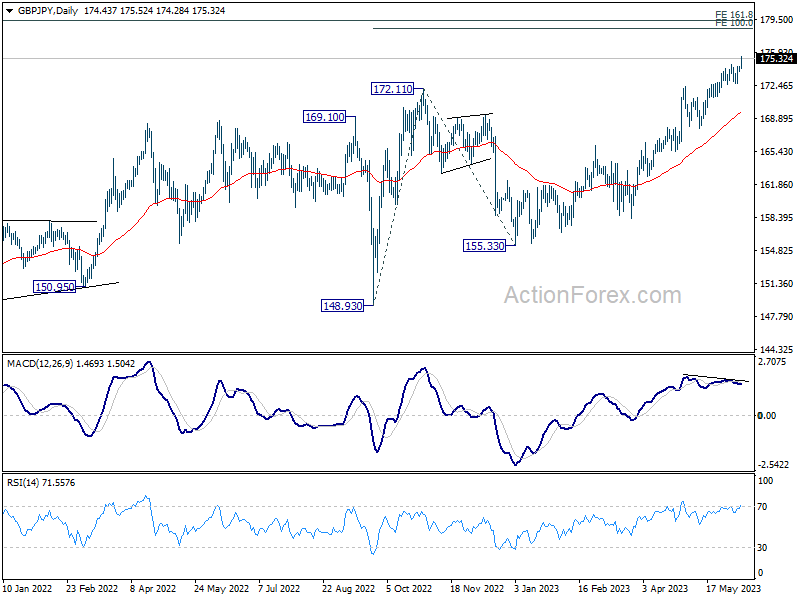

In the bigger picture, up trend from 123.94 (2020 low) is extending. Next target will be 161.8% projection of 122.75 (2016 low) to 156.59 (2018 high) from 123.94 at 178.69. For now, medium term outlook will remain bullish as long as 167.82 support holds, even in case of deep pull back.

{kind=link}

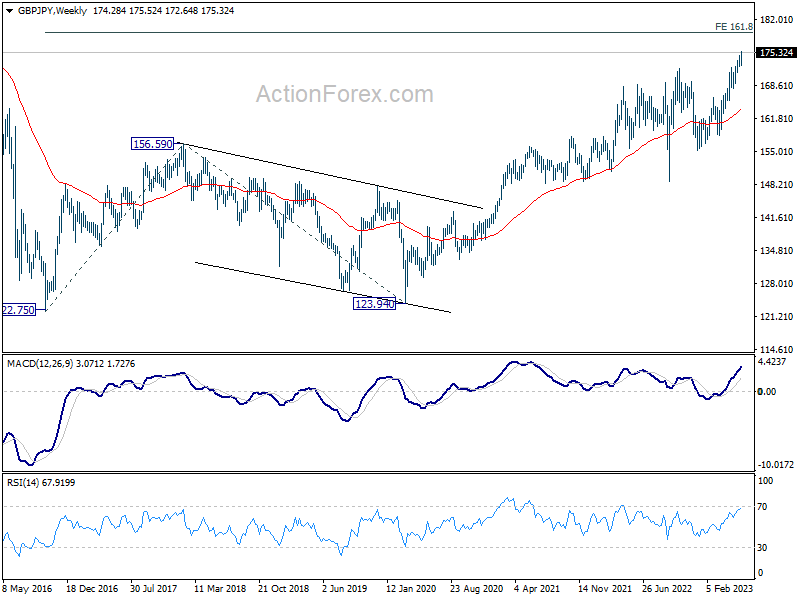

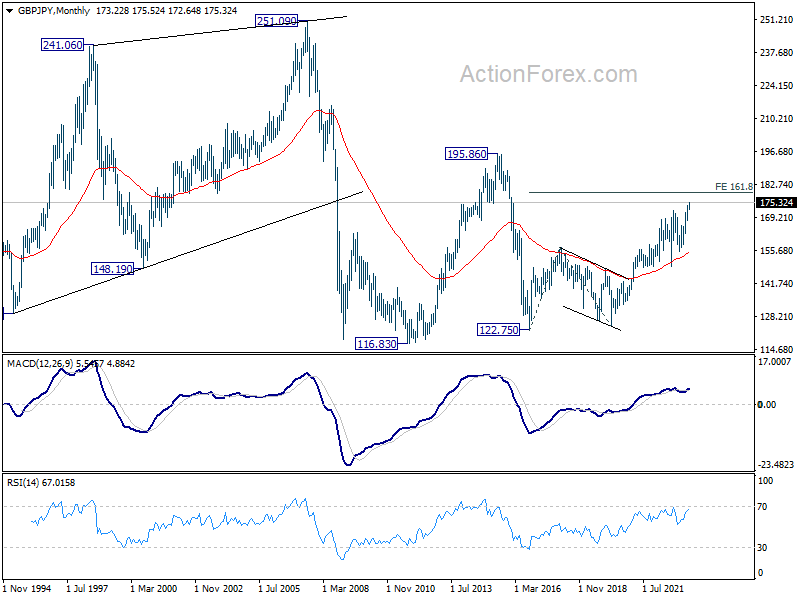

In the longer term picture, as long as 55 M EMA (now at 155.22) holds, rise from 122.75 (2016 low) could still extend higher to 195.86 (2015 high).

{kind=link}

{kind=link}